Following numerous postponements, Ethereum validators are now able to retrieve their staked Ether and associated rewards from the Ethereum mainnet. The Shapella hard fork has been successfully implemented on the Ethereum mainnet, enabling validators to withdraw their staked Ether from the Beacon Chain.

The highly anticipated Shapella update on Ethereum has been launched, introducing the much-awaited new feature, the Ether unstaking. The Ethereum community has expressed various reactions to the latest update in the ecosystem. The term “Shapella” is a combination of “Shanghai” and “Capella,” referring to simultaneous upgrades. This hard fork marks a significant milestone in Ethereum’s development, generating excitement among community members for the network’s future.

The highly anticipated update occurred at 10:27 pm UTC on April 12, during epoch number 194,048. In the initial hour following the hard fork, Ethereum block explorer beaconchai.in reported that 12,859 Ether were released through 4,333 withdrawals.

Ether staking rewards are withdrawn

At present, approximately 44% of validators, equating to 248,043 out of 559,549 active validators, have the option to request a partial or complete withdrawal.

Most of the current withdrawals range from 2.8 to 3.2 ETH, indicating that primarily staking rewards are being withdrawn at this time. Data from Rated Network Explorer reveals that just before the Shapella hard fork was implemented, 3,996 validators joined the exit queue.

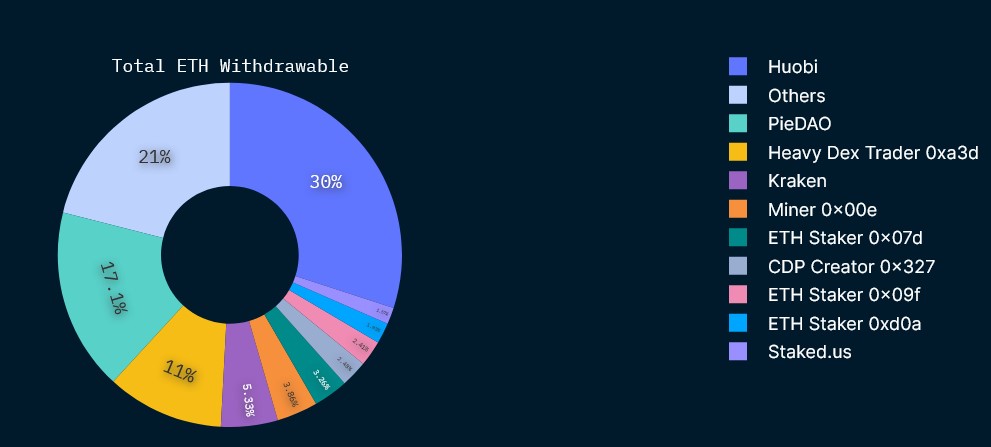

Based on data from blockchain analytics company Nansen, crypto exchange Huobi possesses the most significant portion of withdrawable Ether at 30%. The decentralized autonomous organization PieDAO follows with a 17.7% share.

Nansen data indicates that 284,622 Ether from 7,948 validators are awaiting complete withdrawal. The price of Ether experienced minimal fluctuations during the first hour after the hard fork, as forecasted in an April 11 report by blockchain intelligence platform Glassnode. In theory, the hard fork could unlock 18.1 million Ether on the Beacon Chain, which is equivalent to over $34.8 billion.

However, the Ethereum Foundation has implemented several measures to prevent a sudden influx of ETH into the market. Glassnode’s report projected that less than 1% of the total amount would be released during the first week, and the 12,859 Ether unlocked within the first-hour accounts for a mere 0.07% of the total Ether staked on the Beacon Chain.

As for the market, the predictions are optimistic. The capacity of Ether to surpass resistance levels has led some analysts to predict a $3,000 price target in Q2 2023. Data from analytics provider Santiment reveals that whale accumulation remains robust, increasing by 0.5% in March.

This positive buying activity could support on-chain data indicating that Ether sell pressure following the Shanghai hard fork will be insignificant.

Ethereum Investment Proposal EIP-4895 facilitated the transfer of staked Ether from the Beacon Chain to the Ethereum Virtual Machine (EVM). This is known as the execution layer, thereby enabling withdrawals. This update on the Ethereum blockchain represents the most substantial upgrade since the Merge on September 15 and brings Ethereum one step closer to achieving a fully operational proof-of-stake system.

The community celebrates the Ethereum Shapella upgrade

During the Shapella watch party organized by the Ethereum Foundation team, Ethereum co-founder Vitalik Buterin expressed that the network is currently in a “really good place.” He said the most challenging and rapid aspects of the Ethereum protocol’s transition have essentially concluded. There are still substantial tasks to be accomplished, but they can proceed at a more relaxed pace.

In celebration of the new update, crypto singer Jonathan Mann performed a song at the Shapella watch party.

As some community members celebrated the event, others focused on the network’s future prospects. Ethereum community member Anthony Sassano highlighted the next significant feature, EIP-4844, which aims to improve the scalability of rollups on Ethereum.

The Shapella update is expected to attract more institutional investors to Ethereum.

The U.S. Treasury warns about DeFi. But they acknowledge that the majority of money laundering, terrorist financing, and proliferation financing still take place using fiat currency or outside the realm of cryptocurrency.

According to a recent report from the U.S. Treasury Department, it was observed that individuals from the Democratic People’s Republic of Korea, along with other fraudsters, were exploiting vulnerabilities of DeFi to facilitate money laundering. The report also stated that the majority of instances of money laundering, terrorist financing, and proliferation financing still took place using fiat currency or outside the crypto ecosystem.

The U.S. Treasury, in its “Illicit Finance Risk Assessment of Decentralized Finance” report, which was published on April 6th, stated that certain groups engaged in illicit activity from North Korea were able to take advantage of some DeFi platforms’ non-compliance with Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT) regulations.

How illicit activity is performed on DeFi platforms

These actors utilize different tactics and services, such as exchanging virtual assets for other more manageable or less traceable virtual assets, using cross-chain bridges to swap virtual assets from other blockchains, sending virtual assets through mixers, and placing virtual assets in liquidity pools as a form of layering.

Although the money laundering process by malign actors remains the same, they may use new methods like chain hopping. Criminals find DeFi services more appealing than centralized VASPs as they don’t need to provide customer identification information.

Such laundering methods pose challenges for investigators tracing illegal proceeds, and actors typically use more than one technique, with a level of sophistication depending on their technical experience and familiarity with DeFi services. However, even lesser-skilled actors have been observed using some of these tactics, according to law enforcement.

Most of the time, they use:

DEXs and cross-chain bridges to convert virtual assets. Illicit actors often use decentralized exchanges (DEXs) to exchange virtual assets, such as cryptocurrencies, into a different virtual asset. They may do this to exchange into a more liquid asset that has higher trading volumes and is easier to cash out into fiat currency. They may also exchange virtual assets for another virtual asset that is compatible with a cross-chain bridge, mixer, or other DeFi service or exchange for an asset that is less traceable. This allows them to move their funds between different blockchains and makes it more difficult for authorities to trace financial transactions.

Virtual asset mixers to obfuscate transaction information. Criminals use virtual asset mixers to functionally obfuscate the source, destination, or amount involved in a transaction. Mixers pool or aggregate virtual assets from multiple individuals, wallets, or accounts into a single transaction. They may also split an amount into multiple amounts and transmit the virtual assets as a series of smaller independent transactions or leverage code to coordinate, manage, or manipulate the structure of the transaction. Mixing services may be advertised as a way to evade Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT) requirements and rarely include the capacity and willingness to provide upon request to regulators or law enforcement the resulting transactional chain or information collected as part of the transaction.

Placing illicit funds in liquidity pools to generate funds from trading fees. Illicit actors can place criminals’ proceeds in a DeFi service’s liquidity pool, where the assets provide liquidity to support trades on the service. By placing funds into liquidity pools, actors may generate funds from trading fees. Liquidity providers typically lock their virtual assets into the liquidity pool and may receive a portion of fees or some other type of return or interest created through the DeFi service. This allows bad actors to receive profits from their illicit funds without directly accessing them.

The report’s highlights

The report highlighted that inadequate AML/CFT controls and other deficiencies in DeFi services “facilitate the theft of funds.” Brian Nelson, the undersecretary of the Treasury for Terrorism and Financial Intelligence, pointed out that illicit actors, including criminals, scammers, and North Korean cyber actors, were utilizing DeFi services to launder illicit funds. To reap the potential benefits of DeFi services, addressing these risks is necessary.

However, the Treasury reaffirmed that most instances of money laundering, terrorist financing, and proliferation financing still took place using fiat currency or outside the digital asset ecosystem.

Officials recommended increasing regulatory supervision of AML/CFT for platforms offering DeFi services, providing guidance to DeFi platforms on AML/CFT, and addressing regulatory gaps.

The evaluation was conducted in compliance with an executive order on digital assets signed by President Joe Biden in March 2022. In response to the order, various U.S. government agencies have started examining the potential implications of different aspects of the digital asset space on the country’s financial system and payment infrastructure.

According to a blog post by a pseudonymous Bitcoin app developer called 0xB10C, a mysterious entity has allegedly been gathering the IP addresses of BTC users since March 2018. The entity has reportedly used 812 different IP addresses to conceal its identity while collecting data.

This activity violates the users’ privacy as the entity is said to be linking the IP addresses to their BTC addresses. Over the past few years, Bitcoin node operators have reported the entity’s IP addresses in several public posts.

0xB10C, the developer behind Bitcoin analytics websites such as Mempool.observer and Transactionfee.info, has previously received a Bitcoin developer grant from Brink.dev. In a recent blog post, 0xB10C revealed an entity that they have named “LinkingLion,” due to the IP addresses associated with it passing through LionLink network’s colocation data center. However, 0xB10C noted that ARIN and RIPE registry information suggests that LionLink may not be the originator of the messages.

LinkingLion reportedly uses 812 different IP addresses to establish connections with Bitcoin full nodes that are visible on the network, and then asks which version of the Bitcoin software they are using. However, the entity often closes its connection without responding, despite the node’s compliance with the request, occurring approximately 85% of the time.

The recent blog post suggests that the mysterious entity may be attempting to determine if a particular Bitcoin node can be reached at a specific IP address. While this behavior may not be alarming on its own, what the entity does the other 15% of the time is what raises concerns. The post by 0xB10C indicates that during this 15% of the time, the entity does not immediately terminate the connection. Instead, it listens for inventory messages containing transactions or requests for an address and then listens for both inventory and address messages before closing the connection within 10 minutes.

Although this behavior is typical of a node updating its copy of the blockchain, LinkingLion never requests blocks or transactions, suggesting that the entity has an ulterior motive for gathering this information.

Tracking the IP address of a specific Bitcoin address

As per 0xB10C’s blog post, LinkingLion might be keeping track of transaction timing to identify the node that received a transaction first, allowing the entity to associate an IP address with a specific Bitcoin address. The developer explained that nodes that complete the version handshake and remain connected obtain knowledge of the node’s inventory, including blocks and transactions. The timing information of when a node announces new inventory is particularly relevant, as the entity may learn about a new wallet transaction from that node first. Given its connections to several listening nodes, the entity can utilize this information to link broadcast transactions with their corresponding IP addresses.

To counteract the potential invasion of privacy caused by LinkingLion, 0xB10C has created an open-source ban list that nodes can utilize to block connections from the entity. However, the developer cautioned that the entity could bypass this ban list by altering the IP addresses it employs to connect. 0xB10C believes that the only long-term solution to the issue is to change the transaction logic in Bitcoin Core, which developers have struggled to achieve thus far.

During a conversation with Cointelegraph, 0xB10C noted that this vulnerability could impact not just users running their own nodes but also users who depend on a third-party server through a wallet such as Electrum or Mycelium. As a result, the privacy of a large number of BTC users is potentially at risk.

According to 0xB10C, when using an Electrum wallet, users connect to a remote Electrum server and communicate information such as which addresses they are interested in and details of their transactions, all of which can be associated with their IP address if they don’t use Tor or a similar tool to protect their privacy. The developer further explained that LinkingLion could operate public Electrum servers and entice users to connect to them, potentially allowing the entity to obtain users’ IP addresses and associated transaction data. As a result, it has been suggested that running an Electrum server connected to one’s node is a safer option.

The issue of privacy has been a persistent concern among Bitcoin and other cryptocurrency users. While Bitcoin addresses are pseudonymous, the entire transaction history associated with them is publicly available. Notably, Breeze Wallet has sought to enhance privacy on the network by utilizing cryptographic puzzles and off-chain transactions. Despite these efforts, Bitcoin educator Andreas Antonopoulos has argued that Bitcoin may never be fully private.

Recently, the Montana Senate passed a bill that aims to safeguard the interests of crypto miners operating within the state.

The proposed law is currently being reviewed by the Montana House of Representatives and seeks to eliminate discriminatory regulations that could hamper their mining operations, both for individuals and commercial entities.

The bill seeks to exempt digital assets used as payment from taxes, and allow home crypto mining that uses less than 1 megawatt of energy annually, except when it violates existing noise bylaws.

The proposed pro-crypto mining bill in Montana aims to remove any energy rate classification that hinders home crypto mining and digital asset businesses. Lobbyists and crypto companies have been working together for years to establish crypto-friendly laws in the state. Montana has high wind energy potential, but remote wind projects struggle due to the need for long transmission lines. However, the bill can be an early buyer of that power and help to bring customers (Bitcoin miners) to the state. There is a misconception that mining is bad for the grid or the environment is holding back the crypto-mining industry in the United States, despite it being a powerful tool for balancing the grid and cleaning up the environment.

Regulatory policies also fail to consider the positive aspect of this process. One of these would be the grid balancing concept.

Crypto mining is best suited for states with grid-balancing programs. These programs pay participants to lower their power consumption during times of high power prices or low supply. Miners can easily reduce their power consumption at any hour of the day, making them ideal participants in such programs.

What is the Montana pro-crypto bill?

The proposed bill seeks to establish a “right to mine digital assets” in Montana and prevent discriminatory electricity rates for crypto miners. The bill also protects “home” mining and removes local government’s power to use zoning laws to prohibit crypto mining operations.

Additionally, the bill prohibits extra taxes on the use of crypto as a payment method and categorizes digital assets as personal property, similar to stocks and bonds. The Montana Senate passed the bill on Feb. 23 with 37 for and 13 against, and it will now be presented to the House for approval. Finally, the bill will require the signature of Governor Greg Gianforte to become law, who may choose to veto it.

How Montana Could Benefit from Pro-Crypto Mining Bill

Proponents of the bill anticipate that Montana can attract mining companies by updating legislation, which will, directly and indirectly, boost the region’s economy.

Montana State Senator Daniel Zolnikov, the primary advocate of the bill, believes that Montana has a lot to gain by embracing the digital asset industry.

By permitting unrestricted crypto mining operations, Montana can potentially attract more businesses and investments from the cryptocurrency sector, creating jobs in rural communities.

Senator Zolnikov hopes that this move will signal to the larger digital asset industry that Montana welcomes their innovation and new companies into the state.

Sustainability Concerns Surrounding Montana’s Pro-Crypto Mining Bill

Despite optimism about the potential benefits of crypto mining, some are concerned about the impact on small towns and communities.

Colin Read, former mayor of Plattsburgh, New York, and SUNY economics professor, pointed out that mining companies often fail to deliver on their promises of job creation.

Additionally, an influx of crypto mining companies could cause energy and sustainability challenges, as seen in New York, which experienced skyrocketing retail energy rates due to increased demand.

As a result, the New York Public Service Commission introduced steeper energy tariffs for crypto miners to mitigate the issue.

Similar challenges have arisen in Texas, where crypto mining businesses have set up operations, leading to power grid overloading during extreme weather conditions.

In Montana, Missoula County has implemented requirements for crypto mining firms to either consume or generate enough renewable energy to cover 100% of their operations, responding to concerns about power consumption and pollution. These sustainability concerns underscore the importance of balancing the potential economic benefits of pro-crypto mining legislation with sustainable energy practices.

Montana’s weather conditions, including summer heat rising above 100 degrees Fahrenheit (38 Celsius) and sub-zero temperatures in winter, contribute to the state’s high per capita energy consumption rate. Due to environmental concerns surrounding the environmental impact of crypto mining, several American states have implemented laws limiting energy-intensive activities, such as placing caps on energy usage or restricting energy sources.

For instance, New York recently imposed a temporary ban on mining firms using non-renewable energy sources to reduce the state’s carbon footprint. Montana may face similar sustainability challenges if its pro-crypto mining bill is passed.

Senator Zolnikov addressed these concerns, stating that Montana already has an attractive energy mix for digital asset mining and that the bill aims to provide legal certainty for long-term operations. Montana has access to geothermal, wind, solar, and hydro energy sources, including the Missouri River and its tributaries, which are used to generate hydroelectric energy.

Will the pro-crypto bill pass?

Montana’s pro-crypto mining bill aims to attract more cryptocurrency mining businesses to the state, potentially bringing positive transformations. However, the bill’s approval could lead to initial sustainability challenges related to eco-friendly and sustainable energy.

While Montana presently has both renewable and non-renewable energy sources, the state’s response to emerging changes in the wake of the pro-crypto mining legislation will be crucial. Balancing economic benefits with sustainable energy practices will be a delicate balancing act for Montana.

Euler Finance fell victim to a flash loan attack that resulted in the loss of more than $195 million in stablecoins and ERC-20 tokens.

On March 13, Euler Finance, a noncustodial lending protocol based on Ethereum, was hit by a flash loan attack. This resulted in the theft of millions of dollars in Dai (DAI), USD Coin (USDC), staked Ether (stETH), and wrapped Bitcoin (wBTC). As per the latest update from on-chain data, the attacker carried out multiple transactions and was able to steal almost $196 million, making it the largest hack of 2023 thus far.

The funds stolen include the following:

DAI (8,877,507.35)

wBTC (849.14)

stETH (73,821.42)

USDC (34,413,863.42)

stETH (3,897.50)

stETH (8,099.30)

As per findings by the crypto analytic company Meta Seluth, the recent attack appears to be linked to the deflation attack that occurred a month ago. The attacker leveraged a multichain bridge to transfer the funds from BNB Smart Chain (BSC) to Ethereum and executed the attack today.

This DeFi attack on Euler Finance is one of the most significant hacks of 2023 thus far.

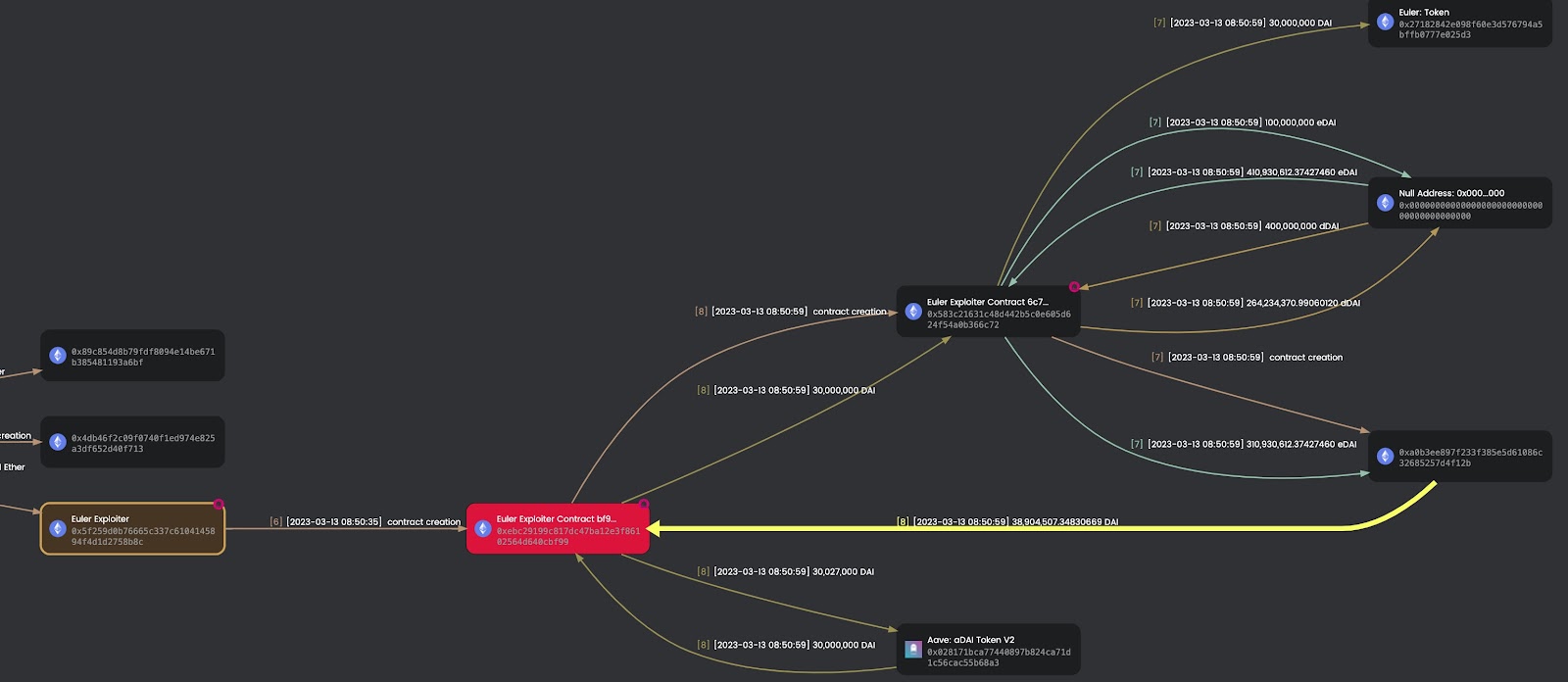

Movement of funds from Euler Finance. Source: Meta Seluth

ZachXBT, another well-known on-chain investigator, confirmed the correlation and stated that the attack’s fund movement and approach bear striking similarities to those of bad actors who recently targeted a BSC-based protocol.

In the previous attack, the attackers deposited the funds into Tornado Cash, a cryptocurrency mixer. Presently, the illicitly obtained funds are residing in the following hacker-controlled addresses:

0xebc29199c817dc47ba12e3f86102564d640cbf99 (Contract) – 8,877,507.34 DAI

0xb2698c2d99ad2c302a95a8db26b08d17a77cedd4 – 8,080.97 ETH

0xb66cd966670d962c227b3eaba30a872dbfb995db – 88,752.69 ETH & 34,186,225.91 DAI

Euler Finance has acknowledged the exploitation and reported that they are working closely with security experts and law enforcement agencies to address the matter.

According to Slowmist, a blockchain security firm that conducted an in-depth analysis of the attack, the attacker utilized flash loans to deposit funds and then proceeded to trigger liquidation by leveraging them twice. After donating the funds to the reserved address, the exploiter performed a self-liquidation to obtain any remaining assets.

The exploit’s success can be attributed to two key factors. Firstly, the funds were donated to the reserved address without undergoing a liquidity check, resulting in a soft liquidation. Secondly, the soft liquidation logic was activated by high leverage, allowing the liquidator to acquire most of the collateral funds from the liquidated user’s account by only transferring a portion of the liabilities to themselves.

The entire process occurred within a single transaction (one per pool) using flash loans obtained from AAVE.

It seems that one of the smart contracts in Euler has a glitch where it fails to verify the health factor during the execution of the donateToReservers() function. As a result, the attacker could liquidate their position from the protocol, repay the flash loan, and generate a substantial profit.

In a funding round last year, Euler Finance secured $32 million in investments from notable entities such as FTX, Coinbase, Jump, Jane Street, and Uniswap. Euler Finance garnered significant attention for its liquid staking derivatives (LSDs) offerings, which enable stakers to unlock liquidity for staked cryptocurrencies like Ether and potentially increase their returns. LSDs are a relatively new type of token, and they now account for up to 20% of the total value locked in decentralized finance protocols.

Today the Euler Foundation is launching a $1M reward in the hope that this provides additional incentive for information that leads to the Euler protocol attacker’s arrest and the return of all funds extracted by the attacker.

Silvergate Capital Corporation has revealed that it will close its operations due to “recent industry and regulatory developments”. The company confirmed that the liquidation of Silvergate Bank would involve the complete repayment of all customer deposits.

This decision follows the withdrawal of support by various crypto companies, including Coinbase, Paxos, Gemini, BitStamp, and Galaxy Digital, following an investigation into Silvergate’s alleged participation in the collapse of FTX. The bank also announced the closure of its exchange network on March 3, stating that the decision was based on risk considerations.

Silvergate had established itself as a significant banking partner for several crypto companies. However, apprehensions about its financial stability arose when it announced a two-week delay in filing its annual 10-K report, which typically offers a summary of the company’s financial position.

The departure of Silvergate has left the potential impact on other crypto companies that have funds held by the bank or have exposure to it uncertain. The bank stated that the transfer volume of customer fiat deposits had decreased by approximately $50 billion in Q3 of 2022 compared to the corresponding period in 2021.

Debate over Silvergate’s downfall and the future of crypto banking

The collapse of Silvergate bank sparked a debate over who was responsible for the chain of events that led to its downfall. After the bank’s voluntary liquidation announcement, numerous reactions from lawmakers, crypto analysts, executives of crypto firms, and commentators appeared on social media.

Some lawmakers in the United States have seized the opportunity to comment on the crypto industry, characterizing it as a “risky, volatile sector” that poses a risk to the broader financial system.

Senator Elizabeth Warren has referred to Silvergate’s collapse as “disappointing but predictable,” urging regulators to take action against the risks associated with crypto.

As the bank of choice for crypto, Silvergate Bank's failure is disappointing, but predictable. I warned of Silvergate's risky, if not illegal, activity—and identified severe due diligence failures. Now, customers must be made whole & regulators should step up against crypto risk.

Senator Sherrod Brown expressed his apprehension about banks that engage with cryptocurrencies. In his opinion, they pose a potential risk to the financial system.

The senator emphasized the need for robust safeguards to protect the financial system from the dangers associated with crypto. The senator’s comments have drawn criticism from some members of the community who argue that the issue was not caused by crypto but instead by fractional-reserve banking. They point out that Silvergate held considerably more in-demand deposits than cash reserves, which they believe was the primary factor behind the bank’s troubles.

.@SenSherrodBrown, you’re wrong that #crypto triggered Silvergate’s issue. What did it was $13.3bn in demand deposits that depositors cld withdraw in minutes, but only $1.4bn of cash. Had $SI held $13.3bn of cash, the bank run wouldn’t have impaired its capital. Not a crypto… https://t.co/nGlfHwUcBN

Some companies have taken the opportunity to reaffirm their dissociation from the bank. Binance CEO Changpeng Zhao said on Twitter that the crypto exchange does not have any assets stored with Silvergate. Likewise, Coinbase issued a similar statement.

Update: We’re sorry to see Silvergate make the tough decision to wind down their operations. They were a partner & contributors to the growth of the cryptoeconomy. Coinbase has no client or corporate cash at Silvergate. Client funds continue to be safe, accessible & available. https://t.co/78oMrLQ6VH

On the other hand, Nic Carter, the co-founder of Castle Island Ventures and Coin Metrics, a crypto intelligence firm, opined that the government was responsible for “accelerating the collapse” of Silvergate. Similarly, Ram Ahluwalia, the CEO of Lumida, a financial services company, shared a similar perspective, asserting that a letter from a senator had eroded public confidence in Silvergate, resulting in a bank run. He argued that the bank was denied due process.

Previously, Carter mentioned the existence of “Operation Choke Point 2.0.” He claimed that the U.S. government is utilizing the banking sector to orchestrate “a sophisticated and extensive crackdown on the crypto industry.”

However, some individuals think that the downfall of Silvergate might not necessarily have an adverse impact on the crypto industry. Instead, they believe that combined with proposed tax law changes, it could intensify the departure of crypto firms from the United States.

– Silvergate winding down operations in light of “regulatory developments” – Proposed changes to capital gains – Proposed elimination of tax loss harvesting

none of these are bad for crypto…

they’re just reasons for passionate builders to operate outside the US

In the wake of Silvergate’s liquidation, there has been a growing concern about where crypto firms will turn to for their banking needs.

Coinbase, which previously accepted payments through Silvergate, announced on March 3 that it would be facilitating cash transactions for institutional clients using its other banking partner, Signature Bank.

However, Signature Bank had disclosed in December its intentions to lower its exposure to the crypto sector by decreasing deposits from clients holding digital assets.

In a bid to further diminish its crypto exposure, Signature imposed a minimum transaction limit of $100,000 on transactions processed through the SWIFT payment system on behalf of Binance.

The market is down

Given the liquidation of Silvergate Bank, the cryptocurrency market has experienced a decline. The other factors involved in this downfall include the lawsuit against KuCoin exchange, and comments from the United States Federal Reserve chair Jerome Powell that have worried investors.

Bitcoin is giving signs of a bearish future, and the crypto Twitter community talks of a potential bottom at $12,000. Ether has also experienced a decline.

The expectation of interest rate hikes and a softening economy weighs on risk assets, and Powell’s comments regarding a possible uptick in inflation have added to investor concerns.

The uncertainty regarding crypto regulation has led to market volatility, and the liquidation of Silvergate Bank is expected to make regulators keep an even closer eye on the sector.

Banks are already implementing robust anti-money laundering measures in preparation for further crypto regulation. While the crypto market had a strong start to 2023, investors’ appetite for risk is likely to remain muted until there is more transparency regarding the roadmap for crypto industry regulation and signs that U.S. inflation has peaked.

Ajay Kumar Choudhary, the executive director of the Reserve Bank of India (RBI), has revealed that the recently launched digital rupee, India’s in-house central bank digital currency (CBDC), is undergoing offline functionality testing.

Apart from evaluating its offline capability, the Reserve Bank of India (RBI) is assessing the potential of CBDCs for cross-border transactions and their integration with legacy systems of other nations.

The wholesale segment pilot was launched by the RBI on November 1, 2022, with 50,000 users and 5,000 merchants onboarded for real-world testing. As of the end of February 2023, around $134 million and 800,000 transactions have been completed via wholesale CBDCs.

In addition to offline functionality, the RBI is also exploring the CBDC’s potential for cross-border transactions and its linkage with the legacy systems of other countries. Choudhary stated that the RBI is eagerly anticipating the participation of private sectors and fintechs in CBDC, especially on offline and cross-border transactions.

Furthermore, the banks’ executive stated that the CBDC would soon become the medium of exchange. That’s why it needs all features of physical currency, including its anonymity.

The launch of CBDC is India’s motivation for improving regional financial inclusion and leading the digital economy. CBDC would also eventually replace cryptocurrencies, as per Choudhary’s statement on behalf of the RBI.

India’s CBDC for remittances

India’s national payment network, the Unified Payments Interface (UPI), has expanded its services to Singapore as of February 21, 2023.

The integration of UPI with PayNow enables citizens of both countries to transfer funds across borders with great speed.

The facility was launched by Shaktikanta Das, Governor of the Reserve Bank of India, and Ravi Menon, Managing Director of the Monetary Authority of Singapore, through token transactions using the UPI-PayNow linkage.

This integration of UPI with PayNow will allow users from India and Singapore to transfer money across borders with great speed. Users can send or receive money from India using only a UPI-id, cellphone number, or virtual payment address for money held in bank accounts or e-wallets. UPI’s instant real-time payment system allows for immediate cash transfer between the two bank accounts via a mobile interface.

UPI goes Global!

Since UPI was introduced as a payment system in India, it has revolutionised the lives of Indians, but in fact, India’s digital payment system is steadily becoming globally attractive & is being adopted by other countries.#indiafirst#IndiaSingaporeRelationspic.twitter.com/55sGh5bzbZ

Initially, four major Indian banks, namely State Bank of India, Indian Overseas Bank, Indian Bank, and ICICI Bank, will support outgoing remittances. Incoming remittances will be facilitated by Axis Bank and DBS Bank India. Users in the region will have access to the service through Singapore’s DBS Bank and Liquid Group.

ICICI Bank is one of the participants in India’s central bank digital currency (CBDC) program.

According to Sathvik Vishwanath, CEO of Indian crypto exchange Unocoin, this integration of UPI with PayNow is a valuable addition to India’s payment rails. As close to 30% of Singapore’s population consists of expatriates, and they send money to India once a month or quarter, this integration eliminates friction, reducing the processing time and costs.

While India’s digital payment infrastructure has expanded significantly over the last few years due to COVID-19, the government remains skeptical about cryptocurrencies. The government imposed a 30% tax on crypto gains, forcing major players to relocate from the country. However, the government is eager to utilize blockchain technology for its CBDC program and intends to use existing infrastructure to scale the CBDC program.

But India is in no hurry to push out CBDC

Despite joining the CBDC race a few months ago, the Indian government is in no hurry to rush its central bank digital currency (CBDC) pilot. As per a report by The Economic Times on Feb. 8, India’s digital rupee pilot, launched by the Reserve Bank of India (RBI), has attracted 50,000 users and 5,000 merchants.

At a press conference, RBI Deputy Governor Rabi Sankar announced the first public milestones of India’s digital currency and emphasized the government’s plan to proceed with CBDC testing in the smoothest way possible. Sankar stated that the RBI doesn’t want to push CBDC developments without having a full understanding of its potential impact.

Furthermore, Sankar noted that the RBI has set targets in terms of users and merchants and plans to go slowly with the CBDC testing. He stated that they want the process to happen gradually and slowly and that they are in no hurry to make something happen so quickly.

The latest announcement is in line with data from an official digital rupee application, which indicates that the pilot has reached its capacity for users. As per the data from the digital rupee app by the ICICI Bank, India’s CBDC program is full at present, suggesting that more users will be able to join the trial at a later date.

India’s CBDC development came after countries like China aggressively rolled out digital currency in April 2020. However, despite significant efforts to promote the use of CBDCs, some former central bank officials claimed that the digital yuan’s usage has been low.

The CEO of Kraken, Jesse Powell, has accused U.S. regulators of enabling “bad actors” in the cryptocurrency industry to grow to an enormous size at the expense of legitimate players.

In a recent tweet, Jesse Powell, present a personal idea about the true intentions of the regulators:

I have a theory: Regulators let the bad guys get big and blow up because it serves their agenda.

1. destroy capital/resources in crypto ecosystem 2. burn people, deter adoption 3. give air cover to attack good actors

Jesse Powell has claimed that regulators, including the Securities and Exchange Commission (SEC), are allowing crypto companies to operate without enforcement actions as a distraction from their real targets.

Many of the respondents agree and offer personal perspectives on why the regulators are more interested in pursuing their secret politics than in offering a safe investment environment for individuals.

Powell argues that this could lead to the destruction of the industry by allowing bad actors to dominate the market, while legitimate players are forced to compete for dwindling resources. According to Powell, regulators will simply jail violators later after the damage has already been done.

Jesse Powell, the CEO of Kraken, has claimed that U.S. regulators are favoring “bad guys” over “good guys” in the cryptocurrency industry and that the legitimate players are being treated as enemies. Powell warned that if the bad actors are allowed to run unchecked, they could potentially wipe out the legitimate players. Powell made these statements after Kraken settled with the SEC by agreeing to discontinue staking services and pay a $30 million settlement.

Many in the crypto community have criticized the SEC for its “regulation by enforcement” approach, which has also targeted celebrities endorsing tokens on social media.

In September 2022, Powell announced that he would be stepping down as CEO and transitioning to the position of chair of the board, while Kraken’s chief operating officer, Dave Ripley, would take over as CEO.

Meanwhile, Paxos is also reportedly facing SEC enforcement action for alleged violations of investor protection laws related to the Binance BUSD stablecoin.

SEC vs Kraken’s crypto staking option

Following the settlement with Kraken, Gary Gensler, the Chair of the United States Securities and Exchange Commission (SEC), has issued a warning to other cryptocurrency companies to comply with the law.

Gensler emphasized that crypto exchanges must register with the SEC to operate within the regulations of the U.S. He claimed that many companies in the industry are deliberately avoiding registration. Gensler pointed out that the business models of many crypto projects are full of conflicts and urged them to separate bundled products. Gensler stressed the need for time-tested rules and laws to protect investors and prevent companies from misusing their customers’ funds. He warned companies against having their “hand in the customer’s pocket.”

Gensler made this statement in response to the SEC’s settlement with Kraken, where the exchange agreed to cease staking services and programs for its U.S. customers and pay a $30 million settlement.

Kraken announced that it would still offer staking services to non-U.S. users through a subsidiary.

The SEC’s actions have been met with criticism from many in the industry, who argue that firms are being punished for operating in a regulatory environment with unclear guidelines.

SEC Commissioner Hester Peirce has criticized the regulator’s actions, calling them “lazy and paternalistic,” and pointing out that the staking program had been beneficial to its users.

The recent SEC lawsuit against Paxos over Binance USD (BUSD) has caused confusion and debate among the cryptocurrency community.

The U.S. Securities and Exchange Commission (SEC) issued a wells notice to Paxos. They claim that BUSD is an unregistered security, which resulted in the New York Department of Financial Services (NYDFS) ordering the halt of BUSD issuance.

This has led to a range of reactions from the crypto community, with some members dismissing it as fear, uncertainty, and doubt (FUD), while others view it as an attack on the Binance exchange.

The community is split on their thoughts about the situation, with some saying that those who bought the stablecoin were not expecting it to increase in value.

The crypto community on Twitter started to talk about this controversy, but they seem to agree that nobody would buy a stablecoin and anticipate a profit. Others expressed confusion about the development, questioning how BUSD can be considered a security and asking their followers if they expected its value to reach $2.

Some even took it more personally, attacking SEC chairperson Gary Gensler, suggesting that he is on an “unhinged, unchecked crusade against crypto.”

However, some dismissed the news as FUD and pointed out that BUSD is fully backed and the halt in issuance by Paxos will not affect existing tokens. They encouraged everyone to stay informed but advised against making emotional decisions. A few voices have also pointed out the urgent need for a stablecoin registry framework.

Bitcoin analyst Tedtalksmacro also expressed similar thoughts, suggesting that BUSD may not meet the criteria of a security. The analyst hinted that the situation might just be a way to target Binance.

The SEC claims that BUSD is an unregistered security and is suing it's issuer Paxos 🚩

To be considered a security, the Howey Test is used… I don't think BUSD meets the criteria, it's a damn stablecoin!?

It’s important to understand that despite stablecoins being designed to have a fixed value, their holders can still generate profits through methods such as arbitrage, hedging, and staking.

What is BUSD?

BUSD is a stablecoin co-founded by Paxos and Binance. Paxos leverages blockchain technology to provide its Stablecoin as a Service product to other companies.

The company has also previously developed a stablecoin backed by gold, known as PAX Gold (PAXG). Both BUSD and PAXG tokens fall under the jurisdiction of the New York State Department of Financial Services.

BUSD is a fiat-backed stablecoin, pegged to the U.S. dollar. Paxos holds an equivalent amount of U.S. dollars in FDIC-insured banks or backed by U.S. Treasuries, serving as the reserves for the total supply of BUSD.

The price of BUSD adjusts in equal amounts to the changes in the value of the U.S. dollar.

Binance’s CEO still supports BUSD

Binance CEO Changpeng Zhao, also known as “CZ,” announced that the exchange would continue to support Binance USD (BUSD), despite the announcement made by the SEC that argues that BUSD is an unregistered security.

Changpeng Zhao (CZ), CEO of Binance, has reassured users that their funds are secure despite regulatory enforcement.

However, he stressed the fact that Paxos, regulated by NYDFS, fully owns and manages BUSD.

Paxos will continue to manage BUSD, including redemptions, and its reserves have been audited by multiple parties, according to Zhao. He acknowledged that the enforcement action might cause a decrease in BUSD’s market cap over time. But Binance will consider alternative non-USD-based stablecoins.

Despite this, Binance will remain supportive of BUSD on the exchange, though it acknowledges that some users may switch to other stablecoin tokens due to the enforcement.

CZ also explained that Paxos, the issuer of the Binance USD (BUSD) stablecoin, is regulated by the New York State Department of Financial Services. He has made assurances of its reserves, which have been audited by multiple parties.

Zhao also acknowledged that the actions taken by the SEC and NYDFS could have a significant impact on the future development of the cryptocurrency ecosystem. He warned of the potential implications if BUSD is ruled as a security by the courts.

Given the regulatory uncertainty in certain markets, Binance may also review other projects to ensure the safety of its users. This comes after a number of cryptocurrency service providers, and tokens have faced enforcement actions by American regulators, including Ripple’s ongoing legal battle with the SEC over XRP being an unregistered security. Kraken also ceased its staking services to U.S. clients and paid a $30 million settlement to the SEC for failing to register its crypto asset staking program.

Binance, the cryptocurrency exchange, has introduced Binance Tax, a tax reporting tool, in preparation for the tax season.

Binance Tax is a tool that helps users access information on their crypto activity to comply with local regulations. It allows users to download a tax summary report that includes details of their gains and losses throughout the year, including spot trades, crypto donations, and fork rewards.

Currently, the Binance Tax tool is only available for Binance platforms, but the company intends to integrate with other platforms in the future.

Taxes in crypto

The launch of Binance Tax follows recent global regulatory crackdowns on the crypto industry, with regulators focusing on investor protection and compliance with local standards. Currently, only Binance users located in Canada and France have access to Binance Tax. Binance mentioned that are actively working to expand support to additional regions and include support for more networks and wallets beyond Binance.

In the US, the Securities and Exchange Commission has called for firms to disclose their exposure to crypto risks. It has reintroduced a bill to allow companies to apply for compliance agreements with federal agencies.

This move by Binance aims to ensure its users are prepared for the upcoming tax season and stay on top of their tax obligations.

One month prior to the launch of Binance Tax, the exchange joined an association to improve compliance with global sanctions.

In the past year, regulatory agencies worldwide have increased their control over the crypto industry, particularly after the FTX crisis. For instance, the Securities and Exchange Commission in Thailand plans to implement stricter rules for the crypto industry with a focus on protecting investors.

Regulators in South Korea, the Netherlands, and the US have been investigating exchanges for non-compliance issues, with some exchanges, such as Kraken, being forced to settle with the US Treasury’s Office of Foreign Assets Control.

In December 2022, the US SEC asked companies to reveal any exposure to crypto bankruptcies and risks. Additionally, a bill was reintroduced by a House committee chair to allow companies to apply for compliance agreements with federal agencies for crypto innovation.

What happened to the crypto regulatory landscape in 2022?

Regulations in the crypto world were once seen as an obstacle to adoption, but they are now seen as a means to gain global mainstream acceptance. In 2022, crypto businesses saw broader acceptance from regulators worldwide, with many being granted operational licenses and access to new markets. However, the collapse of crypto firms like Terraform Labs, FTX, and Celsius had a negative impact on the industry’s reputation with regulators and investors.

North America

In North America, the US became the leader in crypto disruption after China’s ban on crypto mining and trading in 2021. The US is home to the largest crypto ATM network and is the highest contributor to the Bitcoin hash rate. NFTs received significant attention in US politics, with the FEC permitting their use for political campaign fundraising.

Canada banned crypto leverage and margin trading after the FTX collapse, and the US introduced the Crypto-Asset Environmental Transparency Act to report on the energy use and environmental impact of crypto miners.

South America

El Salvador remains the biggest contributor to mainstreaming Bitcoin, with President Nayib Bukele announcing a new BTC investment strategy. Brazil also saw pro-crypto regulation, with a bill signed into law legalizing the use of crypto as a payment method and a Payment Institution License issued to Crypto.com.

Asia

Asia saw numerous regulators soften their anti-crypto stance and allow crypto businesses to operate. China loosened its crypto ban, and the Shanghai High People’s Court recognized Bitcoin as property with the right to compensation in a loan case. India imposed two new crypto tax policies, but during its G20 presidency, it plans to develop standard operating procedures for cryptocurrencies.

Pakistan’s central bank signed new laws to launch a central bank digital currency. South Korea spent much of 2022 tracking down those responsible for investor losses from Terraform Labs, but also saw a reduction in hacking activities after implementing Know Your Customer (KYC) requirements.

Europe

The European Union‘s Committee of Permanent Representatives has approved a framework for regulating cryptocurrencies, known as the Markets in Crypto-Assets framework, to ensure consistent regulation among EU member states. The International Monetary Fund, a UN financial agency, has called for greater regulation of African crypto markets. Meanwhile, the Central African Republic has reportedly passed a bill to legalize the use of cryptocurrencies in finance.

In the United Kingdom, the government is seeking to tighten regulation of the crypto industry. In response to the FTX collapse, the country’s HM Treasury has issued guidelines for the Financial Conduct Authority to monitor crypto companies and their advertising. This has further influenced an upcoming 2023 legislation to restrict foreign crypto services from operating in the UK.

Africa

In South Africa, the Financial Sector Conduct Authority has updated its 2002 Financial Advisory and Financial Intermediary Services Act to declare crypto as a financial product subject to financial services laws. Nigeria has banned ATM cash withdrawals of over $225 (100,000 nairas) per week to promote the use of its CBDC, the eNaira. African crypto exchange Yellow Card has received regulatory approval to expand its services across Africa.

The Dubai Virtual Assets Regulatory Authority issued operational approvals to crypto businesses in 2022, but had to revoke the Minimum Viable Product license from FTX MENA.

Australia has become the fourth largest crypto ATM hub, overtaking El Salvador, following the US, Canada, and Spain. Australian financial regulators continue their efforts from 2022 to create a regulatory framework for stablecoins.

Movement of funds from Euler Finance. Source: Meta Seluth

Movement of funds from Euler Finance. Source: Meta Seluth