Bitcoin miners are nearing capitulation due to shrinking profit margins and increased BTC sell-offs. Since the halving, miners have seen a 63% drop in daily revenues. As a result, miners are forced to sell their reserves.

According to CryptoQuant, a market intelligence firm, Bitcoin miners are showing signs of giving up, similar to what happened after the FTX crash in late 2022. This could mean that Bitcoin (BTC) might be reaching a low point.

Miner capitulation means some miners are reducing their operations or selling some of their Bitcoin to stay in business or manage their risks.

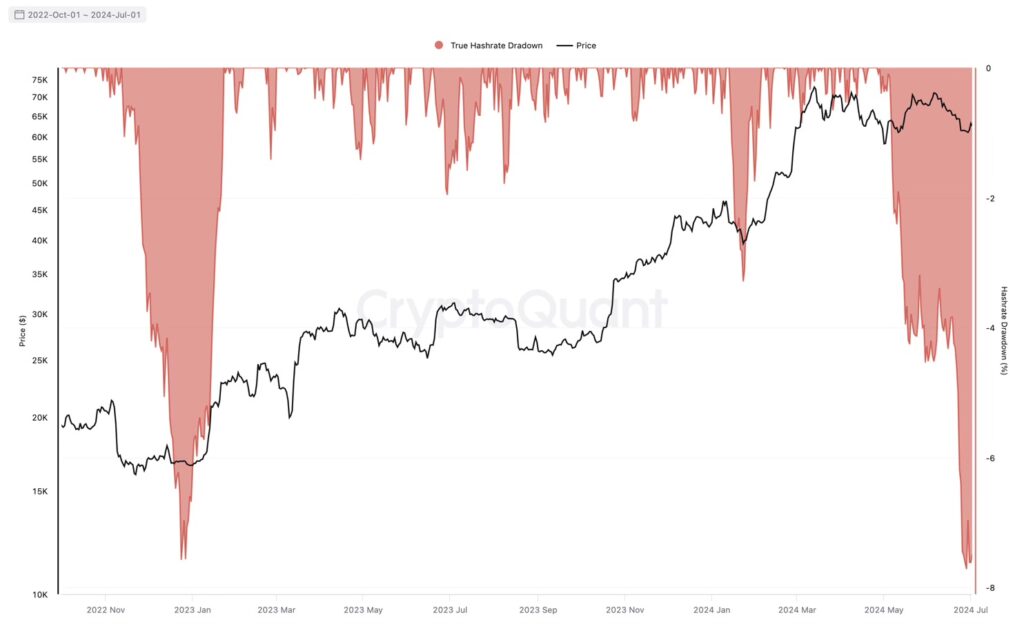

During this time, Bitcoin’s price dropped by 13%, from $68,791 to $59,603. One major sign is a drop in Bitcoin’s hash rate, which is the total computing power that secures the Bitcoin network.

This situation is very similar to late 2022, when the market hit rock bottom after the FTX crash.

The CryptoQuant graphic shows several signs that miners are struggling. One major sign is a 7.7% drop in the hash rate since the halving, indicating that it’s becoming harder for miners to continue their work. The hash rate, which measures the total computing power of the Bitcoin network, usually falls when the market is doing poorly. Now, the hash rate has reached a four-month low of 576 EH/s after hitting a record high on April 27.

This suggests that miners might face even tougher times ahead, but it could also mean good opportunities for investors looking to buy Bitcoin at a lower price.

Early signs of miner capitulation

When bitcoin miners start to give up, savvy investors often see it as a good time to buy. This is because when miners have to sell their BTC to cover costs, it pushes the price down.

However, this sell-off can also mean the market is hitting its lowest point, setting the stage for a possible recovery. Data from CryptoQuant shows that miners are selling their Bitcoin reserves faster than before.

Daily BTC outflows from miners’ wallets are at their highest since May, showing a big sell-off.

This trend suggests that miners, struggling with falling revenues, would rather sell their assets than keep operating at a loss.

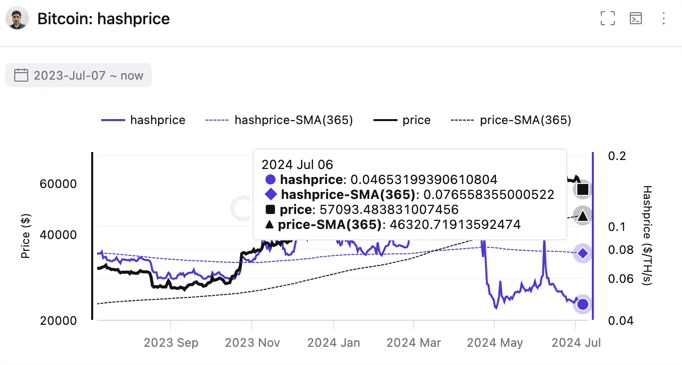

The “hash price,” which measures how much miners earn per unit of computing power, has also fallen to very low levels. Right now, the average revenue per hash is $0.046 per EH/s, just slightly above the all-time low of $0.045.

This drop in profitability makes things even harder for miners, forcing them to shut down operations and sell their bitcoins, adding more pressure on the market.

As miners give up, bitcoin might find a new bottom before bouncing back.

Bitcoin’s hashrate decline

Notably, the 7.7% decline in hashrate is similar to what happened in late 2022, when Bitcoin’s price hit a low of $15,500 before rising over 300% in the next 15 months.

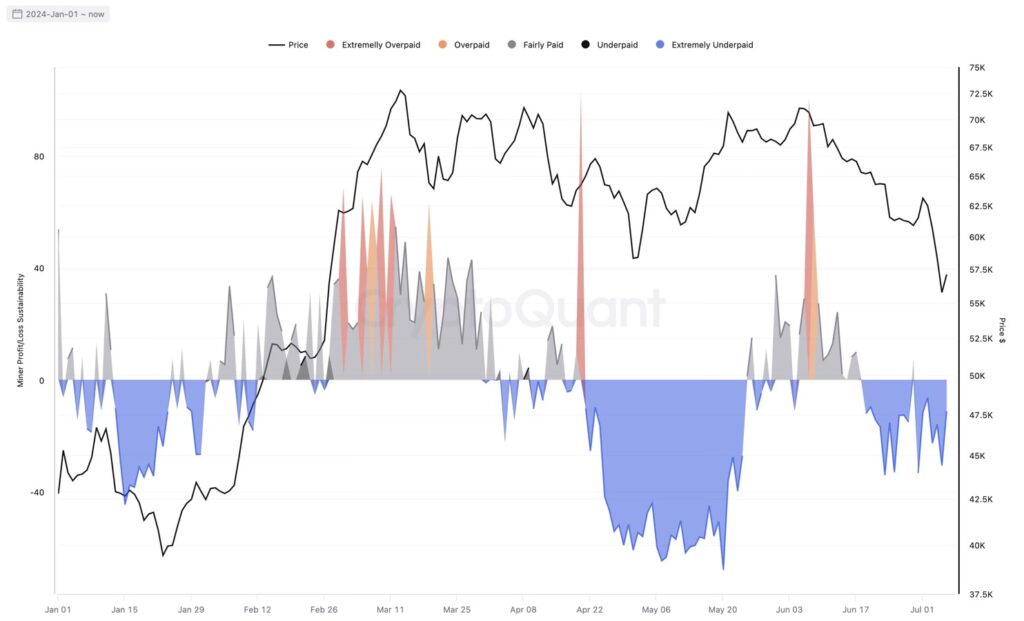

The CryptoQuant report mentioned that since the halving, miners have been extremely underpaid, as shown by the miner profit/loss sustainability indicator.

As a result, miners have seen a 63% drop in daily revenues since the halving when both Bitcoin’s block rewards and transaction fees were higher.

Total daily revenues have decreased from $79 million on March 6 to $29 million now.

Additionally, revenue from transaction fees has dropped to only 3.2% of the total daily revenues, the lowest since April 8.

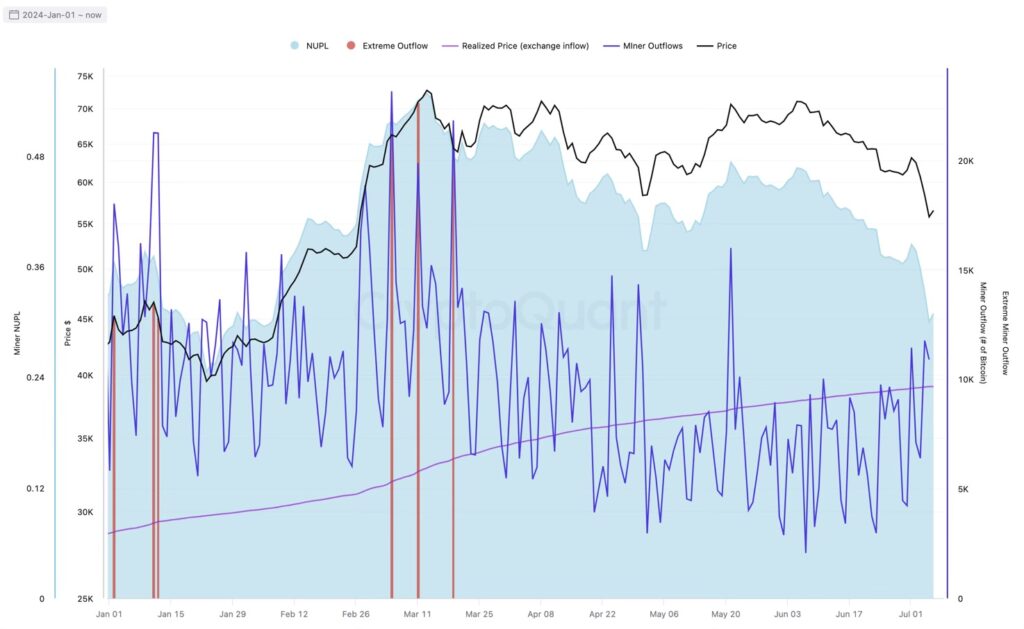

Source: Daily Bitcoin miner outflows, CryptoQuant

Due to these decreased revenues, Bitcoin miners have had to use their reserves to earn yield. Daily miner outflows have surged to the highest level since May 21, suggesting they might be selling their BTC reserves.

This sell-off by miners, along with sales from Bitcoin whales and national governments, has contributed to Bitcoin’s recent price drop, reaching a four-month low of $53,499 on July 5.

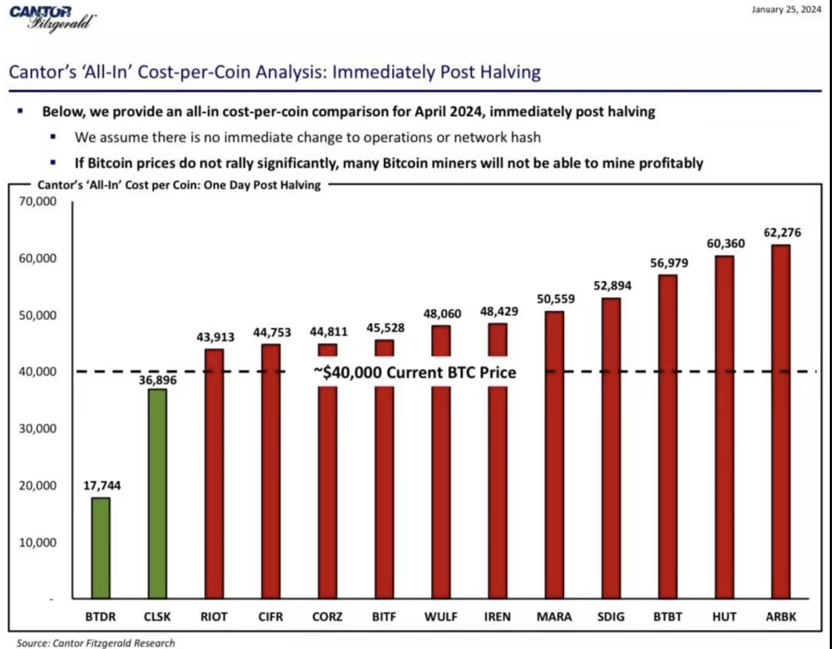

An earlier report by financial services firm Cantor Fitzgerald noted that some of the world’s largest mining companies might be forced to give up if Bitcoin’s price falls to $40,000, highlighting the tough situation for the mining industry.

Bitcoin has recently experienced significant sell-side pressure, leading to a substantial price drop and declining investor confidence.

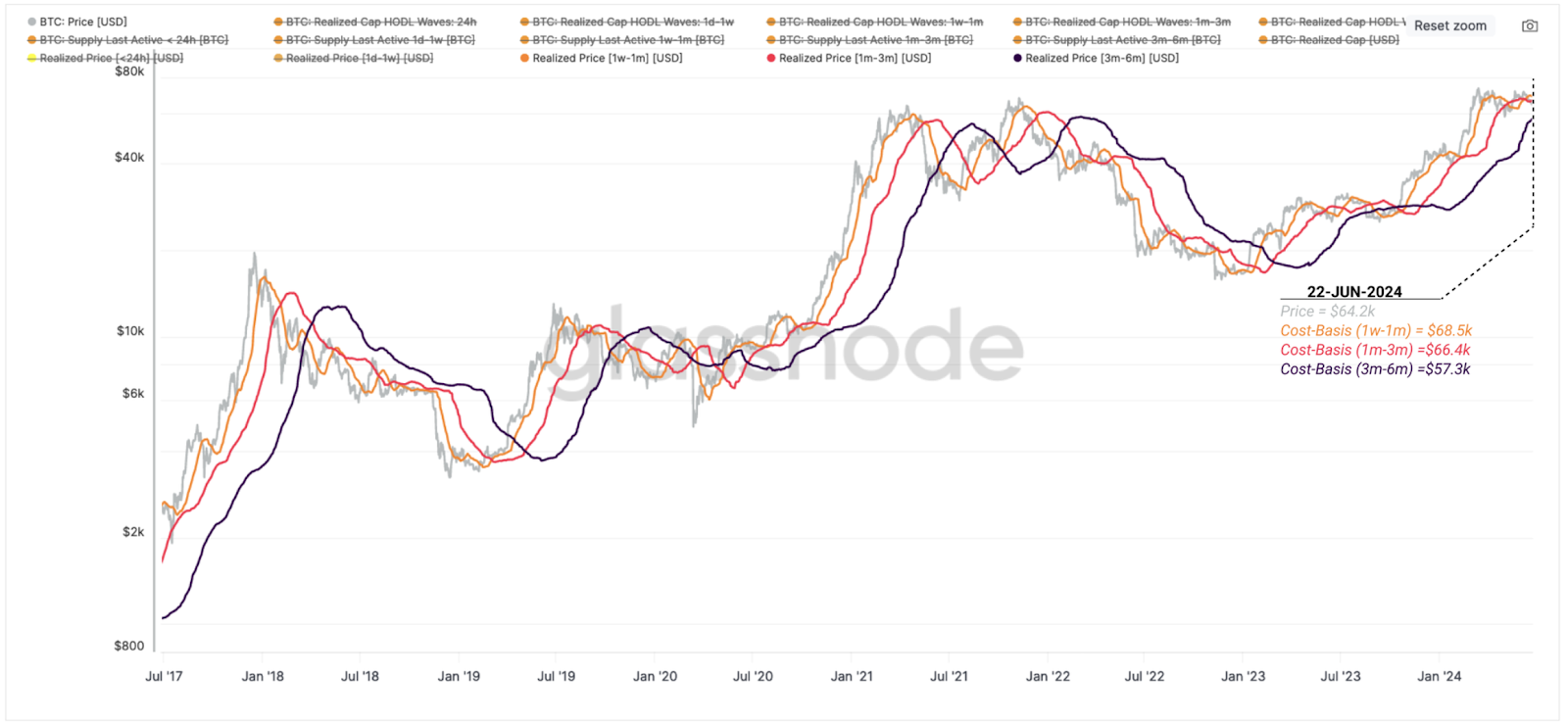

Bitcoin‘s price has faced increasing sell-side pressure, causing it to drop by over 5.5% in the past week, reaching a six-week low of $58,400 on June 25. According to market intelligence firm Glassnode, this decline pushed BTC below its short-term cost basis, indicating a potential for a deeper correction.

What is the cost basis?

The cost basis is the original value or purchase price of an asset. In this context, it helps determine whether Bitcoin holders are currently in profit or loss.

“Since mid-June, the spot price has fallen below the cost basis for both 1-week to 1-month holders ($68.5k) and 1-month to 3-month holders ($66.4k),” Glassnode reported in its “Week On-chain” newsletter published on June 25. “If this trend continues, it could lead to a further decline in investor confidence, making the correction deeper and recovery slower.”

Bitcoin realized price by cohort. Source: Glassnode

The short-term holder (STH) cost basis, or realized price, is a metric that indicates the average purchase price of Bitcoin for investors who have held their coins for less than 155 days.

Understanding investor behavior is crucial in assessing the dynamics of the Bitcoin market.

Short-term holders, those who have kept their coins for less than 155 days, tend to react more quickly to market fluctuations.

When Bitcoin’s price falls below its average purchase price or cost basis, it often triggers panic selling as these investors seek to minimize their losses.

This can lead to a cascading effect, further driving down the price.

In contrast, long-term holders who have held their coins for more than 155 days typically have a higher cost basis and are more resilient to short-term price volatility. Their investment strategies are often rooted in long-term growth expectations, making them less likely to sell during market downturns.

The recent market trends highlight a worrying shift in investor sentiment.

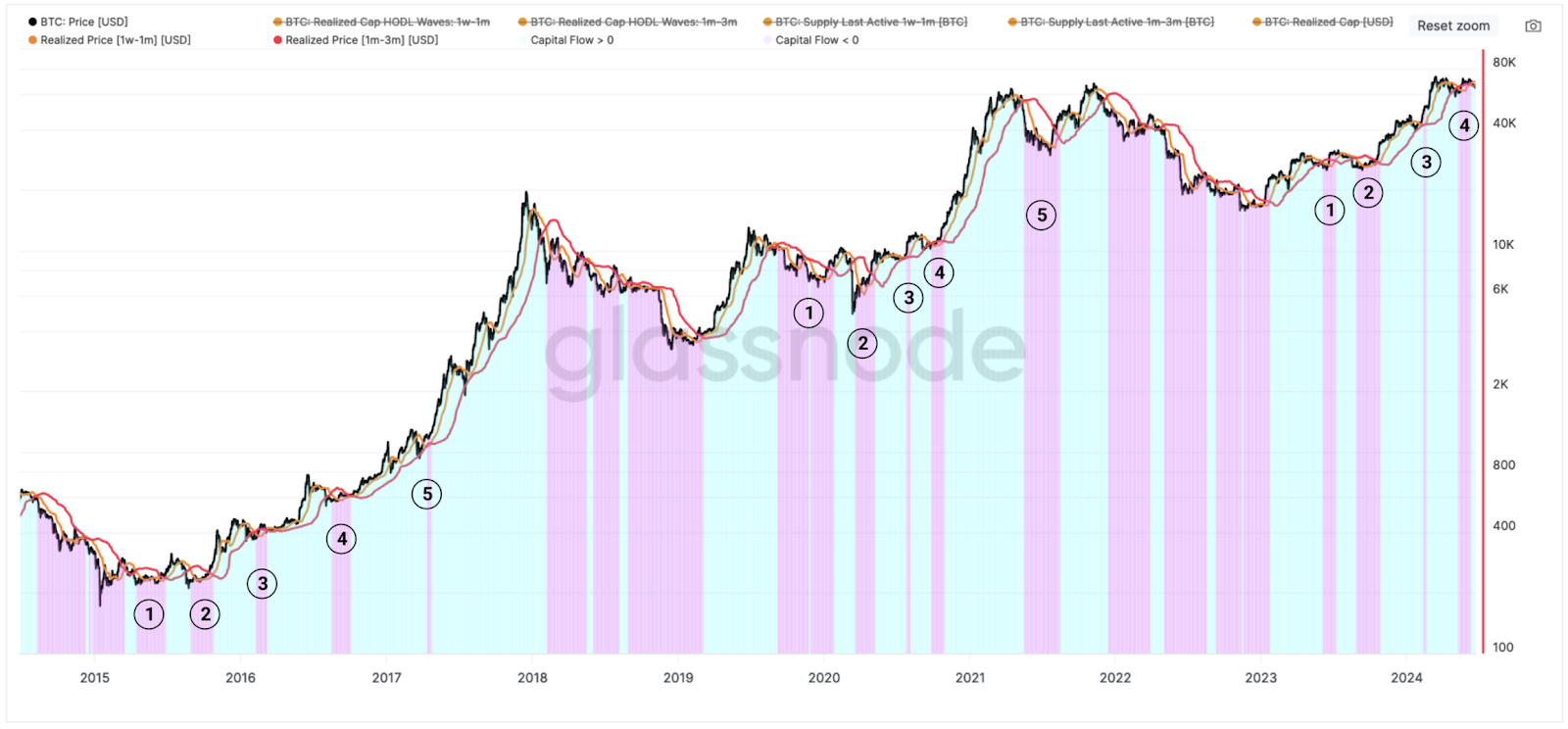

The fact that the cost basis for short-term holders has fallen below that of mid-term holders (1 to 3 months) signals weakening demand and a net outflow of capital from Bitcoin.

Such a structure has historically led to deeper corrections and prolonged recovery periods. The current market environment, characterized by significant outflows from Bitcoin ETFs and a general decline in investor confidence, mirrors patterns observed in previous market cycles where similar negative capital flows resulted in substantial price declines.

According to data from LookIntoBitcoin, when BTC dropped below the $64,000 mark on June 23, it fell below the STH realized price, which was $64,591 at that time.

Furthermore, the recent price drop nearly brought Bitcoin below the cost basis for holders of 3 to 6 months, which is $57,300.

This cost basis is still increasing despite the falling price. The report also notes that the cost basis for 1-week to 1-month holders has fallen below that of 1-month to 3-month holders. This indicates a decline in demand and a net capital outflow from Bitcoin.

Investor confidence and market trends

“During previous bull markets, a negative capital flow structure has happened up to five times. This pattern has been present since May and continued into early June,” the Glassnode report states.

Spot Bitcoin ETFs are experiencing an increase in inflows. On June 25, the 10 U.S.-based spot Bitcoin exchange-traded funds (ETFs) saw inflows totaling $31 million, breaking a seven-day streak of outflows.

According to SoSo Value, Fidelity’s ETF FBTC led the way with $49 million in net inflows on June 25. It was followed by the Bitwise Bitcoin ETF BITB, which saw $15 million in inflows, and the VanEck Bitcoin Trust ETF HODL, which had $4 million in net inflows.

Total Bitcoin spot ETF net inflow. Source: SoSo Value

Contrasting Trends in ETFs

On the other hand, the Grayscale ETF GBTC experienced a single-day outflow of $30.2 million, while the ARK 21Shares Bitcoin ETF saw $6 million in net outflows.

As of the end of June 2024, the ten spot Bitcoin funds that started trading on January 11 have accumulated net inflows of $14.42 billion, managing over $53.56 billion in assets. The significant outflows observed over the past few weeks are the highest since April, when spot Bitcoin ETFs recorded net outflows exceeding $1.2 billion between April 24 and early May.

The rehabilitation trustee of Mt. Gox has announced that repayments in Bitcoin and Bitcoin Cash will commence in July 2024. Creditors have been waiting for over a decade to recover their funds.

The long-awaited repayment process will start in July 2024 for the creditors of the now-defunct Mt. Gox cryptocurrency exchange, which lost 850,000 Bitcoin in 2014.

Mt. Gox, once a pioneering cryptocurrency exchange, handled over 70% of global blockchain trades. In 2014, the platform abruptly went offline following a security breach that led to the loss of more than 850,000 BTC, valued at over $51.9 billion at today’s prices. This event caused Bitcoin’s price to plummet to a local low of $420 in February 2014.

The exchange had suffered multiple hacks between 2011 and 2014, severely undermining its security. Although the Mt. Gox rehabilitation trustee has announced plans for repayments, the process has faced numerous delays. The most recent deadline was set for September 2023, just before the previously scheduled repayment date of October 31, 2023. Despite the upcoming repayment plans, there remains uncertainty about further delays.

Plans for repayment

The rehabilitation trustee for Mt. Gox will begin processing repayments in Bitcoin and Bitcoin Cash starting in July 2024, as stated in a notice from the exchange on June 24. According to the announcement, repayments will be made to cryptocurrency exchanges where the required information for implementing the repayments has been verified and confirmed.

The trustee has urged users to remain patient, explaining that the order of payments will depend on the completion of information verification with each cryptocurrency exchange. Users are asked to wait until these repayments are processed.

Mt. Gox owes over $9.4 billion worth of Bitcoin to about 127,000 creditors. These creditors have been waiting for more than 10 years to recover their funds after the exchange collapsed in 2014 due to multiple unnoticed hacks.

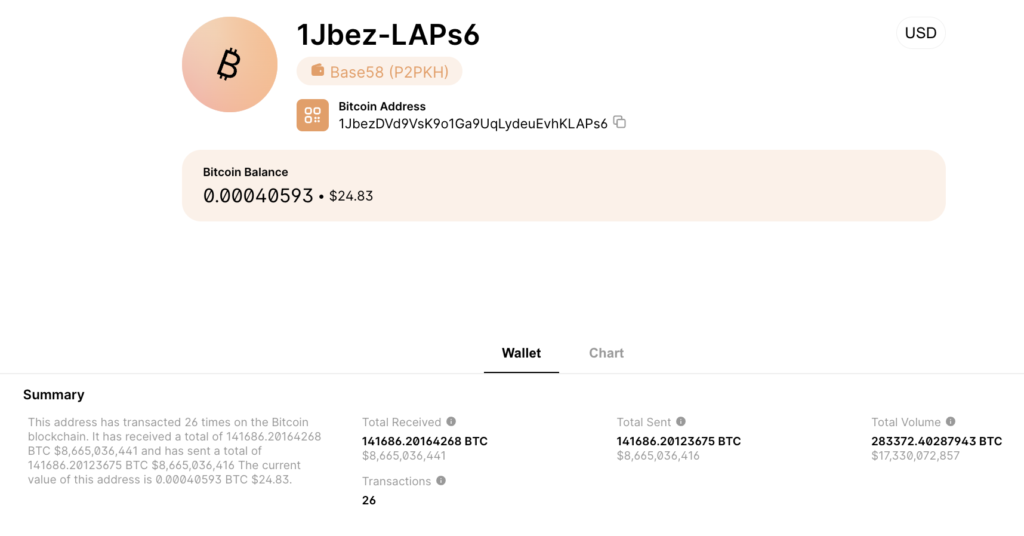

Mt. Gox wallet made transactions in May 2024

The $9.6 billion Bitcoin transfer by Mt. Gox in May was a part of the ongoing repayment process.

The exchange’s repayment plans have been among the most closely watched developments in the industry, with users waiting for over 10 years to be reimbursed for their lost BTC.

On May 28, Mt. Gox transferred 141,686 BTC, into a new wallet (1JbezDVd9VsK9o1Ga9UqLydeuEvhKLAPs6) from several other cold wallets associated with the exchange.

This marked the first on-chain movement of funds from Mt. Gox in more than five years.

After the deposits, the wallet then made several other transactions, depositing funds in other wallets.

As of the writing of this article, the said wallet holds no more funds.

Following these reports, Mt. Gox rehabilitation trustee Nobuaki Kobayashi confirmed that this consolidation was part of the exchange’s repayment plans, though he did not specify when repayments would commence.

In a May 28 announcement, Kobayashi stated, “The Rehabilitation Trustee is preparing to make repayment for the portion of cryptocurrency rehabilitation claims to which cryptocurrency is allocated… As the Rehabilitation Trustee is proceeding with the preparation for the above repayments, please wait for a while until the repayments are made.”

Markets anticipate Mt. Gox repayment

After the initial batch of Mt. Gox transfers, the price of Bitcoin dropped by 2% on May 28. As of June 25, BTC has dropped by 9.75% since May 28, when the Mt. Gox wallet was active.

This dip might indicate that markets are factoring in a potential repayment by Mt. Gox. Analysts think that the market has reacted to these movements with a slight bearish sentiment. This could be due to the expectation of selling pressure from creditors once they receive their repayments.

Despite the minor price decline, this is still an important moment in the timeline of cryptocurrency evolution, fixing one of the crypto industry’s most significant and long-standing issues.

Shareholders allege that Musk’s new venture, xAI, diverted crucial AI talent and resources from Tesla, accusing him of disloyalty and creating significant AI value outside the company.

On June 13, Tesla shareholders filed a lawsuit against CEO Elon Musk and the company’s board, alleging that Musk’s new startup, xAI, is competing with Tesla by taking its AI talent and resources. This lawsuit coincided with shareholders voting to reinstate Musk’s $44.9-billion pay package, which a Delaware judge had invalidated in January.

The Cleveland Bakers and Teamsters Pension Fund, along with Daniel Hazen and Michael Giampietro, filed the complaint on June 13 in Delaware’s Chancery Court, representing Tesla. They accuse Musk of diverting critical talent and resources from Tesla to xAI, and of raising billions for the startup while promoting its access to Tesla’s AI-related data.

Tesla has been promoting its AI-driven self-driving and driver assistance features for a long time. According to the lawsuit, xAI has recruited several key AI employees from Tesla, including Ethan Knight, the former leader of Tesla’s computer vision team, in March 2024.

Referring to a report from CNBC in early June, the lawsuit also claims that Musk started personally directing Nvidia to send graphics processing units (GPUs), which are crucial for AI models, to xAI and X instead of Tesla.

At the time, Musk stated on X that the GPUs “would have just sat in a warehouse” because Tesla had “no place to send them.”

“Throughout this period, Musk’s fellow directors on the Tesla board have done nothing,” the shareholders claimed. They accused the board of completely failing to fulfill its fiduciary duty to Tesla and its shareholders in light of Musk’s blatant disloyalty, allowing him to “create billions in AI-related value at a company other than Tesla.”

The lawsuit seeks the return of the “value that has been diverted from Tesla.”

Tesla Inc. (TSLA) shares have fallen over 28% this year.

Musk’s personal AI ambitions

In 2023, Elon Musk, the visionary behind Tesla, SpaceX, and Neuralink, launched Grok, an AI chatbot developed by his research firm xAI. Grok, named after a term from “The Hitchhiker’s Guide to the Galaxy,” is designed to be witty, informative, and engaging.

Grok was conceived to create an AI companion capable of meaningful conversations, insightful information, and a touch of personality. Led by former Google AI researcher Igor Musatov, the xAI team in Austin, Texas, specializes in deep learning and natural language processing (NLP).

Grok stands out from competitors like Google’s Bard and OpenAI’s ChatGPT with its engaging personality and real-time information access from X (formerly Twitter).

This allows Grok to provide immediate, relevant responses. Grok has performed well on key AI benchmarks, scoring 63.2% and 73% in human evaluation and MMLU, respectively, outperforming GPT-3.5.

Based on transformer architecture, Grok processes long text sequences to generate coherent responses. Currently in beta, Grok is accessible to X Premium users and continues to evolve with plans for algorithm refinement, capability expansion, and cross-platform integration.

Grok’s development reflects Musk’s commitment to advancing AI technology, aiming to shape the future of human-AI interaction in the conversational AI market.

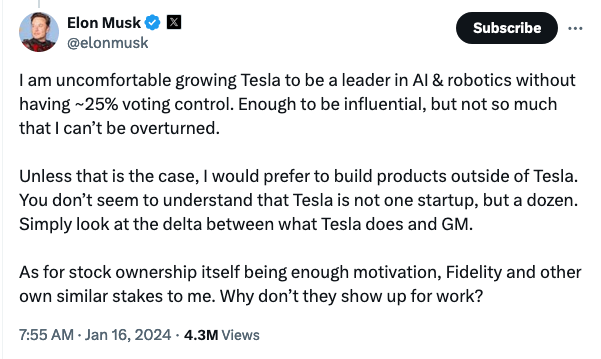

xAI started over Musk’s lacking Tesla voting control, say investors

Investors claim xAI was founded due to Musk’s lack of voting control at Tesla.

They referenced Musk’s January X post, in which he expressed discomfort with expanding Tesla’s AI and robotics efforts without having about 25% voting control. “Unless that is the case, I would prefer to build products outside of Tesla,” Musk stated.

Shareholders argue that this comment indicates Musk “deliberately founded xAI to develop AI-related products outside of Tesla that he originally planned to create within the company.”

At the time of the post, Musk owned about 21% of Tesla, but Delaware’s Chancery Court annulled his 2018 compensation plan in January, reducing his ownership to 13%, according to the lawsuit. With his voting power diminished, “Musk responded by ramping up operations at xAI,” the shareholders claimed.

The June 13 shareholder vote to reinstate the 2018 pay package is expected to face a lengthy battle in Delaware’s Chancery and Supreme Courts as Tesla seeks to overturn the previous decision.

Tesla did not immediately respond to a request for comment.

Republican presidential candidate Donald Trump positioned himself as a strong supporter of cryptocurrency and criticized Democrats’ efforts to regulate the sector during a fundraising event in San Francisco.

Former U.S. President Donald Trump is ramping up his support for cryptocurrency as part of his 2024 presidential campaign, aiming to be known as the “crypto president,” according to a recent Reuters report.

On June 7, sources said that Trump announced his ambitions during a fundraising event in San Francisco hosted by Craft Ventures’ general partner, David Sacks, and tech billionaire Chamath Palihapitiya. The event helped Trump raise $12 million to boost his campaign before the November 5 presidential election.

Trump emphasized his support for crypto and his plans to advance the industry, contrasting it with the Democratic Party’s approach, which he described as imposing strict regulations on the industry.

The claim follows Biden’s controversial decision on crypto

Just a week ago, President Joe Biden faced criticism from the crypto community after vetoing a resolution that would have overturned the U.S. Securities and Exchange Commission (SEC) Staff Accounting Bulletin (SAB) No. 121.

These guidelines require institutions that hold crypto assets to record them as liabilities on their balance sheets.

This comes after several recent statements from Trump showing his support for the crypto industry. On May 26, Trump posted on TruthSocial that the U.S. must be a leader in the crypto field.

“Our country must be the leader in the field, there is no second place,” Trump declared in a May 25 post on Truth Social, a social media platform owned by Trump Media and Technology Group. “I am very positive and open-minded to cryptocurrency companies, and all things related to this new and burgeoning industry,” he added.

He also compared himself to the current U.S. president, saying, “Crooked Joe Biden, on the other hand, the worst president in the history of our country, wants it to die a slow and painful death. That will never happen with me!”

However, some experts believe a shift in crypto regulation is happening in Washington.

Meanwhile, the crypto industry isn’t just waiting for changes.

Coinbase, a major crypto exchange, donated $25 million to the crypto-focused super political action committee (PAC) Fairshake as it increases its lobbying efforts ahead of the November U.S. elections.

This latest donation brings the total amount raised by the PAC and its affiliates this election cycle to $160 million, matching recent contributions from Ripple and venture firm Andreessen Horowitz.

Governments worldwide are pro crypto

As Trump pushes for the U.S. to lead in the crypto industry, similar efforts are being seen worldwide, highlighting the global shift towards digital currencies and blockchain technology.

For example, Qatar has recently launched the first phase of its Central Bank Digital Currency (CBDC) project.

The Qatar Central Bank (QCB) is using advanced technologies like distributed ledger and artificial intelligence to enhance liquidity and transaction efficiency for large payments among major banks. This initiative mirrors Trump’s vision of positioning the U.S. at the forefront of financial technology innovation.

Meanwhile, in Spain, Worldcoin’s human identity and financial network have suspended its operations. This follows an investigation by the Spanish Agency for Data Protection, which has halted data collection until the end of 2024.

Similar regulatory scrutiny is occurring in Germany. These challenges highlight the importance of addressing regulatory concerns, something Trump will need to navigate to ensure the responsible growth of the U.S. crypto industry.

In the United Arab Emirates, the central bank has approved a new licensing system for stablecoins. This move aims to boost digital transactions, enhance the digital economy, and foster innovation with payment tokens backed by UAE dirhams.

This regulatory clarity is something Trump envisions for the U.S., advocating for a framework that supports innovation and growth in the digital economy.

By examining these international developments, it’s clear that the global landscape of cryptocurrency is rapidly evolving. Trump’s ambition to make the U.S. a leader in this field aligns with these broader trends, emphasizing the need for clear regulations and innovative approaches to digital currencies.

The ongoing legal struggles between the SEC, Coinbase, and Ripple, have exposed the complexities of regulatory challenges in the cryptocurrency industry. On one side we see SEC’s enforcement actions, but one the other we have the financial platforms such as Coinbase that pushes for clearer regulations.

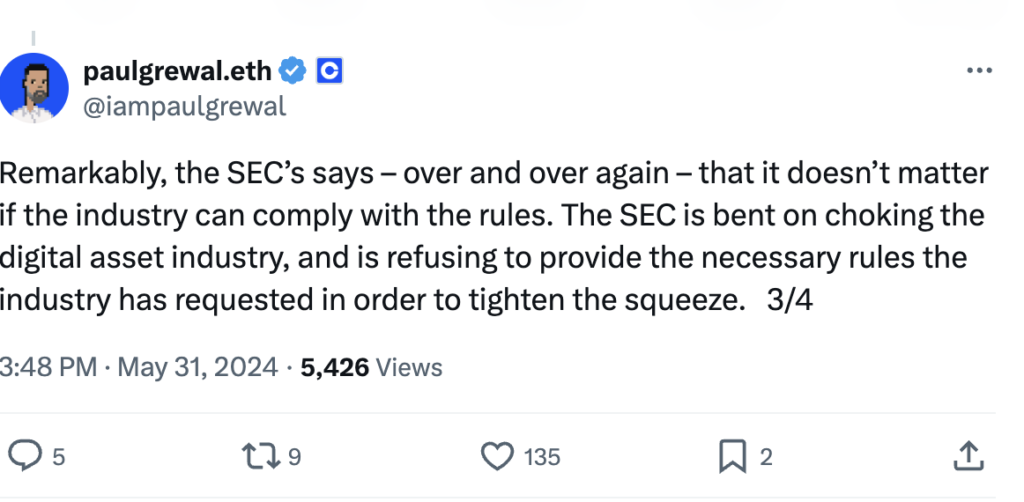

The United States Securities and Exchange Commission (SEC) will persist with its regulation-by-enforcement strategy towards the cryptocurrency industry to fulfill its objective of “choking” the sector, according to crypto exchange Coinbase.

In a May 31 filing with the U.S. Court of Appeals, Coinbase stated, “The SEC is serious about the destruction of digital assets.” This filing is part of Coinbase’s ongoing effort to compel the SEC to develop fair regulations for the crypto industry.

The exchange contends that the SEC is unwilling to establish clear and fair guidelines. “Giving the agency further opportunity to explain itself is both pointless and exquisitely undeserved,” Coinbase added.

Coinbase has argued that the SEC feels no obligation to make its rules easy to follow and thinks its regulations are “workable enough” because it has already taken legal action against several firms for breaking them. Coinbase urged the court to consider the views of other SEC Commissioners who also believe that the SEC is obstructing the digital assets industry and stifling new technology.

Hester Pierce, a pro-crypto SEC commissioner, recently suggested a cross-border sandbox program for U.S. and U.K. blockchain firms experimenting with tokenized securities. She noted that many firms seeking guidance from the SEC have found the process unhelpful, stating, “One of the problems that we’ve had is that people have tried to come into the SEC to get relief, but, you know, you sort of come in, and nothing happens. This would […] force the SEC’s hand a little bit.”

SEC downplays impact of its regulations on crypto industry

Coinbase pointed out that the SEC has tried to downplay its strict approach to the crypto industry by saying its rules only affect a small part of the market.

According to Coinbase, the SEC claims that only a “small set of market participants” might face “compliance difficulties” under certain parts of the existing rules.

The SEC sued Coinbase in June 2023, accusing the company of not registering as a broker, national securities exchange, or clearing agency, thereby avoiding the securities market’s disclosure requirements.

Coinbase has tried to get the case dismissed, but the SEC has consistently opposed these attempts.

Despite some optimism from the crypto industry and legal experts that Coinbase would succeed, it has not been able to get the case dismissed.

The SEC and Coinbase have since debated the issue online

The SEC vs. Coinbase: overview of the conflict

The conflict between Coinbase and the SEC began in June 2023, when the SEC sued Coinbase for allegedly operating without proper registrations. This lawsuit followed years of Coinbase lobbying for clearer regulations, during which they held over 30 meetings with the SEC. Coinbase criticized the SEC for its “power grab” enforcement and lack of clear guidelines.

Legal proceedings and decisions

March 11, 2023: Coinbase’s legal team accused the SEC of failing to set up clear cryptocurrency regulations.

Judge’s ruling: Judge Katherine Polk Failla allowed the SEC’s lawsuit against Coinbase to proceed but dismissed one claim related to Coinbase Wallet, narrowing the lawsuit’s scope.

October 2023: Coinbase aimed to dismiss the SEC’s charges, arguing that the transactions in question did not meet the definition of investment contracts.

January 2024: Judge Failla questioned both parties about whether certain cryptocurrencies should be classified as securities.

SEC vs Coinbase: Arguments

Paul Grewal (Coinbase CLO): Criticized SEC Chair Gary Gensler for misrepresenting crypto tokens and hindering the digital assets industry. Grewal also highlighted the need for Congressional involvement in crypto regulation.

Gary Gensler (SEC Chair): Emphasized the need for compliance with securities laws, citing scams and fraud within the cryptocurrency market. Gensler maintained that current laws are sufficient for regulating crypto securities markets.

Coinbase Chief Legal Officer Paul Grewal recently criticized SEC Chair Gary Gensler, accusing him of “misrepresenting” crypto tokens. Gensler had previously asserted, “Many of those tokens are securities under the law of the land, as interpreted by the US Supreme Court. We follow that law.”

On Monday, May 6, Gensler emphasized the impact of scams and fraud within the cryptocurrency market.

He noted that although crypto is a small part of the overall financial market, it disproportionately contributes to illegal activities due to non-compliance with securities laws.

Gensler stated that the crypto industry needs to make proper disclosures, especially for tokens classified as securities, so that investors can make informed decisions.

Meanwhile, Paul Grewal criticized the SEC for issuing a Wells notice to Robinhood Markets concerning its cryptocurrency operations. This dispute arises amid reports that the SEC is investigating whether Ethereum (ETH) is a security.

Broader industry impact

Ripple’s involvement: Ripple’s legal team, along with Coinbase’s, raised concerns with Treasury Secretary Janet Yellen about the lack of clear oversight in cryptocurrency.

Community and legal support: The crypto community, digital asset associations, and policymakers have shown support for Coinbase, highlighting the need for new legislation from Congress.

The battle between Ripple and SEC continues

On May 20, 2024, the SEC filed its response to Ripple‘s Motion to Seal, requesting the court deny Ripple’s request to seal financial and securities sales information. The SEC argued that these documents are ‘judicial documents’ and essential to the arguments in the remedies-related motions.

This push for transparency contrasts with the SEC’s efforts to keep internal documents related to William Hinman’s 2018 speech, where he stated that Bitcoin (BTC) and Ethereum (ETH) were not securities, from becoming public.

Hinman’s connection to Simpson Thacher, a firm promoting Enterprise Ethereum, has been controversial. Documents revealed he continued meeting with Simpson Thacher despite SEC Ethics Division warnings. Hinman returned to Simpson Thacher after his SEC tenure.

An ongoing investigation into alleged crypto conflicts of interest within the SEC could disrupt the SEC’s plans to appeal against the Programmatic Sales of XRP ruling. In February, watchdog group Empower Oversight announced that the Office of Inspector General was nearing the conclusion of its investigation into these conflicts, particularly focusing on Hinman’s financial ties to Simpson Thacher.

If the investigation uncovers evidence of conflicts of interest, the SEC could face significant scrutiny from lawmakers and may abandon its appeal plans to avoid further controversy. This scenario could positively impact XRP’s market perception.

Additionally, in January, the SEC filed a Motion to Dismiss its charges against Debt Box after a court order questioned the SEC’s conduct. However, Judge Robert Shelby denied the Motion to Dismiss in March.

The end of the SEC’s plans to appeal the Programmatic Sales ruling could be beneficial for XRP, potentially boosting investor confidence and market stability.

SEC vs Coinbase: Important developments

In December 2023, the SEC rejected Coinbase’s petition for new rules for digitally traded securities. Coinbase appealed this decision, seeking a court order to compel the SEC to establish clearer regulations.

As a response, Coinbase launched the #Crypto435 campaign, encouraging Americans to advocate for supportive crypto legislation, and filed a petition in federal court to demand clearer regulatory guidelines from the SEC.

Is Coinbase legal?

The ongoing legal battles and regulatory challenges faced by Coinbase highlight the urgent need for clear and fair guidelines for the cryptocurrency industry.

As the largest crypto exchange in the U.S., Coinbase’s fight against the SEC is pivotal in shaping the future regulatory landscape for digital assets.

The resolution of this conflict will significantly impact the broader crypto industry and its regulation.

Bitcoin realized price by cohort. Source: Glassnode

Bitcoin realized price by cohort. Source: Glassnode

Bitcoin capital flow by STHs. Source:

Bitcoin capital flow by STHs. Source:  Total Bitcoin spot ETF net inflow. Source:

Total Bitcoin spot ETF net inflow. Source: