A representative of Russia’s Chamber of Commerce and Industry called for the government to carry out cross-border settlements using CBDCs (central bank digital currency) and cryptocurrency.

According to TASS, a local Russian publication, Sergei Katyrin, President of the Chamber of Commerce and Industry, wrote a letter to Mikhail Mishustin, the Russian Prime Minister, containing a series of proposals for developing cooperation between African countries.

Russia to create a new bank to support economic trade with African countries

Katyrin advocated the use CBDCs (central bank digital currency) and cryptocurrency for mutual settlement and payment as part of Russia’s intent to develop more economic relationships with African countries, as a way to circumvent the Western sanctions imposed as a consequence of the Russian invasion of Ukraine.

Sergei Katyrin stated, “It seems useful to instruct the Ministry of Finance of the Russian Federation, together with the Central Bank, to ensure providing intergovernmental agreements with African states on the use of national currencies and cryptocurrencies in mutual settlements and payments.”

He also mentioned that the government should create a new export-import bank to support small and medium-sized enterprises in Africa.

At the same time, some African countries consider cooperation with Russia-linked blockchain networks.

Africa is starting to adopt crypto on a larger scale

At the beginning of April, three African countries, Cameroon, the Democratic Republic of the Congo (DRC), and the Republic of the Congo made a joint announcement about their plans to adopt TONcoin, the native coin of Ton blockchain. The announcement stated that each country would make a gradual transition to adopt cryptocurrency as a central pillar in their economic structures.

The TON blockchain is supported by the TON Foundation and has raised funds of around $250 from big companies from the crypto industry. Huobi Incubator and KuCoin Ventures were among the fund’s contributors. As projects are accepted, the fund will deploy funds via incubation, investment grants, hackathons, and educational programs.

Benjamin Rameau, the managing partner of TONcoin Fund, states that they are focusing on Web 3-related developments and are currently incubating a non-fungible token (NFT) and a decentralized exchange. He added that wallets, NFT marketplaces, and decentralized finance are all possibilities for the fund.

Unofficially, TON has been associated with Telegram, the privacy-focused messaging app, as its co-founder, Pavel Durov expresses support for TON and possible integrations on the Telegram app.

According to reports, the DRC may also launch a new national stablecoin on top of TON blockchain.

Other African countries have also reported CBDC projects, including Kenya, Ghana, and the Republic of South Africa. Ghana worked last year to build offline capabilities to support its potential CBDC. This was to encourage its use in all sectors of society.

Crypto status in Russia

Russia continues to work on issuing a new federal bill regarding the use of cryptocurrencies after they banned crypto payments in 2021. But only one year later, in mid-February 2021, the Bank of Russia launched the digital ruble trial. Russian citizens successfully transacted the digital ruble and the trial was a success.

The digital ruble trial included 12 financial institutions and three of them have already successfully implemented the CBDC platform. During the first stage of the process, users will open digital wallets on the platform’s mobile application. They can also convert the fiat in their bank accounts into CBDC and use tokens for national transactions.

The next stage of the trial is to test the digital rubles as a payment method in stores. More developments are planned for the CBDC that will enable users to use it as they use fiat currencies.

Cryptocurrency donations are elevating philanthropy and come from different types of demographics. When it comes to digital currency and charity, there are many differences that arise from traditional donations.

This method of giving is likely to be a long-lasting one in the nonprofit sector, and possibly transform philanthropy. Although the availability of cryptocurrency for charitable giving has already prompted new waves of young people to consider philanthropy, it may not be enough. While smaller charities have been able to compete for donations due to crypto’s accessibility, these are only the first steps. This is another hint that digital assets may soon become more deeply embedded in our daily lives.

Crypto donations are gaining popularity

As of the moment of writing, 2021 was the year of the largest crypto donations.

Fidelity Charitable is a nonprofit that advises donors about charitable giving. In 2020, approximately 45% of crypto investors gave to charities, while only about 33% of all general investors donated. In 2021, Fidelity Charitable has received $331 million in cryptocurrency donations, compared to $28 million in 2020. The Giving Block, a cryptocurrency donation platform reported that $69 million was the total amount of donations received in 2021. This is a huge 1,558% increase compared to 2020.

When making crypto donations, transfers can be easily performed from any country around the globe, which allows charities to have donors worldwide. Many international charities have begun accepting cryptocurrency donations:

Crypto donations can help when NGOs are unable to obtain funding through other mediums. A famous example is WikiLeaks, which is banned from receiving funding through Visa, Mastercard, and PayPal. WikiLeaks now receives millions in crypto donations. Despite the unprecedented growth, cryptocurrency charity is still a new way of giving that differs from the traditional charity methods.

One of the main difference between traditional donations and crypto donations are the donors. On average, cryptocurrency users are younger than traditional donors to philanthropy. More than 60% of cryptocurrency users are younger than 40. The average age for crypto users in the United States is 38, while the average age for donors is 64.

United Way, an international charity, began accepting cryptocurrency in 2014. According to their analytics, the average user is between 45 and 65 years old and 80% of users are female. At the same time, the average age of donators of United Way is between 25 and 35 years, and 80% are men. This is a clear sign that the rise of cryptocurrency is attracting younger people to philanthropy.

What are the causes of this demographic shift? The answer is more complex and consists of:

Causes published on social media

Crypto transactions have low fees

Tax deductions

Crypto donations are anonymous

Social and humanitarian causes published on social media

Many cryptocurrency donations are made by tech-savvy young adults who want to support causes that receive more attention online. These donors might read touching stories and feel connected to specific events. Stories shared via Twitter about the Russia-Ukraine conflict have resulted in around $100 million in crypto donations for Ukraine.

Similar to the first wave of the pandemic in India, social media was a COVID-19 helpline that had global reach and helped with crypto donations. Vitalik Buterin (Ethereum founder) donated $1 billion to India’s COVID-19 relief program in Shiba Inu tokens. These tokens soared in price around the same period. He also donated about $5 million in ETH for Ukraine.

The Tor Project, a well-known non-profit dedicated to internet freedom and privacy, received 58% in cryptocurrency donations in 2021. This was due to crypto donors’ greater affinity for data privacy causes than other causes.

Because crypto donors might be confused about which cause or non-profit they should support, The Giving Bock recently introduced cause funds and impact index funds. These funds will assist donors in making informed decisions and could open up opportunities for them that they may not have otherwise considered.

The crypto donation platform allows you to fund causes that cover education, disaster relief, food, and the environment. Donors have the option to support a specific cause, rather than picking a non-profit organization. All non-profits receive an equal amount of the donation amount. This arrangement gives smaller non-profits an equal footing and ensures that the larger cause receives greater attention than bigger, more well-known non-profits.

Crypto transactions have lower transaction costs

For many reasons, donors may find crypto donations more attractive. Donations can be used to avoid capital gains taxes for crypto investors. There are also potential savings for donors as well as non-profits from transaction fees that traditional financial platforms require.

Crypto donations have lower transaction costs than credit and debit cards. Since most traditional donations happen online via a credit card, the processing fees vary between 2% to 7%. This fee is much lower for crypto donations.

A $2,000 wire transfer from the U.S. may add between $30 to $50 in transaction fees. Transferring the same amount via the Ethereum blockchain can cost around $15-20 in gas fees. But there are many other blockchains that charge much lower fees. The transaction time in crypto is also considerably less, while international bank transfers can take up to a few days.

Tax deduction for crypto donations

Another reason for making crypto donations is to reduce taxes. Tax-deductible crypto donations to NGOs are possible in the U.S., Canada, Australia, as well as New Zealand.

An investor can deduct the current fair market value of the crypto when he or she donates it directly. If the value of the crypto assets has appreciated over time, you can now deduct the value of the current price from your taxes, although you may have invested far less. If, however, you want to convert crypto to fiat first, you may have to pay capital gains taxes. These taxes can be as high as 20-30%.

Crypto helps to protect anonymity

It is easier for nonprofits to identify existing donors than it is to find new donors. Donors often prefer anonymity as they feel the pressure to give more. Donating large amounts may also require you to complete a KYC (know your customer) process.

Crypto donations help donors maintain their anonymity while they give millions of dollars. However, this anonymity offered by crypto may not last as many countries raise crypto regulations.

More than 1,300 charities accepted cryptocurrency donations in 2021. By allowing direct crypto donations, more young people are inspired to give. This shift will encourage smaller organizations to adopt crypto donations as well, and potentially disrupt the model of traditional donations.

In an age of blockchain and crypto, the physical war in Ukraine could be funded by NFTs. Ukraine’s Minister of Digital Transformation announced an NFT collection to illustrate the chronological events of the conflict between Russia and Ukraine.

The government of Ukraine is selling non-fungible tokens (NFTs) to ensure that all the facts and events of the war between Russia and Ukraine will not be forgotten over time. All the funds collected will be used to support the army and civilians in the atrocious war.

Ukraine’s invasion

On February 24th, 2022, Russia started to invade Ukraine. The entire world was in shock, including Russian citizens. Nobody ever believed that the threats of the Russian president, Vladimir Putin, would ever come to ve true. We were all wrong.

Ukraine’s invasion has been going on for more than a month now, and the end of the aggression is nowhere in sight.

While the officials of the two sides continue to meet for face-to-face talks in the pursuit to end the war, the population is either defending the country or fleeing.

Since the first week of the invasion, the Kyiv government has started to accept cryptocurrency donations, which were plentiful, especially from famous personalities within the tech and crypto space.

The crypto donations also proved to be a reliable financial market during these uncertain times. The Bitcoin price went up as sanctions poured in and the Russian economy started to collapse.

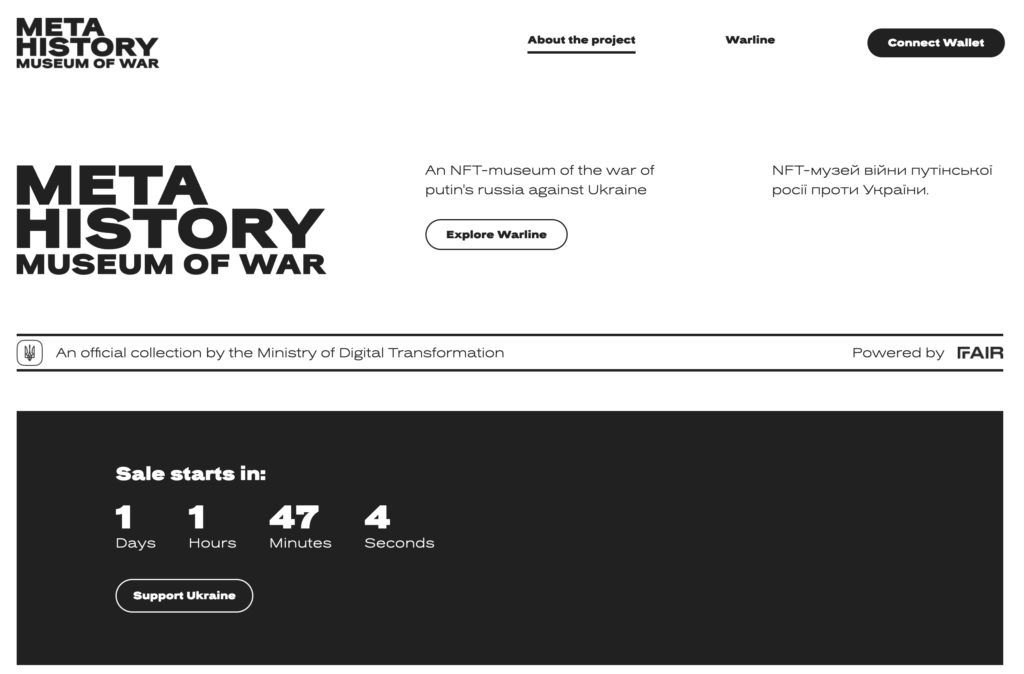

Meta History: Museum of War

The NFT collection displaying the terrible facts of the war between the two countries has been announced with a Twitter post by Mykhailo Fedorov, Ukraine’s Minister of Digital Transformation.

While Russia uses tanks to destroy Ukraine, we rely on revolutionary blockchain tech. @Meta_History_UA NFT-Museum is launched. The place to keep the memory of war. And the place to celebrate the Ukrainian identity and freedom. Check here: https://t.co/IrNV0w54tg

Ukraine’s minister claimed that while Russia uses tanks to destroy Ukraine’s infrastructure, Ukraine relies on revolutionary blockchain tech to help rebuild it.

The Museum of War is a collection that combines non-fungible tokens (NFTs) registered on blockchain with news items. Each item of the collection is a reminder of an important event of the war and uses a unique illustration.

The NFT launch replaces an earlier plan that would have allowed tokens to be airdropped to anyone who donated cryptocurrency to Ukraine. However, the government decided to not do the airdrop. There is currently no plan to give prior donors an advantage in selling the new NFTs.

Both countries have used cryptocurrency to bypass local currency restrictions and capitalise on the hype around cryptocurrency to solicit donations. Some claim that the Ukrainian government raised $54 million in cryptocurrency through donations.

Writing history into the collective memory of the digital age

According to the online museum, these tokens aim to preserve the memories of those events. They are created with the sole scope to share truthful information with the entire world and help continue receiving donations for Ukraine’s support.

The virtual museum platform presents the collection as a chronological record of all events in recent Ukrainian history. The NFTs are factual statements accompanied by personal reflections. Each NFT has a simple formula: each token is an actual news piece from an official source and an illustration from international artists.

At the moment, there are 54 NFTs available, which cover the first three days of the war between Russia and Ukraine. The NFT collection of the war in Ukraine starts with Russia’s announcement to launch a special military operation in Donbas.

The collection is currently unreleased but can be seen on the project’s official website. The sale is expected to start at the beginning of April 2022.

The NFT collection is being launched in collaboration with Fair.xyz, a blockchain company that provides the NFT sales platform.

Supporters can also choose to donate Ether (ETH) directly on the page of the project – Museum of War.

Web3 is one of the most used words of 2022. The idea behind the buzzword is to create a decentralised platform that hosts decentralised applications. As the concept gets more supporters, investors are paying attention.

What is Web 3.0?

Web3, or Web 3.0, is a cryptographic term that describes a decentralised internet version that runs on public blockchains such as the Ethereum blockchain, or any other programmable platform.

Web3 could reduce the power of the largest internet companies, such as Amazon, Google and Microsoft, and give that power back to users. However, the technology needed for this massive internet shift may not be here yet, and it is not as advanced as the hype and the popularity of digital assets. Therefore, Web3 does not pose a threat to tech giants. Yet!

Some voices argue that Web3 won’t be a truly decentralised Internet. This is especially true as venture capitalists continue to invest in space in order to monetise and control it. Jack Dorsey, the former CEO of Twitter, stated that Web3 on Ethereum will be centralised because of heavy venture capital investment. His repeated comments have led to a dispute between Dorsey and venture capitalists, who have invested billions in the crypto space and Web3 this past year.

You don’t own “web3.”

The VCs and their LPs do. It will never escape their incentives. It’s ultimately a centralized entity with a different label.

As with everything trending, big investors have taken notice of the upcoming Web3, and many have already decided to invest in it. Does this mean that Dorsey’s prophecies are right?

Nexo Ventures will be investing in Web3, decentralised finance (DeFi), non-fungible tokens (NFTs), metaverse, and GameFi. The venture arm will be led by Tatiana Metodieva, Nexo’s head for corporate finance and investments. Nexo Ventures would “explore the feasibility” of allowing Nexo’s users to invest alongside them and thus leverage our capabilities to facilitate wealth maximisation and investor diversification.

Since the appeal of a Web3 ecosystem has sparked the attention of investors, several similar funds have been launched in recent months. In December 2021, Hashed has raised $200 million for a fund dedicated to growing the Web3 ecosystem. Hashed is s South Korean venture firm that started investing in the crypto space in 2016, hitting big on projects like Axie Infinity and The Sandbox.

Griffin Gaming Partners, a gaming-focused venture capital firm, also announced that it would be investing $750 million in Web3.

Gaming has been a hot industry sector, with crypto exchange FTX investing $100 million last year to help fund gaming studios that incorporate the Solana blockchain into their games. Lightspeed Venture Partners and Solana Ventures raised the fund.

Wait, is the metaverse part of Web 3?

Web 3.0 is about who will control the internet in the future, but the metaverse is about how people will interact with the internet in the future.

Most people navigate websites and apps using their smartphones, tablets, or computers. The metaverse will use virtual reality (VR) to access the Internet, and users will be able to move between virtual worlds using digital avatars.

Animoca Brands is a Hong Kong-based game software and has a broad portfolio of blockchain games, traditional games, and other products.

Animoca Brands’ co-founder and chairman, Yat Siu, stated that his company would continue to assist businesses into Web3 in order to accelerate the evolution to an open metaverse.

Siu is long a supporter of the concept that an open metaverse would be better than one that is controlled by large Web2 companies. Siu’s argument centres on the fact that Web3 platforms and tech like NFTs allow users to retain ownership rights over data and content online instead of being controlled and used by large centralised Web2 companies such as Meta.

Siu believed that we are “super early” in terms of building an open metaverse. However, he stressed the importance of speeding the process because of the danger of large centralised firms dominating the virtual sphere.

Yat Siu believes that Web3 is a great way to combat the central metaverse companies. As Web3 develops into a global trade framework, users will be accustomed to having a stake in it.

In the end, this is what Web3 is trying to solve – user ownership and privacy. The web2 era has been all about big corporations owning customers’ data. But that’s about to change.

On March 14, the European Parliament discussed the effects and carbon footprint of Proof-of-Work cryptocurrencies. The EU Bitcoin ban was not passed, but the energy discussion has not ended.

A rule proposal that would have effectively banned Bitcoin in the European Union (EU) has been struck down.

The European Parliament’s Committee on Economic and Monetary Affairs (ECON) voted to keep the provision out of a draft Markets In Crypto Assets (MiCA) framework. This is the EU’s comprehensive regulatory package that governs digital assets.

EU’s response to crypto companies: MiCA

The MiCA framework was introduced by the European Commission in September 2020, as the EU executive branch responsible for proposing and enforcing laws. It is part of a larger digital finance strategy to adapt Europe to the digital age. It’s also quite different from other regulatory efforts.

For instance, the U.S. has introduced many bills over the years that directly impact the crypto space. These include tax and securities laws, but different states may have their own regulatory requirements. The country does not have a comprehensive equivalent to the EU’s MiCA. In August, the country’s most comprehensive bill regarding crypto regulation was presented. China had already banned crypto trading and mining in 2021. However, it was still working on its own digital currency, the digital yuan.

MiCA covers cryptocurrencies such as Bitcoin and Ether, as well as stablecoins. The proposed framework does not cover digital currencies issued by central banks (CBDCs), nor crypto assets like security tokens, which might be considered financial instruments such as securities, deposits or treasury bills.

Although the promise of a passportable license to crypto asset service providers sounds appealing for established crypto firms that want to establish in the region, industry participants are concerned about the impact MiCA may have on the EU’s digital asset market.

EU’s Parliament voted on the crypto proposal

This Bitcoin ban proposal was added to the draft last Wednesday. It sought to limit cryptocurrencies powered using an energy-intensive computing process called proof-of-work (PoW). The proposal was met with heavy opposition by crypto advocates around the world.

After the Bitcoin ban was opposed by the committee, Stefan Berger, member of the EU Parliament, and rapporteur for MiCA, tweeted: “ECON committee approved my #MiCA report. A good day for the crypto sector! The EU Parliament has paved the way for innovation-friendly crypto regulation that can set standards worldwide. The process is not over yet; Steps still lie ahead of us.”

ECON-Ausschuss hat meinen #MiCA-Bericht angenommen. Ein guter Tag für den Krypto-Sektor! Das EU-Parlament hat den Weg geebnet für eine innovationsfreundliche Krypto-Regulierung, die weltweit Maßstäbe setzen kann. Der Prozess ist noch nicht vorbei; Schritte liegen noch vor uns /1

The vote on the provision, commonly known as the Bitcoin ban, was close, and a small majority could defeat it. The proposal required that all cryptocurrencies be subject to the EU’s “minimum environmental sustainability standard with respect to their consensus mechanism.”

The rule suggested a phase-out plan for popular proof-of-work (PoW) cryptocurrencies such as Bitcoin and Ether that would allow them to switch their consensus mechanism to less energy-intensive methods like proof-of-stake (PoS).

While plans are in place to make Ethereum a proof-of-stake (PoS) consensus system this year, it is not clear if the same will be possible for Bitcoin.

The MiCA draft will be subject to a “trilogue” after the vote of the Parliament. This is a formal round between the European Parliament, Commission and Council.

Can renewable energy sources save Bitcoin?

Experts in renewable energy see two possible ways that crypto can be used to address power consumption concerns, first, by increasing demand for renewable energy sources. Second, by using blockchain technology to interact transparently and transparently with power grids in an auditable and measurable manner.

A small majority of members of the monetary committee voted for a compromise calling on the European Commission to propose alternative regulations. This is the EU’s executive arm that proposes new legislation.

“By January 1 2025, the Commission shall present to the European Parliament and to the Council, as appropriate, a legislative proposal to amend Regulation (EU) 2020/852, in accordance with Article 10 of that Regulation, with a view to including in the EU sustainable finance taxonomy any crypto-asset mining activities that contribute substantially to climate change mitigation and adaptation.”

Some politicians and regulators around the globe have criticized proof-of-work for their concerns about energy. EU leaders are worried that renewable energy could be used to sustain cryptocurrencies such as bitcoin, instead of being used for national purposes.

U.S. President Joe Biden instructed federal agencies to coordinate efforts in drafting cryptocurrency regulations through an executive order.

According to a fact sheet accompanying the order, this governmental effort to regulate the crypto industry focuses on consumer protection, financial stability, illicit uses, leadership in the global financial sector, financial inclusion and responsible innovation.

This executive order, which is the first to be solely focused on the growing digital assets sector, directs federal agencies in communicating their work better but does not specify the positions that the administration would like agencies to take.

The order also did not set out any new regulations that cryptocurrency companies must follow.

Senior administration officials spoke neutrally about digital assets, telling reporters that the growing cryptocurrency sector could threaten the U.S. financial system and national security. Criminals could use cryptocurrency to hide funds or avoid sanctions if there is not enough oversight.

The official stated that digital assets could also offer American innovation, competitiveness, and financial inclusion opportunities. “Innovation is key to America’s story, our economy, creating jobs and new opportunities, building new industries and maintaining our global competitive edge.”

The U.S. executive order that focuses on digital assets, has six key points:

protecting U.S. interests

protecting global financial stability

preventing illicit uses

promoting “responsible innovation,”

financial inclusion

U.S. leadership

Around 40 million Americans have reported to be trading or investing in cryptocurrency, which is 16% of the entire U.S. population.

An administration official cited crypto’s volatility as one reason that investors could be hurt. He pointed out that the price of bitcoin at the start of the COVID-19 epidemic was $10,300. The price reached a peak of $69,000 in November 2021, before plummeting again at the beginning of 2022.

The official stated that the President had proposed a whole-of-government holistic approach to understand not only macroeconomic risks but also the microeconomic risk to each individual, investor, and business that interacts with these assets.

The official stated that investor protection will be a key goal. Understanding the technology that underpins digital assets is one part of this effort. Part of this effort will also include understanding the weaknesses and areas that are not serving all consumers in the current financial system.

The official stated that the order recognises that the assessment of potential risks and benefits of digital assets must also include an understanding of how the financial system meets current consumer needs in an equitable, inclusive, and efficient manner.

The “antiquated” payment infrastructure could make it difficult for consumers to access services. This was especially true for cross-border payments, the official stated.

The future of money

A section of the order directs U.S. Treasury Department officials to prepare a report about “the future money and payment system.”

The effects of cryptocurrencies on economic and financial growth will be observed to the extent that technological innovation may influence that future.

Last November’s President’s Working Group report called for Congress to pass a bill that more clearly defines federal bank regulators’ oversight power over stablecoins. Moreover, the Financial Stability Oversight Council could act in place of legislation.

Yellen mentioned FSOC’s role, saying that the financial stability watchdog would examine any potential risks posed in the cryptocurrency sector and “assess whether appropriate safeguards” are already in place.

Digital dollar

In the executive order, the U.S. will ask agencies to assess how they could issue a CBDC (central bank digital currency).

This order is tied to the Federal Reserve’s ongoing efforts to study digital currency issuance. In recent months, branches of the central bank published numerous reports evaluating both technological and policy questions before a central bank digital money (CBDC).

According to the administration official, CBDCs are being considered by more than 100 countries. These use cases can include both domestic and international transactions.

The official stated that many of these countries were also working together to establish standards for CBDC design, and cross-border systems.

The price of Bitcoin (BTC) surpassed the $40,000 level on intraday charts, as the leading cryptocurrency rose more than 15% in one day, despite the ongoing war between Russia and Ukraine.

The two largest cities in Ukraine, Kyiv and Kharkiv, are under attack from the Russian side. However, the huge economic sanctions imposed on Russia seemed to have brought the largest single-day gain Bitcoin had seen in a year. Most of the crypto markets are green, and Ethereum (ETH), the second-largest cryptocurrency, has risen by more than 12%.

All banks worldwide have pledged to block SWIFT from Russia. The U.S. Treasury Department has placed a ban on U.S. entities interfacing with Russia’s central banks. Foreigners are prohibited from Moscow’s stock exchange for fear of stock-market sell-offs.

Financial markets and war in Ukraine

Russian President, Vladimir Putin, initiated the conflict in Ukraine. The entire world is watching, and most nations are sending humanitarian aid and military equipment. However, observers fear that the almost 200,000 strong invading force that was defeated by the surprisingly strong Ukraine resistance will resort to more brutal tactics. As sanctions from the United States and Europe began to bite into Russia’s economy, the Russian and Ukrainian delegations held an initial peace talk at the Belarus border during the fifth day of the conflict.

Although nobody had expected Ukraine to fight off the invading forces for so long, with each day that passes, more economic sanctions and escalations are taking place.

Mykhailo Fedorov, Ukraine’s Vice Prime Minister and Minister for Digital Transformation asked that all major crypto exchanges block Russian addresses during the fifth day of the conflict.

The U.S. and the European Union have removed certain Russian banks from the Society for Worldwide Interbank Financial Telecommunications (SWIFT), a messaging network that supports global financial transactions. This is the system that both Ripple and Stellar are trying to replace with lighting speed networks and significantly lower transaction fees.

Is cryptocurrency a way to avoid sanctions?

These economic sanctions are without precedent in the modern economy, and some militate for adopting blockchain products to bypass some of these constraints. As investors see the potential for massive investments in decentralised finance (DeFi) after the Russian sanctions, Bitcoin and all other top altcoins are rallying today.

Due to the ban from the SWIFT payment system, Russian banks are now prohibited from interbank transactions with non-Russian entities. It is expected that the Russian banks will try to use crypto as a way of circumventing this sanction and other measures meant to isolate them from the global financial system.

Russian citizens are now unable to use their credit cards outside Russia, and the effects of the harsh sanctions on the Russian central bank had caused the ruble to drop 30% in one day, on February 28, when $1 was around 101 Russian Rubles. In an attempt to stop the price from plummeting even further, the Russian central bank froze the Russian exchange market and ordered Russian businesses to sell 70% of their foreign cash assets. Also, the central bank ordered brokers not to execute sell orders from foreign shareholders.

The DeFi space is still an innovation, but considering the strict Russian financial environment, it could help increase the number of people focusing on it. Military conflicts have always posed a huge threat to economies, and investors often wonder where else they can put their money. This looks like one of those smart bets, and DeFi could be one of the few solutions left to this fast degrading economy.

Without a doubt, the sanctions imposed on Russia by Western powers are biting hard on the country’s economic system. Russia’s ruble is sinking.

Major cryptocurrencies have declined on Monday, February 21, as Russia publicly recognised two pro-Russian republics in Eastern Ukraine.

There are no concrete plans for a summit between Putin and U.S. President Joe Biden. However, 150,000 Russian troops are reported to have moved closer to the Ukraine border.

Investors have become more cautious in recent weeks as they fear rising energy prices, sanctions from the U.S. and its European allies against Russia. This will likely impact a global economy already suffering from inflation and delays in supply chains.

Russia deployed troops in Ukraine

After recognising the two regions as independent on February 21st, Russian President Vladimir Putin directed the deployment of troops in the two eastern Ukraine breakaway areas. This accelerated a crisis that the West fears could lead to a major war.

These moves were condemned by the United States of America and the European Union. They promised new sanctions. However, it was unclear whether the West would view the Russian military action as a start of an invasion. In practice, the area was already controlled both by Russian-backed separatists as well as Moscow.

It is expected to see the U.S. announce new sanctions soon as a response to Russia’s decisions.

Political tensions cause crypto prices to decrease

Although the price of Bitcoin has been steady throughout the week, some analysts predict a volatile few more weeks.

After a strong February during which we saw the cryptocurrency rebound from six-month lows at 2022’s beginning, BTC settled in the $41,000 to 45,000 range.

However, things changed as the Biden administration announced sanctions against the separatist Ukraine republics following Putin’s speech. The price per barrel of brent crude oil rose to $97, which represents an almost 4% increase.

Bitcoin, the most popular cryptocurrency, dropped to around $36,000 in the following hours. This is a drop of over 5.5% from the previous 24 hours. Ether, which is the second-largest crypto by market capitalization, lost 7% during the same time period. Other cryptos suffered from negative numbers.

The U.S. equity market was closed due to the National Presidents Day holiday. However, major European stock exchanges including the FTSE 100 and the DAX in Frankfurt, as well as the CAC 40 in Paris, finished in the red. Major Asian indexes lost ground Monday as well, including the Japanese Nikkei225, Hong Kong’s Hang Seng, and the Asia Dow.

Market analysts noticed that the sudden deterioration of diplomatic relationships can have a strong effect on financial markets. The cryptocurrency market was already sensible and the investor’s confidence, which was already shallow, has quickly disappeared.

Some of the biggest losers are Theta Fuel (TFUEL), Gala (GALA), Harmony (ONE), Quant (QNT) and New (NEO), as they all lost over 16% in value in the last 24 hours.

Other cryptocurrencies that are popular, Cardano and Solana, have fallen by around 12% in the past day. Memecoins such as Dogecoin and Shiba Inu have seen their value drop by 7-10% during this period.

Overall, the crypto market has fallen by 6% in the past day and is now valued at $1.67 trillion.

The chart is mostly in red and shows no signs of recovery.

Stocks extend losses as investors weigh likelihood of Russia invading Ukraine

Most financial markets experience downturns by the prospect of war between Russia, Ukraine and other countries. The increasing political tensions have shaken both the crypto and other commodities market. As investors waited for developments in Russia-Ukraine, worldwide shares keep losing value.

Shares fell in all Asian markets. Tokyo’s Nikkei225 index fell 1.8% to 26,426, while Hong Kong’s Hang Seng lost 3.29%, to 23,575. The Kospi in Seoul fell 1.69% to 2,695.80. The Shanghai Composite index also fell 1.44%, to 3,440.

S&P 500 e-mini futures slid 1.81%. Dow Jones industrial average futures e-mini fell 1.37%, while Nasdaq 100 futures e-mini dropped 2.65%. The stock market was closed in the US due to the President’s Day holiday.

On February 8, 2022, the U.S. Justice Department announced that it had seized over $3.6 billion worth of stolen Bitcoin. They arrested a couple who were accused of laundering the cryptocurrency stolen in the Bitfinex heist six years ago.

Ilya Lichtenstein (34) and Heather Morgan (31) were charged with conspiring to launder the 119,754 Bitcoin stolen in 2016 from Bitfinex, one of the largest cryptocurrency exchanges in the world.

The capture of the lost funds, at the beginning of February 2022, make it the largest financial seizure of all time – considering the price of one Bitcoin at around $40,000.

An official from the Justice Department declined to comment on whether Mr Lichtenstein or Ms Morgan were involved in the 2016 Bitfinex theft.

What happened during the 2016 Bitfinex hack?

Over the years, many crypto thefts highlighted the security flaws in the cryptocurrency’s relatively new world. Even though most of the funds were eventually recovered, they still led to the loss of large amounts of digital currency. Another important aspect of these hacks is the news itself, which causes crypto to lose significant value.

The 2016 Bitfinex breach was one of many cryptocurrency exchange hackings and it resulted in the theft of 119,754 Bitcoins.

After Bitfinex, one of the largest crypto exchanges in the world was hacked, the price of Bitcoin’s plunged around 20%.

The US court documents prove that Bitfinex’s hackers sent 2,000 transactions, adding up to 119,754 BTC, to a cryptocurrency wallet that belonged to Ilya Lichtenstein. The documents also show that around 25,000 BTC was transferred from that wallet over the past five years. The funds underwent a series of complicated transactions in an attempt to conceal their true origin.

However, thanks to the underlying blockchain technology, the funds were traced. Part of those funds ended up in accounts owned by the two defendants, while some were spent on gold, NFTs and gift store certificates.

On January 31, 2022, the law enforcement officers gained access to Lichtenstein’s wallet, including his encrypted files stored in a cloud account. This led investigators to confiscate 94,636 Bitcoins that were still in that wallet, which are now worth around $3.6 billion. In 2016, when the hacking took place, the 119,754 BTC stolen were worth approximately $71 million. As of 2022, the amount would be worth over $4.5 billion.

The couple was released on bond

On February 8, 2022, Mr Lichtenstein and Ms Morgan appeared in Manhattan’s federal court. The judge released them on bond at $5 million for Mr Lichtenstein’s case and $3 million for Ms Morgan’s case. There was no response on their part.

Ilya Lichtenstein has American and Russian citizenship and describes himself as a tech entrepreneur. According to her LinkedIn profile, Heather Morgan is a serial entrepreneur. According to the complaint, the couple is accused of conspiring to defraud the United States.

After the arrest, the deputy attorney general stated that this outcome only comes to prove that cryptocurrency does not provide a safe haven to criminals. Despite the defendants’ efforts to launder the stolen funds, digital anonymity couldn’t be preserved. The police managed to follow the stolen Bitcoin each time it was moved to a new wallet.

Cryptocurrency is not for the criminals

As more Americans are buying and selling cryptocurrency like Bitcoin, regulators have placed some large American exchanges under their official supervision.

However, cryptocurrencies are moved through decentralized computer networks, which aren’t under the control of any government or central entity. As such, most trading occurs on unregulated exchanges, like Bitfinex. These exchanges give little information to consumers about their operations.

These security issues that keep threatening the world of cryptocurrency exchanges, can only weaken consumer confidence and slow down widespread adoption. Mt. Gox, the first Bitcoin exchange, got shut down after it was hacked in 2014 and $500 million were stolen.

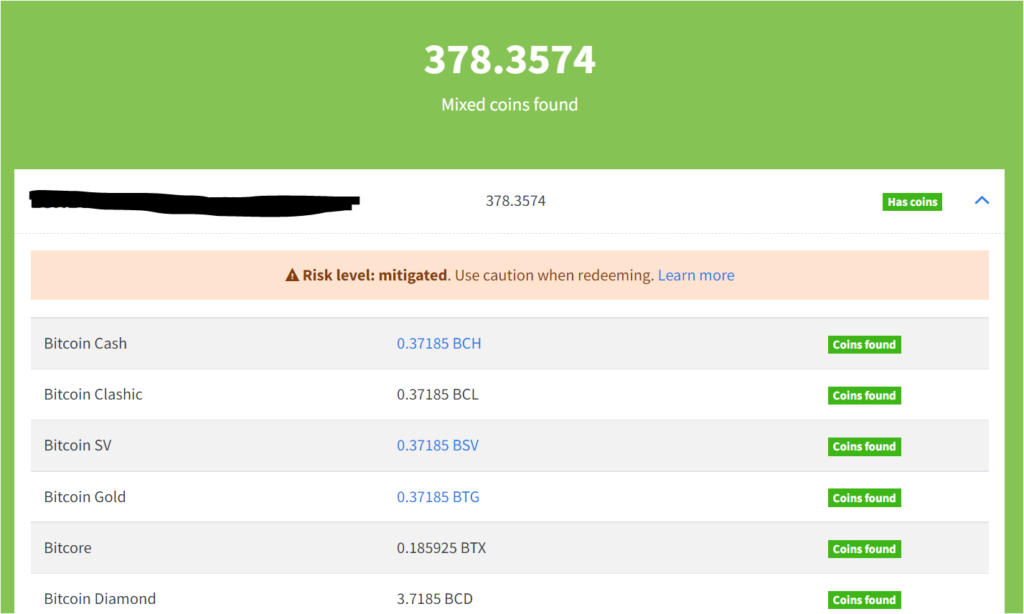

Did you know that you can claim Bitcoin hard forks coin if you owned Bitcoin at the moment of the fork?

Bitcoin, the first and most popular cryptocurrency ever created, has not been free from conflicts within the community. Over the years, many individuals and groups of developers have come up with ideas to make Bitcoin even better.

But most of these suggestions ended up dividing the community. That’s why over 100 Bitcoin hard forks have taken place since Bitcoin’s creation in 2009. Here’re the top BTC hard forks and how to claim them.

A Short History of Bitcoin

On October 31, 2008, a whitepaper was published that described the concept of Bitcoin ━ a trustless peer-to-peer system for digital currency to replace traditional money. The paper was published under the name of Satoshi Nakamoto, but the author’s identity remains a mystery to this day. Many believe that the name is a pseudonym of one or a team of developers.

On January 3, 2009, the genesis block (block 0) was mined on the Bitcoin network, and the miner, the unknown Satoshi, was rewarded with 50 bitcoins.

From that point on, Bitcoin (BTC) was mined by other early contributors up to 2010. Laszlo Hanyecz, a programmer, made the first commercial transaction using cryptocurrency by purchasing two Papa John’s Pizzas for 10,000 BTC.

Bitcoin has been traded many millions of times since then. The first major transactions were made in black markets. The largest was the Silk Road, an online black marketplace, which traded close to 10 million Bitcoin during its lifetime.

As Bitcoin grew more as a currency on different markets, regulations emerged from many countries. For instance, the People’s Bank of China (PBC) made the news headlines when they adopted these three separate actions and issued new regulations regarding cryptocurrencies.

December 2013. The PBC banned financial institutions from using Bitcoin.

September 2017. The PBC issued a total ban on Bitcoin use.

June 2021. PBC implemented a crackdown against major cryptocurrency miners.

The price of Bitcoin fell by half after each of these events. However, it always found a way to rise again to new astonishing values. This is because many countries and institutions allow cryptocurrency use. Also, as of September 7, 2021, El Salvador became the first country in the world to adopt Bitcoin as legal tender.

Another aspect of what makes Bitcoin increase in price is the maximum supply. There can only be 21 million BTC. As more investors join the cryptocurrency market, the coin experiences scarcity and the Bitcoin (BTC) price surges as with any supply and demand market.

Additionally, Bitcoin is more transferable and divisible than gold or another material asset and can be stored more easily. It will cost you a lot to transport gold, as well as the cost of storage in secure facilities. However, investors can store Bitcoin on a USB stick, also known as a cold wallet or hardware wallet.

As Bitcoin gained more popularity, it inspired other developers to create other blockchain platforms, and subsequently, some created Bitcoin hard forks.

What is a Bitcoin fork?

Many of the cryptocurrencies that exist today use part of Satoshi’s technology. However, many others adapted the Bitcoin blockchain model or tried to improve it.

As more users joined the blockchain, it became increasingly difficult to update the network as no single person or group could decide on unanimous future development.

To modify the Bitcoin blockchain, all miners must agree on the new rules and what constitutes a valid block on the chain. To change the rules, you must “fork” it to change to indicate that something has changed from the original protocol. These situations are called Bitcoin forking.

Usually, forks are used to add new features or change some blockchain parameters. The forking process results in the blockchain being divided into two distinct blockchains after a certain point in time. Although there have been many forks since the inception of Bitcoin, only a few are viable projects.

Crypto forks can be either soft or hard forks. The main difference is that soft forks are not a fork that results in a new currency and new branches of the blockchain. Soft forks slightly modify the Bitcoin protocol, but the core Bitcoin blockchain remains the same. Soft forks are backwards compatible, which means that the upgraded chain can successfully share and use data from earlier network versions.

However, during a hard fork, the programming code of the Bitcoin blockchain and its mining processes are upgraded. Once a user has updated their software, it rejects transactions from any older version, creating a new branch to the blockchain. Users who keep the older software can still process transactions. This means that transactions are being processed on two separate chains, and two different currencies result from the hard fork.

This is how various digital currencies, similar names to Bitcoin, have been created. These include Bitcoin Cash and Bitcoin Gold.

While not many investors know, anyone who owns Bitcoin, during a hard fork, is entitled to the new cryptocurrency. That’s why some consider that there’s an obvious financial incentive to fork Bitcoin’s blockchain and made some investors sceptical of the necessity of these forks.

Since it can be confusing for casual investors to distinguish between these cryptocurrencies, we’ll be going through the top Bitcoin hard forks.

Bitcoin Forks History

Bitcoin has over 100 forks, but not all projects were further developed, and only a few remain functional today. You can find the complete list of Bitcoin forks on forkdrop.io. We’ll mention the most noteworthy Bitcoin forks here.

Bitcoin XT

Bitcoin XT fork took place on December 27, 2014.

Bitcoin XT is the first known Bitcoin hard fork. Mike Hearn incorporated some of his ideas into the Bitcoin blockchain and launched Bitcoin XT in late 2014. It is said that Hearn is one of the few to have contacted Satoshi Nakamoto via email.

Bitcoin XT was designed to allow 24 transactions per second. The previous version of Bitcoin could only handle seven transactions per second. It proposed to increase the block size from 1 megabyte to 8 megabytes.

Initially, Bitcoin XT was a success. In 2015, it had more than 1,000 nodes running the software. But, just a few short months later, investors lost interest, and the project was abandoned. Bitcoin XT has been removed from the internet, and its website is not functional anymore.

Jonathan Toomim launched Bitcoin Classic in early 2016 as some community members wanted to see block sizes increase after Bitcoin XT’s decline.

Bitcoin Classic, like Bitcoin XT, saw a lot of initial interest. In 2016, there were approximately 2,000 nodes in use. The Bitcoin Classic (BXC) fork proposed a smaller block size of 2 MB.

The BXC coin still exists, but it seems that the community has moved on. The website is no longer live.

Bitcoin Unlimited

Bitcoin Unlimited (BU) fork took place on March 11, 2016.

Bitcoin Unlimited has remained a mystery since its initial release in 2016.

Bitcoin Unlimited is unique because it allows miners to choose the size of their blocks. Nodes and miners can limit the number of blocks they accept up to 16 megabytes. The community behind Bitcoin Unlimited believes in market-driven decision making, emergent consensus, and giving their users choices.

Despite some initial interest, Bitcoin Unlimited has not been widely accepted. Only a few nodes are still online.

Bitcoin Cash fork took place on August 1st 2017 (BTC block 478,558).

Pieter Wuille, a Bitcoin Core developer, presented the idea for Segregated Witness (SegWit) in late 2015. SegWit is a project that aims to decrease the size of Bitcoin transactions, thus allowing for more transactions to occur simultaneously. Technically, SegWit is a soft fork.

In response to SegWit, some Bitcoin developers and users decided to initiate a hard fork to avoid the protocol updates it brought about. Bitcoin Cash was the result of this hard fork. It split off from the main blockchain in August 2017, when Bitcoin Cash wallets rejected Bitcoin transactions and blocks.

Bitcoin Cash allows blocks of eight megabytes and does not accept the SegWit protocol.

Bitcoin Cash remains the most successful Bitcoin hard fork, and it is backed by many in the cryptocurrency community. BCH can be traded on popular exchanges (Binance, Coinbase, Huobi, Gate.io).

BitCore (BTX)

BitCore (BTX) fork took place on April 24, 2017.

BitCore is an unspent transaction output (UTXO) fork of Bitcoin, and it was launched in 2017. BitCore used Bitcoin’s source code to create a new blockchain but updated the core to make the blockchain size smaller (which makes the network easier to scale). BitCore uses the MEGABTX consensus algorithm, which is ASIC-resistant.

Because anyone can become a BitCore miner, it is impossible to centralise mining power. BitCore also has a 10 MB Segwit-enabled block that allows it to handle 17.6 billion transactions per annum or 48 million transactions per hour.

The entire crypto community can mine BTX using PoW and Masternodes.

Bitcoin Gold fork took place on October 23rd 2017 (BTC block 491,407).

Bitcoin Gold is a hard fork that occurred shortly after Bitcoin Cash. The creators implemented this hard fork to restore mining functionality using basic graphics processing unit (GPU) because they felt mining had become too specialised.

The Bitcoin Gold hard fork featured a pre-mining of the Bitcoin Gold crypto. Pre-mining is when the development team creates the coin from the start. In this case, the Bitcoin Gold developers pre-mined 100,000 BTG. Developers said that these pre-mined coins will be used to grow the Bitcoin Gold ecosystem and pay developers.

Bitcoin Diamond (BCD) fork took place on November 24, 2017 (BTC block 495.966).

Bitcoin Diamond is a fork of the original Bitcoin blockchain. Bitcoin Diamond was created only two weeks after the Bitcoin Gold fork.

The BCD’s code allows for 100 transactions per second, increasing the block size to 8 megabytes, thus making it more efficient than Bitcoin. While this is an improvement, considering Bitcoin’s seven transactions per second, other cryptocurrencies have much greater transaction throughput, and that’s why some consider Bitcoin Diamond obsolete.

However, the first major Bitcoin hard fork, Bitcoin Cash, can process 116 transactions per second through its increased block size. Although these cryptocurrencies may not be the same, Bitcoin Cash and Bitcoin Diamond are very similar. Some investors wonder if Bitcoin Diamond was a necessary hard fork.

Bitcoin SV hard fork took place on November 15th 2018 (BCH block 556,766). It is a fork from the Bitcoin Cash blockchain.

Bitcoin SV‘s goal is to realise the original vision and design of Bitcoin as described in Satoshi Nakamoto’s whitepaper.

BSV is designed to provide stability and scalability while keeping Bitcoin a peer-to-peer electronic money system. It also aims to become a distributed data network that can support enterprise-level advanced blockchain applications.

It has also removed artificial block sizes limits, re-enabled script commands, and other technical capabilities that had been previously disabled or restricted by protocol developers on the BTC blockchain. The network can process thousands of transactions per second while keeping transaction fees low for micropayments. It also offers advanced capabilities like tokens, smart contracts and other use cases.

The block size of Bitcoin SV can go up to 2Gb and can process over 10,000 transactions per second. BSV reached over 50.000 TPS on the testnet.

BSV is unmatched in its ability to scale on-chain without any restrictions while being closer to the original Bitcoin design than any other blockchain.

Bitcoin Cash ABC (eCash)

Bitcoin Cash ABC fork took place on November 15, 2020 (BCH block 661648).

Bitcoin Cash ABC (BCHA) is a cryptocurrency that was created in 2020 as a result of a hard fork within the Bitcoin Cash blockchain. This split the original chain into two new ones called “Bitcoin Cash ABC” and “Bitcoin Cash Node.”

Amaury Sechet is the leader of the Bitcoin Cash ABC developers. They proposed an update to the Bitcoin Cash network. This update included a controversial new “Coinbase Rule,” requiring 8% of all mined Bitcoin Cash to be distributed to BCH ABC to finance protocol development.

Another group, Bitcoin Cash Node from the Bitcoin Cash community, opposed the upgrade. They removed the so-called “miner tax” from their source code.

In July 2021, Bitcoin Cash ABC (BCHA) was rebranded as eCash (XEC). With this relaunch, the team also announced their plans to integrate the proof-of-stake consensus layer Avalanche, which introduces great improvements to the network.

Three main improvements are:

Scaling transaction throughput to more than 5,000,000 transactions per second

Improve the payment experience by reducing transaction finality

The eCash (XEC) rebrand also decreases the coin’s decimal from eight to only two.

Beware of Bitcoin Forks Scams

You should also bear in mind that some Bitcoin forks were created as a scam. Bitcoin Platinum, for instance, was created to lower Bitcoin’s value. Other scams, such as the fake Bitcoin Gold wallet, were created to steal your real funds. That’s why it’s crucial to keep your crypto funds safe and don’t trust everyone you talk to over the internet.

At the same time, you should be aware that some developers just want to make quick money. While some Bitcoin forks seem to be similar, the primary reason for their creation is more marketing buzz. Many developers are looking for free coins, and Bitcoin forks have become the new ICOs. The team creates the fork only to sell the coins on crypto exchanges as soon as it starts trading.

To reduce your chances of losing any Bitcoin, you have to move your Bitcoin to a new wallet before claiming any coins.

How to safely claim coins from a fork

Before attempting to claim any Bitcoin fork coins, you should research the new project and the team of developers behind it to establish its legitimacy. They should also provide a clear and accurate roadmap for the project they want to build.

For instance, a Bitcoin fork coin should implement replay protection, to allow the new network to separate from its original.

Depending on the specific Bitcoin fork, you might need to perform certain risk actions such as exposing your Bitcoin wallet private keys, installing specific software or validating your identity on centralised crypto exchanges.

One of the easiest ways to claim Bitcoin fork coins is to use wallets that support them. Note that most wallets don’t support many of the Bitcoin forks simply because the process requires complicated technical developments, which is not feasible for most wallets. This is because most of the Bitcoin forks don’t have a great market value and lack a development team and community.

Bitcoin forks can have various aspects to consider:

Coin ratio. Depending on the Bitcoin fork, the new coins (forked-coins) can be claimed at a specific ratio (It’s mostly a 1:1 ratio, but it can vary).

Fork height. The Bitcoin block height at the time that the Bitcoin Fork took place. Bitcoin wallets that received BTC after that date are not eligible for the Bitcoin fork claim.

Crypto exchange availability. Minor and less successful Bitcoin fork coins will not be supported by a lot of crypto exchanges.

Before attempting to claim any Bitcoin fork coins, you should go through these simple (but effective against theft) steps.

Step 1. Move Bitcoin to a new wallet

For all Bitcoin fork claims and any forks in general, users need to provide the wallet’s private keys in which the Bitcoin was held at the time of the Bitcoin fork. You should never share the keys of an active wallet.

That’s why, for safety reasons, moving the crypto funds to a different crypto wallet should be performed first before revealing the private keys to any third party. By doing this, you eliminate any possibility of having your Bitcoin stolen.

If you still have a Legacy Bitcoin wallet with addresses beginning with 1, claiming these forks can be a great motivation to move your coins to a SegWit account. This will lower your transaction fees and allow you to use Lightning Network.

Step 2. Export private keys

Firstly, you will need to export your private key from the wallet that was used to hold the Bitcoin funds at the time of the fork. Most wallets are able to export a file containing all the addresses and private keys. However, hardware wallets don’t allow private keys export, and for such cases, you need to enter the seed phrase into specific claiming software.

You can import only private keys that have funds to save time.

Step 3. Check Bitcoin wallet address for available claims

Using your Bitcoin wallet address, you can check if your address is entitled to a Bitcoin fork claim on Findmycoins.ninja.

You should save all the claimable wallets’ addresses and private key combinations.

All valid addresses and private key combinations should be recorded in a spreadsheet or text file that allows you to copy, paste, or replace text. The recording format should include a private key followed by the address.

Each entry should be numbered and the amount of Bitcoin they contain at the time of the first fork. It will be helpful to number each key pair for ordering purposes. It may be useful to note the sizes. You can, for example, use the address with the smaller amount to test the process.

Step 4. Claim the Bitcoin fork coin using a crypto wallet

There are several secure crypto wallets that can help you claim some of the most popular Bitcoin forks, such as:

Coinomi. Supports Bitcoin Cash (BCH), Bitcoin Gold, Bitcoin SV (BSV). Find the guide on how to claim Bitcoin forks on their support page.

BitPie & Bither wallets. These are two distinct mobile app Bitcoin wallets. BitPie is used to claim the coins, and then Bither can be used to sell them. Using the two wallets you can successfully claim Super Bitcoin (SBTC), BTW, BCD, BTF, BTP, BTN, Bitcoin Cash and Bitcoin Gold.

While the BitPie and Bither wallets are the most common solution you can find on the web these days to claim your Bitcoin forks, the wallets do not support BTC fork claiming anymore. We tried this option without any success.

How to use Coinomi for Bitcoin fork claims

Step 1. Install and create a Coinomi wallet

Firstly, make sure you have the latest version of Coinomi on your mobile device. Afterwards, create a new wallet, and make sure to write down its seed phrase to recover your funds later, in case something happens to the mobile device. You will also be asked to set up a password for this specific wallet and device.

Step 2. Select the coins you want to add

Before claiming the Bitcoin forks in the Coinomi wallet, you need to select the specific coins as balances in your Coinomi wallet.

Click on the bottom-right plus sign and select Add coins. Select the Bitcoin forks you will be adding (e.g. Bitcoin Cash (BCH), Bitcoin Gold (BTG), BitcoinSV (BSV)).

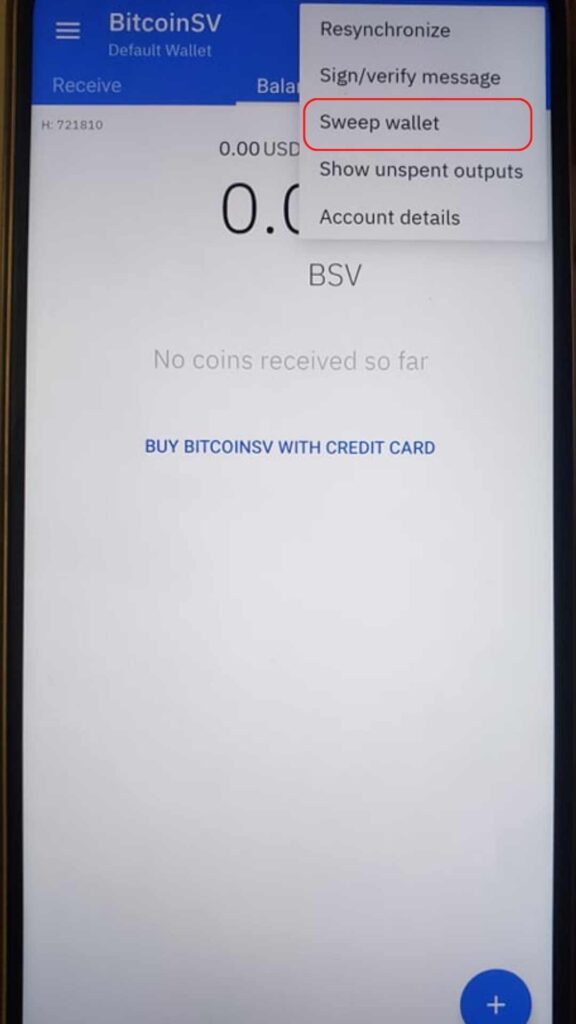

Step 3. Claim Bitcoin fork coins

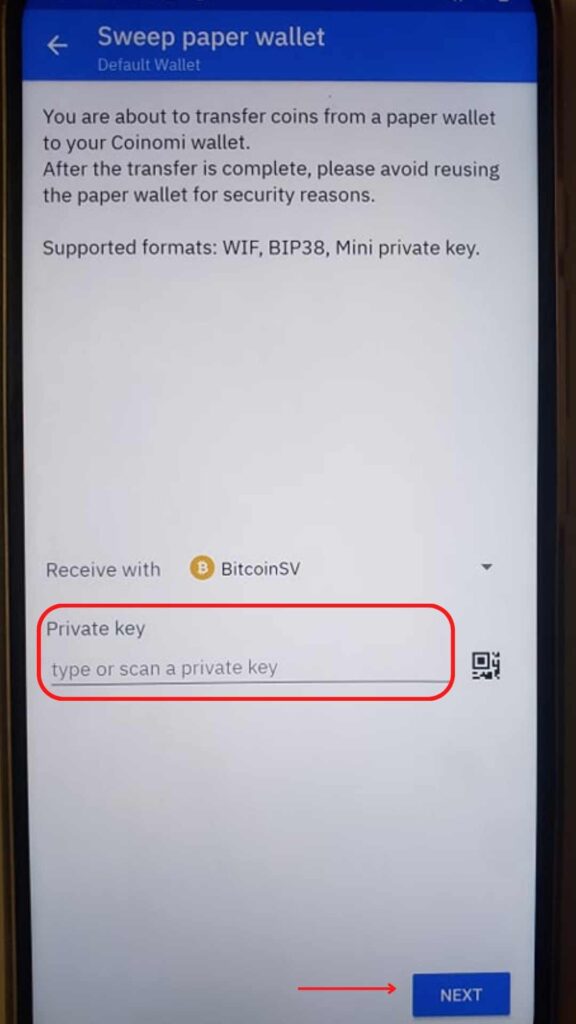

Select the coin you want to claim the Bitcoin fork for, and within that specific wallet, click on the top menu > Sweep wallet.

You will have to paste or scan the wallet’s private key that had the Bitcoin at the time of the fork.

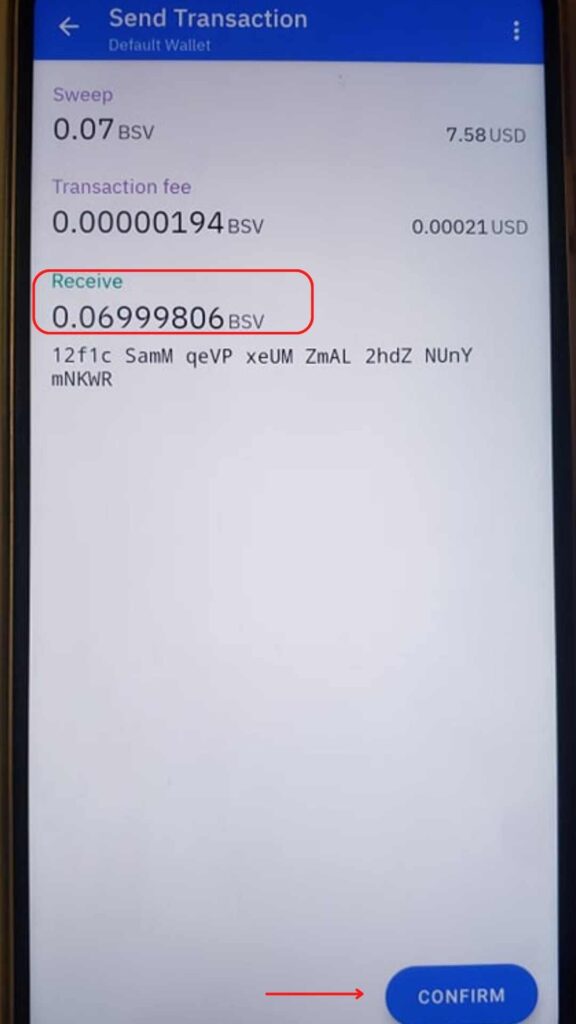

After you get all the transaction details (The amount of Bitcoin fork coins you will receive, the value in USD, the transaction fee), review all the details and tap Confirm.

You will then see the updated balance for the Bitcoin fork coins.

Repeat this step for every address with a balance of the forked coin.

How to claim Bitcoin forks using Ymgve’s Fork Claimer

More advanced crypto users that do not want to rely on a specific Bitcoin wallet, can use Ymgve’s script to claim the most Bitcoin forks. This method will require some technical knowledge on the user’s side because you will need to run a Phyton script.

The Ymgve is open-source. It is available on GitHub, along with all the information about how to use the script. Ymgve supports standard P2PKH and Segwit P2SH-P2WPKH addresses.

Using the Ymgve fork claimer script is recommended if you want to claim most forks, although it’s riskier and mistyping any of the commands can result in a loss of funds.

How do Bitcoin hard forks influence Bitcoin holders?

By the end of 2021, there have been over 100 Bitcoin hard forks, and investors expect to see more soft and hard forks in the years to come. However, out of all the hard forks to date, only a few are still operational.

Long time investors are entitled to claim all of these Bitcoin hard forks. Luckily there are ways to do so, using the wallets described in this article. However, as of the beginning of 2022, no Bitcoin fork has raised more in popularity than the original Bitcoin.