Navigating the dynamic landscape of the crypto industry, we explore the crucial role of security, education, and regulation in mitigating escalating crypto scams. How can these new-age digital assets, despite their rapid evolution and growth, can be protected from the increasing threats posed by bad actors?

The amount of money stolen by criminals in the cryptocurrency world has gone up a lot in the past two years. Even so, people who specialize in online security aren’t worried. They say that new technology often gets taken advantage of when it’s first introduced.

CertiK, the blockchain security company, published a report about online security in 2022. According to the report, wrongdoers stole more than $3.7 billion from Web3 technologies last year. This was a huge jump – 189% more than the $1.8 billion stolen in 2021.

In another report about the first three months of 2023, CertiK said that hackers got their hands on over $320 million.

You can also watch the key findings in the 2022 Certik report on their YouTube channel: https://youtu.be/lWZscaMAR0s

While this is worrying tech developers and investors, it’s also a normal phenomenon. The more projects and technologies are launched, the more there will be people who will search for ways to misuse that technology. This is because new stuff often has weaknesses and opportunities for misuse.

We’ve seen this pattern before, from the beginning of the internet to the spread of email and, most recently, with the introduction of blockchain and digital money.

At the same time, we need to remember that the crypto industry is still new. Some people in the industry are more interested in growing and creating new things than they are in making sure everything is secure. This could be why we’re seeing so many thefts.

Statista, a company that collects data, offers data that may anticipate more growth in the crypto industry. According to their report, the cryptocurrency market is projected to reach US$37.87 bn in 2023. The number of cryptocurrency users is expected to reach 994.30 million by 2027.

Why are there so many scams in crypto?

The fast growth in the number of users and earnings in the crypto industry, along with its new ideas, may lead to more misuse. In the end, we must remember that blockchain technology and smart contracts, which is the infrastructure for digital currencies, are very complicated.

This complexity can lead to weak security spots that talented hackers can misuse. Because digital currencies have real value and can be exchanged for fiat money in many parts of the world, they’re tempting for hackers who can quickly take and possibly cash in the stolen digital money.

In the future, the crypto world will become more secure, and as Web3 gets more mature, there will be fewer successful hacks, misuses, and scams.

However, there will always be a never-ending fight between the wrongdoers and the blockchain security experts, as they both work towards their goals in this constantly changing industry.

But industry leaders see it as a wake-up call for us to double our efforts to secure our funds. And for the financial authorities to oversee these game-changing technologies and make it possible for everyday users to access them safely and responsibly.

Artificial Intelligence – is it secure?

Artificial intelligence (AI) has been a hot topic recently. Some people are talking about how it might change the way we work, while others, like tech entrepreneur Elon Musk, are saying we should be careful about how it’s developed.

We will probably see AI gets used more and more, and it’ll probably face its own security problems, just like Web3 and other new types of technology.

As AI becomes a bigger part of our everyday lives, especially in areas where security is important, like self-driving cars or financial systems, the chance for hacks, misuse, and scams will likely go up.

AI systems can be taken advantage of in several ways, from messing with machine learning algorithms to data tampering and hostile attacks.

Sensitive data can also be accidentally shared from large language models as people interact and share info with AI chat platforms like ChatGPT.

However, as long as there is no immediate money-making opportunity with AI, scammers will probably not start using AI just yet.

But AI can certainly aid any researcher in doing their job, whatever that may be. For instance, AI capabilities may allow for a more advanced set of attack methods. Machine learning can be used by security researchers to check smart contracts to find weak spots more efficiently,

The pain points of the crypto industry

The cryptocurrency industry, being relatively new, is experiencing a number of pain points.

These include:

Rapid Evolution. The speed at which the industry evolves makes it challenging for security measures and best practices to keep up, leading to vulnerabilities.

User Knowledge. Users are still learning how to use crypto technologies safely, making them easy targets for exploitation.

Smart Contracts. Their open and visible nature means that if a contract has a flaw, it can be exploited by anyone, at any time.

Decentralization. Unlike traditional systems that can add extra layers of security through centralized servers, the decentralized nature of blockchain technologies can expose them to more threats.

However, the industry is continually improving its security practices, with some decentralized finance (DeFi) platforms implementing additional measures such as multi-signature wallets and time locks.

In addition, there’s an increased focus on regulatory scrutiny and user education to reduce future scams and hacks.

Crypto scams get more attention than traditional thefts

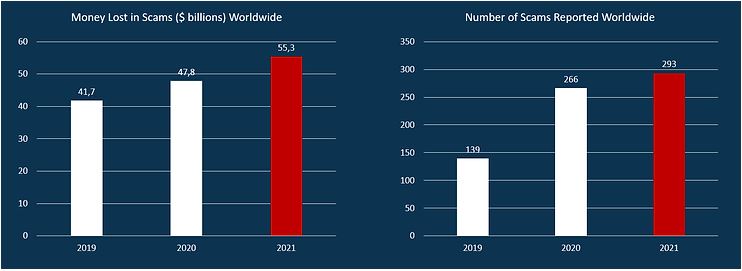

But crypto scams represent only a fraction of the total financial scams. The traditional money system continues to set records for losses through malicious actions each year.

Crypto is often highlighted in the news for theft and fraud, but the total losses are actually much less than fraud involving credit cards, automated clearing house transactions, and wire transfers worldwide.

Source: Global Anti-Scam Alliance

According to the Global Anti Scam Alliance, a nonprofit group dedicated to protecting consumers from financial crime and scams, traditional money lost to scams has been increasing, with $47.8 billion lost in 2020 and $55.3 billion in 2021.

The United Nations estimates that globally, the amount of money laundered around the world in a year is guessed to be 2 – 5% of global GDP, which is about $800 billion – $2 trillion in today’s US dollars. However, since money laundering is done in secret, it’s hard to figure out the total amount of money that’s actually laundered.

What draws so much attention to crypto scams is the very thing that attracted investors in the first place – its transparency.

Crypto transactions happen on the blockchain and are visible to everyone. This transparency can help track stolen funds and may explain why losses in crypto get more attention.

When a major theft occurs, everyone around the world can help track the funds to see exactly where they go. This isn’t possible in traditional financial systems where fund movements happen behind closed doors on private networks.

As more people around the world start using crypto, total losses will probably increase accordingly. However, better education and understanding of cryptocurrencies will ensure this increase isn’t disproportionate to other payment methods.

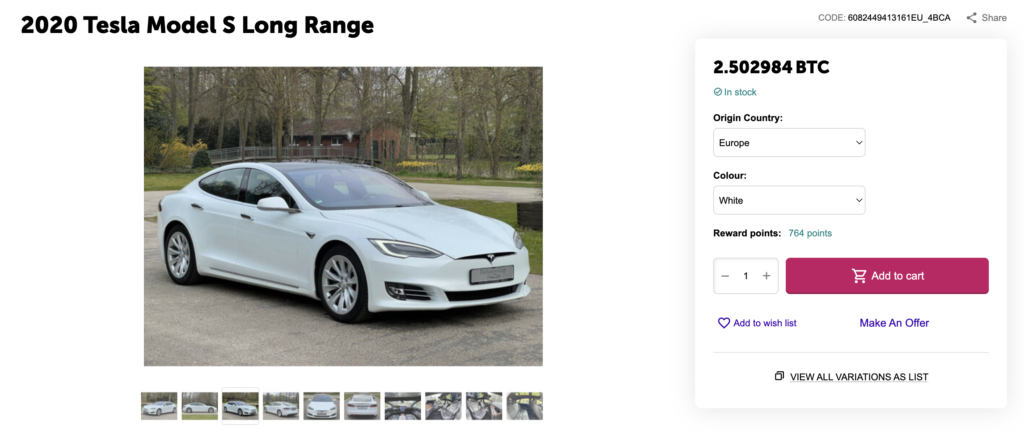

Are you planning on buying a car with Bitcoin? Cryptocurrency is now used to buy real-world assets such as cars and even real estate. While this payment method isn’t accepted worldwide, more and more services are starting to consider it. And car dealerships are no exception.

In 2021, Tesla’s CEO, Elon Musk, announced that it would accept Dogecoin as payment for Tesla. Meanwhile, the offer is no longer standing, but that doesn’t mean you can’t use Bitcoin to buy a car in 2023.

Is it legal to buy a car with Bitcoin?

Yes, it is indeed legal to purchase a car using Bitcoin. You can also use other popular cryptocurrencies, such as Dogecoin and Shiba Inu. However, similar to any other online transaction, it is important to exercise caution and adopt certain safe practices.

The first thing you need is to find a reputable car dealership that accepts Bitcoin as a payment method.

You can do this by checking out reviews on third-party consumer forums to discover the best places to purchase cars with cryptocurrencies. Platforms such as Crypto Emporium and BitCars have supported crypto payments for some years now and have excellent reputations in the market.

One of the advantages of using cryptocurrencies like Bitcoin for transactions is that they are generally secure. This means that you do not need to disclose any personal financial information, as transactions take place directly between two digital wallets. This method of payment contributes to your safety and security during the transaction.

While there is no car manufacturer that accepts cryptocurrency throughout their distribution network as a whole, there are specific car dealerships that have implemented cryptocurrency payment services to serve customers who wish to complete their purchases using digital assets.

In the end, it’s up to you to find a platform that allows crypto payments for products such as cars. Some of the most popular options for such purchases include:

One of the most popular payment services is BitPay, which is already used by some Lamborghini and BMW dealerships thought Europe, the UK and the USA.

Finding out if a car dealership accepts Bitcoin or other cryptocurrencies is simple. The quickest way is to call local dealerships and ask. Salespeople might need to check with management, but they should give you an answer soon.

You can also look at car dealership websites to see if they accept Bitcoin. However, these sites mainly focus on selling cars and might not clearly mention payment methods, so it could be a bit frustrating unless the dealership prominently displays this option.

How to buy a car with Bitcoin (or any other cryptocurrency)

Buying a car with cryptocurrency can be done from a dealer that accepts it or from a private seller who is comfortable with crypto. Usually, dealing with a dealer is easier. Here’s a simplified plan:

Find out which dealerships accept cryptocurrency.

Research different cryptocurrency exchange apps and learn how they work. The dealer might prefer a certain app like BitPay. Depending on the payment processor, you might need to set up an account.

Confirm that the dealer accepts the cryptocurrency you own. Bitcoin is one of the most commonly accepted.

Choose the car you want to buy.

Follow the dealership’s instructions for the exchange.

What’s the advantage of buying a car with Bitcoin?

There are several reasons why some crypto investors prefer to use Bitcoin to buy a car:

Fast Payments. Bitcoin transactions are usually faster than traditional fiat payments. Traditional payments rely on bank transfers or credit/debit cards, which require multiple intermediaries for processing. In contrast, Bitcoin transactions are decentralised and don’t involve intermediaries, allowing for quicker transactions that often take only a few minutes.

Highly Secure Payments. Bitcoin transactions use advanced encryption techniques, making them highly secure. They are recorded on a public ledger called the blockchain, which is virtually impossible to counterfeit or alter. Once a transaction is recorded on the blockchain, it can’t be amended or deleted. This immutability makes all transactions permanent and tamper-proof, hindering anyone from manipulating network records.

Lower Transaction Fees.Bitcoin transactions typically have lower fees than traditional payment methods such as credit cards or wire transfers. This advantage becomes especially significant for international transactions, where traditional remittance fees can be high. Crypto transactions could potentially eliminate 97% of these fees, making large, cross-border transfers more cost-effective.

No Transaction Limits. When purchasing a car with Bitcoin, you don’t need to worry about transaction limits. This is important when making big purchases like cars. Credit card companies and banks may decline a purchase exceeding a certain amount, but cryptocurrencies have no such limitations. This ensures that the transaction proceeds without any delays.

Should you buy a car with Bitcoin?

Whether or not you should buy a car using Bitcoin greatly depends on your comfort level with risk and volatility.

Cryptocurrencies, including Bitcoin, are known for their dramatic price swings.

Take, for example, Bitcoin’s performance in November 2021, when it reached a high of nearly $69,000. At that point, you could have purchased a new Porsche 718 Cayman with just one Bitcoin. Fast forward to the present, Bitcoin’s value is around $17,000, so the same Bitcoin would only be enough to buy an average city car.

The value of cars doesn’t fluctuate as significantly as cryptocurrencies, which makes this kind of transaction risky. However, a workaround for this volatility could be to use stablecoins, which are cryptocurrencies designed to maintain a stable value relative to a specific asset or a pool of assets. A good example is the USDC or USDT, which you can store in a crypto wallet and use for car payments, thus mitigating the risk of your crypto’s value suddenly dropping.

That being said, if you are a firm believer in the future of cryptocurrencies and their potential to revolutionise our financial system, buying a car with Bitcoin could be an exciting way to apply this innovative technology. Plus, there is a certain novelty factor in being able to tell your friends that you bought a car using Bitcoin.

Ultimately, the decision to buy a car with Bitcoin should be based on your personal financial situation, your tolerance for risk, and your belief in the future of cryptocurrencies.

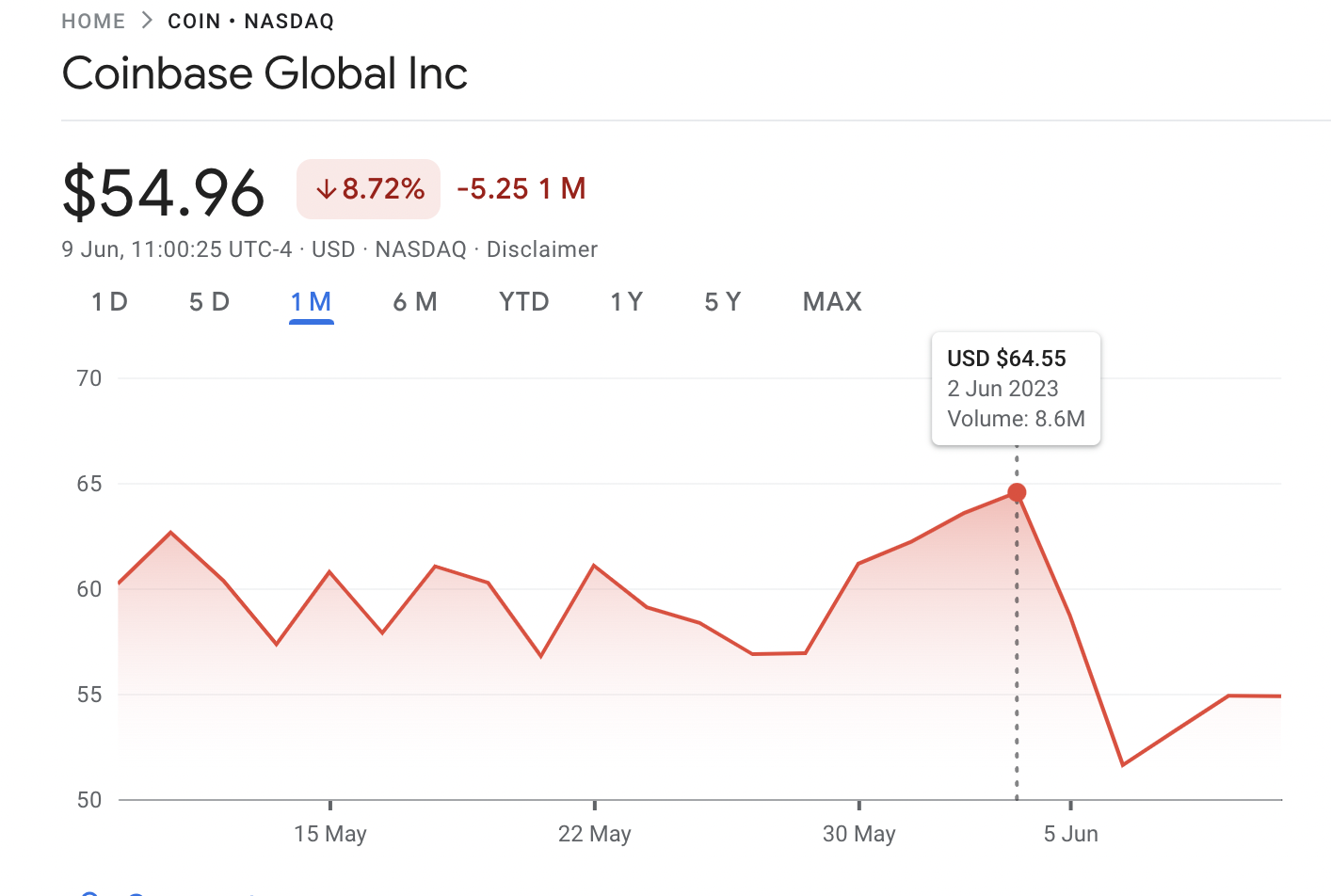

After recently suing Binance, the SEC now targets Coinbase for allegedly operating as an unregistered securities exchange, adding to regulatory scrutiny in the crypto industry.

The U.S. government’s finance watchdog, the Securities and Exchange Commission (SEC), is suing Coinbase. Coinbase is a big company in New York that trades cryptocurrencies like Bitcoin.

The SEC says that Coinbase should have registered as a broker, national securities exchange, or clearing agency, but they didn’t.

This registration helps keep trading fair and transparent.

Also, the SEC claims that Coinbase has been selling certain cryptocurrencies that it shouldn’t have. These include Solana, Cardano, Polygon, Filecoin, The Sandbox, Axie Infinity, Chiliz, Flow, Internet Computer, Near, Voyager Token, Dash, and Nexo. According to the SEC, these count as securities, and you need special permission to sell them.

Today we charged Coinbase, Inc. with operating its crypto asset trading platform as an unregistered national securities exchange, broker, and clearing agency and for failing to register the offer and sale of its crypto asset staking-as-a-service program.https://t.co/XPG2gDkxtVpic.twitter.com/hCdVMw8B2v

— U.S. Securities and Exchange Commission (@SECGov) June 6, 2023

The lawsuit also says that Coinbase has been working like a broker for securities since 2019 without the needed registration. This is two years before they first started offering public shares in April 2021.

The SEC says that Coinbase’s staking program is also a problem. This program involves five different cryptocurrencies. According to the SEC, this makes the staking program an investment deal and counts as a security. Coinbase has been arguing with the SEC about this, saying its staking products are not securities. They keep arguing even though Kraken, another crypto company, settled with the SEC and stopped offering staking services in the U.S.

Gary Gensler, the head of the SEC, spoke about the lawsuit against Coinbase. He said Coinbase had not given its customers enough protection against scams and manipulation. They’ve also not been open about conflicts of interest. Gurbir Grewal, who is in charge of enforcing SEC rules, said that Coinbase knew they were breaking federal securities laws, but they did it anyway.

After the SEC announced its lawsuit on June 6, the price of Coinbase’s shares fell by 15% before trading started.

The SEC’s lawsuit against Coinbase happened just one day after they also sued Binance. Binance is another crypto company that the SEC accuses of breaking securities laws and mixing up customers’ money. Binance is in trouble for breaking 13 different securities laws.

The U.S. Securities and Exchange Commission (SEC) has charged Binance, the world’s largest crypto exchange, and its founder, Changpeng Zhao. They’re accused of mixing up billions in user funds and sending them to a Zhao-controlled company in Europe.

The SEC says Zhao and Binance dodged their own rules to let rich U.S. investors keep trading on Binance’s unregulated international platform. It’s even claimed that an executive admitted the company acted as an unlicensed securities exchange in the U.S.

The lawsuit also suggests that Binance.US was created to protect Binance and Zhao from legal issues. Two former Binance.US CEOs, likely Catherine Coley and Brian Brooks, raised concerns about Zhao’s control over the company.

Between 2018 and 2021, Binance made $11.6 billion, mostly from transaction fees. The SEC claims that Binance knowingly had many U.S. customers and didn’t act, even though it’s against federal law to offer and sell unregistered securities. Binance’s compliance efforts in 2019 were mostly for show, according to the SEC.

Lastly, the SEC accuses Zhao of setting up a plan to help rich customers evade regulations using a VPN service to hide their location and fake compliance documents to cover their tracks.

Coinbase is a publicly traded company

But people in the crypto industry are confused about the lawsuit against Coinbase. This is mainly because Coinbase is a company that has publicly traded shares.

Binance’s boss, Changpeng Zhao, responded to the lawsuit against Coinbase by teasing the SEC.

If you have to pick a fight with everyone, maybe you are the one at fault. 🤷♂️

Paul Grewal, the top lawyer at Coinbase, said that the SEC’s focus on punishing rather than setting clear rules for digital assets is bad for U.S. business. He said we need new laws that create fair and clear rules for everyone instead of lawsuits. But for now, Coinbase will keep doing business as usual.

“The solution is legislation that allows fair rules for the road to be developed transparently and applied equally, not litigation. In the meantime, we’ll continue to operate our business as usual.”

A lot of people in the crypto community are wondering how Coinbase could have gone public in 2021 if it was acting like an unregistered securities broker.

Payment apps may lack protection: A recent warning from the US Consumer Financial Protection Bureau emphasizes that the FDIC might not protect money stored in mobile payment apps. Customers could be concerned about whether their funds are insured, highlighting the risks associated with these platforms.

The US Consumer Financial Protection Bureau (CFPB) has advised Americans to keep their money in a secure, insured bank account rather than in an unprotected app.

The Bureau expressed concern over the growing use of peer-to-peer payment apps, which also handle cryptocurrency transactions, due to the increased risk of losing money if things go wrong.

The public has become more aware of the protection offered by the Federal Deposit Insurance Corporation (FDIC). This comes after the failure of several cryptocurrency platforms and a banking crisis that resulted in the loss of a huge amount of customer money.

Despite this, the CFPB warns that a lot of money is still being held in these payment apps, which aren’t covered by the FDIC.

Payment services don’t offer insurance for your funds

The CFPB says that many peer-to-peer apps like PayPal, Venmo, Cash App, Apple Pay, and Google Pay have features that work much like bank accounts, although Meta Pay doesn’t have that feature.

The companies behind these apps actually like it when you keep your money in their apps because they can then use your money for their own investments (within legal limits), while they hardly ever pay you any interest on the money you store. However, there is a risk involved for these companies, as they could potentially lose money on the investments they make.

The CFPB explains that if your money is in an FDIC-insured account and something goes wrong, whether you’re covered by their insurance is only decided after the fact.

Plus, the insurance only covers the bank’s failure. It doesn’t cover the failure of the payment app, which is usually controlled by state laws and not watched over by the federal government. Most of the time, these state laws are meant for transferring money, not storing it.

So, if you have money in PayPal or Venmo, it could be protected by this pass-through insurance when it’s in their partner banks, but not if they’ve used your money for investments. Also, it might not be clear to you where your money is actually kept.

More and more, these mobile payment services are letting you handle cryptocurrencies. But remember, payment apps may lack protection and cryptocurrencies aren’t insured, even though services like PayPal and Venmo let you keep crypto in your accounts.

In October 2022, the EU published a report to describe the risks of crypto assets investments.

According to the report. “The pseudonymity that prevails in crypto-asset markets makes it virtually impossible to assess the creditworthiness or aggregate exposures of participants.” The paper also talks about the leverage offered by crypto exchanges to individual investors, which can raise up to 125x.

While some jurisdictions try to adopt regulations to protect investors (e.g., MiCA), these regulations often fall short in the face of the ever-expanding crypto industry.

All in all, keeping your crypto investments is a very risky business, and you should be aware of the risks.

Why aren’t crypto insurance policies good enough yet?

Insurance companies still need to improve their crypto insurance plans. Right now, these plans don’t cover everything. To fully protect all your crypto assets, you might have to combine different plans. One might cover the loss of your private key, another might cover errors in smart contracts, and you might need a third in case your wallet company goes under.

What are the risks of investing in cryptocurrencies?

Cryptocurrencies are pretty risky. Their prices can go up and down much more than things like stocks. Future prices could also be impacted by changes in laws, which might even make cryptocurrencies worthless. Plus, cryptocurrencies are always at risk from cyber threats like hacking and theft.

Are cryptocurrencies insured by the FDIC?

No, they’re not. The FDIC insures normal bank accounts up to $250,000, but it doesn’t protect cryptocurrencies at all. If you’re not from the US, you should check your country’s financial authority and see their conditions for insured investments and their limitations.

Can I get insurance for my cryptocurrency investments?

Yes, you can get insurance that offers limited protection against cryptocurrency theft. But these policies often only cover specific situations. They generally don’t protect you against losses due to market changes, hardware damage or loss, sending cryptocurrency to someone else, or problems with the blockchain technology that supports the asset. If you want more comprehensive coverage, you’ll probably need to buy multiple policies.

Revolutionizing the crypto and NFT landscape, Reddit’s unique collectible avatars are on the brink of reaching a staggering 10 million users.

Reddit, a social media site, is nearly hitting 10 million users who have its special profile pictures, called “Reddit NFTs.” These were introduced in July 2022, so it’s been about 11 months.

Right now, data from Dune Analytics shows that there are about 9.9 million people who have these special profile pictures. Among these, around 7.7 million users only have one of these special profile pictures and do not have them in several accounts.

In simple words, Reddit started a marketplace for special profile pictures on the Polygon blockchain in July 2022. These pictures, known as NFTs, were made by independent artists and people who create content on Reddit.

After the marketplace started, the number of people having these pictures grew quickly but then slowed down to about 3 million by November. However, there was a big increase in 2023, with the number of accounts holding these pictures tripling in the last six months.

From the start of 2023, the number of people with these special Reddit pictures has grown by 80%. The total value of the special profile pictures market is $38.4 million, and there are 13.7 million of these pictures.

Also, there have been over 303,033 sales totaling up to $32.6 million, according to the data from Dune Analytics.

In May 2023, a Reddit user named “ContextMelodic4212” praised Reddit for its success but also pointed out that some of the growth might be because of bots.

According to this Reddit user, there are some problems with people using bots to grab or ‘scoop up’ these avatars quickly. “However, I can’t think of a better use case for this technology!”

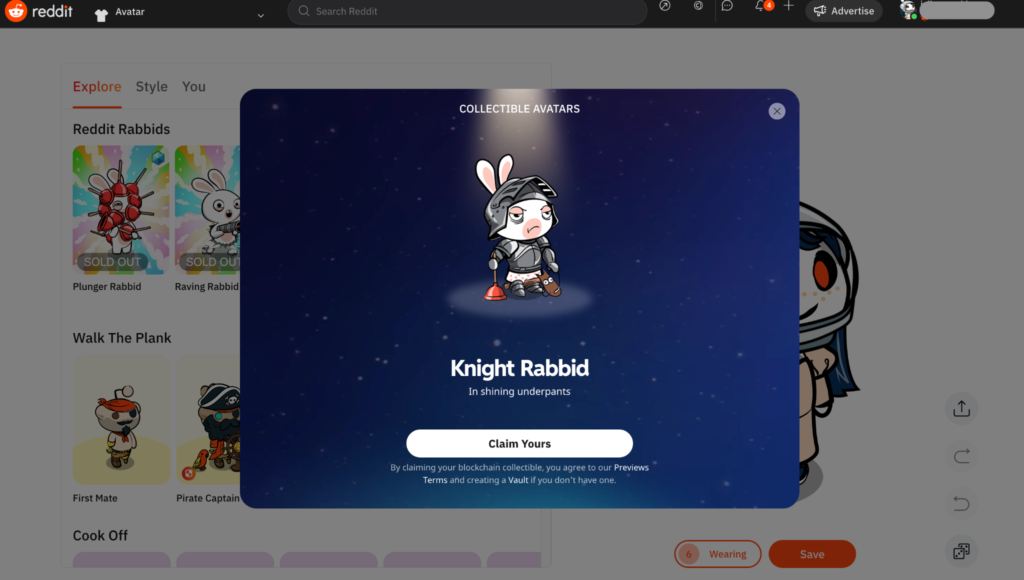

On May 26, 2023, Reddit said it will now support the Rabbids NFT collection from the big video game company, Ubisoft. Reddit users can get these Rabbids NFT pictures for their profiles for free, and people are grabbing them really quickly.

Rabbids first appeared as part of a different video game, the 2006 game “Rayman Raving Rabbids.” Ubisoft, the company that made these games, was the first big video game company to create NFT items within their games in December 2021. They made a collection of Rabbids NFT pictures for a virtual reality game called The Sandbox in February.

During a Q&A session with the India section of Reddit on May 25, Sandeep Nailwal, who helped start Polygon, said he really likes Reddit NFTs. He said that Reddit is maybe the only big tech company that has figured out how to use NFTs well, and they’ve been able to get a lot of people interested in Reddit NFTs.

He also suggested that Reddit could improve its NFTs by having a secondary marketplace and a place for artists to launch their work. He thinks these changes could make Reddit’s NFTs even better.

CryptoSnoo NFT from Reddit

But Reddit already had its own NFTs, which were launched in the summer of 2021.

CryptoSnoo are a collection of NFTs from Reddit that features the popular Snoo mascot in different contexts.

CryptoSnoos are unique cartoon avatars that take the form of the Reddit logo. These are created as non-fungible tokens (NFTs), which means they are unique digital items stored on the Ethereum blockchain. Two years ago, in June 2021, Reddit started an experiment to auction off these special avatars.

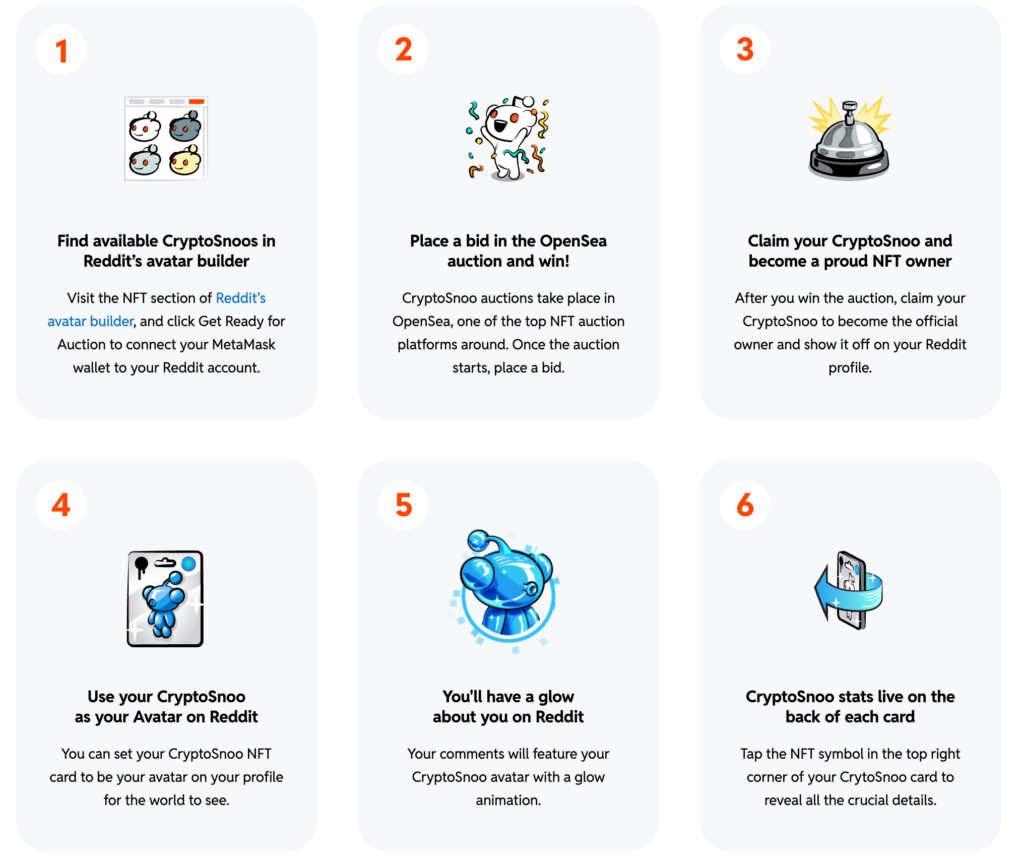

Since the Reddit NFTs were well received, the users of the popular platform can still claim their CryptoSnoos.

Three CryptoSnoos named “Original Block,” “Helium,” and “Snoopermatic” were created on June 17, 2021. These NFTs are based on the original Reddit logo that Alexis Ohanian, Reddit’s co-founder, designed in 2005. Reddit put them up for auction on OpenSea.

CryptoSnoos come in three categories: “Legendary” which means they are one of a kind, “Rare” which means there are very few of them, and “Epic” which means they are limited edition. Reddit users can find these available CryptoSnoos in Reddit’s avatar builder.

But buying an NFT from the CryptoSnoo collection doesn’t mean you own the artwork it represents. Reddit’s rules state that these NFTs are only for fun, and you don’t get any commercial rights to the artwork. Also, Reddit has the power to take away your rights to the CryptoSnoo if you say bad things about Reddit or take any legal action against them.

So, while CryptoSnoos might seem like a fun way to own a piece of Reddit history, potential buyers should understand what they are getting into before buying.

A malicious actor recently exploited Tornado Cash’s governance, enabling them to seize total control. This could potentially allow them to retrieve all the secured votes, empty the tokens held in the governance contract, and disable the router.

Tornado Cash, a decentralized crypto mixer, has faced another setback due to this incident. An attacker cunningly secured full control over the platform’s governance via a devious proposal.

The incident occurred on May 20 at 3:25 ET, when the attacker successfully attributed 1.2 million votes to a nefarious proposal. The proposal had already amassed over 700,000 valid votes, thus enabling the attacker to monopolize Tornado Cash‘s governance.

How was Tornado Cash’s governance exploited?

The disclosure was provided by @samczsun, affiliated with Paradigm, a research-oriented technology investment firm. He exposed the attacker’s claim that the malicious proposal utilized a similar logic to one that the community had previously accepted. Yet, this particular proposal contained an added function.

According to @samczsun, Tornado Cash’s governance was essentially annihilated on 2023/05/20 at 07:25:11 UTC. Through a crafty proposal, the attacker allotted themselves 1,200,000 votes. Since this number exceeds the approximate 700,000 authentic votes, they now wield absolute control.

What are the implications of this for Tornado Cash?

The assailant, by seizing control of the governance, can:

Retrieve all secured votes

Empty all tokens contained in the governance contract

Disable the router

Nonetheless, the attacker is still unable to:

Deplete individual pools

What caused this event?

When the malicious actor formulated their deceptive proposal, they alleged it was based on the same logic as a previously approved proposal. However, this wasn’t entirely accurate because they incorporated an additional function.

Upon voter approval of the proposal, the attacker leveraged the emergencyStop function to modify the proposal’s logic, which in turn awarded them with counterfeit votes.

The attacker’s complete dominance over Tornado Cash’s governance empowers them to retrieve all locked votes, empty the governance contract of all tokens, and disable the router. As per @samczsun, at the time of reporting, the attacker had “simply withdrawn 10,000 votes as TORN and subsequently liquidated them all.”

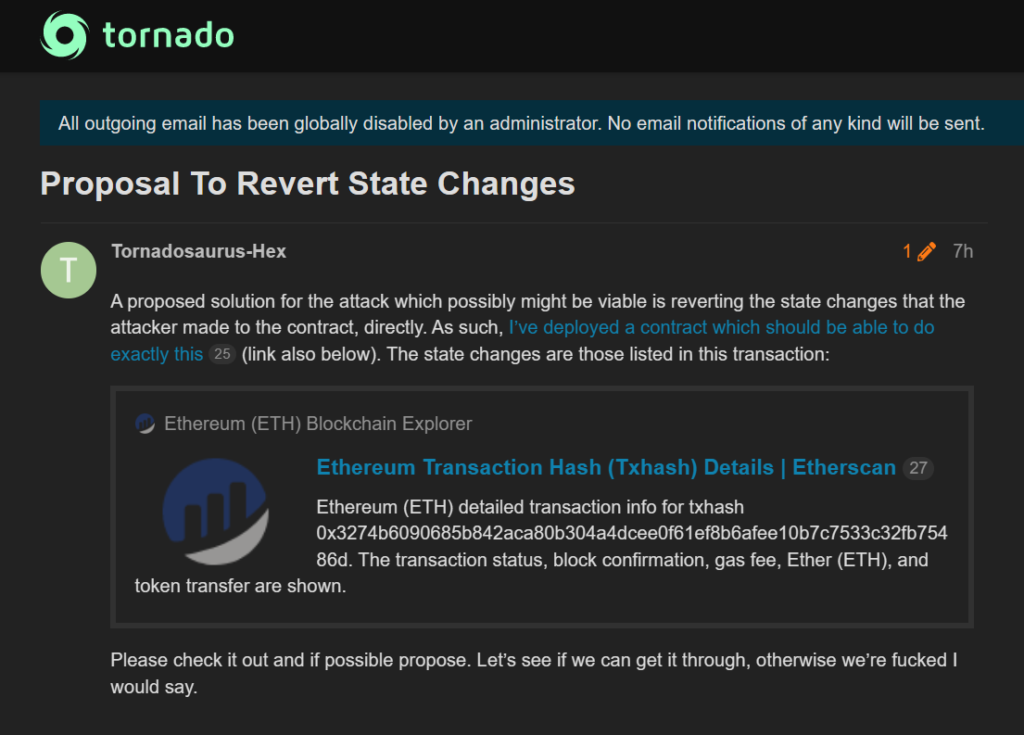

This incident serves as a crucial reminder to cryptocurrency investors to thoroughly scrutinize proposal descriptions and their underlying logic. A prominent member of the Tornado Cash community, known as Tornadosaurus-Hex or Mr. Tornadosaurus Hex, has confirmed the potential compromise of all funds in Governance. He has urged all members to withdraw any funds currently secured in governance.

The Tornado Cash community developer

They also attempted to set up a contract that might potentially reverse the changes, all the while advising the community to withdraw their funds. A distress signal from a Tornado Cash community developer, who verified these incidents, stated:

“We were aware of the protocol attack this morning. A fellow community developer and I have been contemplating solutions all day, but the situation seems nearly hopeless – as it stands, the attacker holds control over Governance.”

Currently, the team is seeking Solidity developers who can help prevent the protocol’s imminent demise. They have also expressed a need for communication with Binance, citing that this exchange possesses more tokens than the attacker.

A previous Tornado Cash developer is said to be in the process of creating a novel crypto mixing service from the ground up, aimed at addressing the “critical flaw” inherent in Tornado Cash.

The developer envisions that this solution will enable the community to protect itself from hackers who exploit the anonymity sets of honest users, without necessitating overarching regulation or compromising on crypto principles.

The next Bitcoin halving will take place in 2024. Is this a ‘buy the dip’ opportunity? With less than one year to the next big crypto event, investors are getting anxious.

Is it time to invest in Bitcoin as the halving approaches? Historical patterns suggest that Bitcoin’s price behaviour tends to follow a distinct cycle aligned with these halving events, which occur every four years.

These cycles, known as “epochs,” typically encompass a significant high and low point in Bitcoin’s value, with these events being roughly four years apart.

Interestingly, in each epoch, the significant low point usually materializes just over a year prior to the next halving. Therefore, long-standing Bitcoin advocates see little evidence to suggest a significant deviation from this pattern in the future.

Ultimately, the Bitcoin halving is just a reminder that the world’s most valuable crypto is designed to become increasingly scarce as time passes by. Even if your crypto investment isn’t in Bitcoin, this even still has a massive effect on the entire market, as Bitcoin represents almost 50% of the market.

What is Bitcoin halving?

Bitcoin is created by powerful computers which solve complicated mathematical puzzles to validate each blockchain block and generate new Bitcoins. Every four years (210,000 blocks, to be more exact), the reward for generating a new block is cut in half. Hence the name Bitcoin halving.

When Bitcoin started, miners got 50 Bitcoins for every block they added. This was a lot, but it helped attract people to the system.

For example, the first halving happened in 2012 when the reward dropped from 50 to 25 Bitcoins. The second halving, in 2016, cut the reward down to 12.5 Bitcoins. The most recent halving in 2020 reduced the reward to just 6.25 Bitcoins.

The next halving is expected to happen in 2024. This halving process will continue until we hit around the year 2140, by which time all 21 million Bitcoins should have been mined.

Why does Bitcoin halving happen?

Imagine the Bitcoin system as a digital gold mine that’s programmed to dig up a new chunk of gold every 10 minutes. As more miners (people with powerful computers) join the hunt, they’re able to dig up gold faster. But to keep things fair and maintain the 10-minute digging goal, the digging process is made harder every couple of weeks. Despite the growth of the Bitcoin network over the past decade, the average digging time has stayed below 10 minutes, around 9.5 minutes, to be exact.

Now, the total amount of Bitcoin that can ever exist is capped at 21 million. When this number is hit, no more Bitcoin can be created. Bitcoin halving is a process that gradually reduces the amount of new Bitcoin that can be mined each time a block is added to the blockchain. This makes Bitcoin scarcer and potentially more valuable over time.

You might think that halving the reward for mining would make people less interested in doing it. But Bitcoin halvings have historically been associated with big jumps in Bitcoin’s price. This keeps miners motivated to mine more, even though they’re getting less Bitcoin each time they mine a block.

So, miners are encouraged to keep digging as long as the price of Bitcoin keeps going up. If the price doesn’t rise and the reward for mining keeps getting smaller, miners might be less interested in mining Bitcoin. This is because it takes a lot of time, computer power, and electricity to mine Bitcoin.

If you want to know more about Bitcoin, check out this Bitcoin hard fork guide, which explains all past forks which affected all BTC holders.

Should I buy Bitcoin?

Investor and entrepreneur Alistair Milne shared his perspective, recommending that those seeking to benefit from Bitcoin should consider purchasing now, as the period preceding the halving might not present as advantageous an entry point. He advised, “Avoid shorting when it’s dark green and ensure you’re fully invested before it turns blue.”

In the earlier part of the month, a well-known yet contentious figure in the Bitcoin industry used the halving narrative to argue that the pricing cycles aren’t a matter of coincidence. PlanB, the anonymous creator of the Stock-to-Flow (S2F) Bitcoin price prediction models, noted that about half of the market participants believe the link between halvings and price is random.

Why is bitcoin S2F/halving not priced in?

Because ~50% thinks the BTC price jumps after last 3 halvings (red) are a coincidence. Halvings are key to S2F, but these critics focus on auto-correlation between halvings and conclude there is no relation between S2F/halvings and… pic.twitter.com/8VaIy6oM5i

PlanB’s comments were framed within the debate over the relevance of the S2F theory to halvings, a theory that has faced considerable criticism due to unmet price predictions from 2021 onwards. However, PlanB also asserts that the current BTC/USD value is low, and the market hasn’t adequately factored in the upcoming halving.

PlanB questioned, “Why is bitcoin S2F/halving not priced in? Because ~50% thinks the BTC price jumps after last 3 halvings (red) are a coincidence.

Why isn’t the Bitcoin S2F/halving reflected in the price? Approximately 50% believe the price spikes following the last three halvings are coincidental,” adding an explanatory chart to his statement. He continued, “Halvings are key to S2F, but these critics focus on auto-correlation between halvings and conclude there is no relation between S2F/halvings and price. I disagree, obviously. 2024 halving will be very interesting!”

What does the Bitcoin halving event mean?

Think about Bitcoin miners like gold miners. They get paid in Bitcoin for their hard work of adding new transactions to the blockchain. But when Bitcoin halving happens, miners earn less for their work. This means fewer new Bitcoins enter circulation, similar to how less gold would be available if miners dug up less gold.

Here’s where the basic rules of supply and demand come in.

When the supply of something goes down, but demand stays the same or even goes up, the price usually goes up.

The halving event also slows down how fast new Bitcoin is made, which helps control inflation. Inflation is like when a dollar can’t buy as much as it used to. But Bitcoin is designed to be the opposite – it’s supposed to become more valuable over time. The halving event helps make this happen.

For instance, Bitcoin’s inflation rate was 50% in 2011, but it dropped to 12% in 2012 after the first halving and 4-5% in 2016 after the second halving. Currently, it sits at around 1.77%. So, after each halving, Bitcoin tends to become more valuable.

However, this process isn’t without its issues. Mining Bitcoin uses a lot of electricity, and miners might struggle to break even if the reward they’re getting is halved but the price of Bitcoin doesn’t go up enough to cover their costs.

Also, because of this, miners will be on the lookout for newer, more efficient technologies that can help them mine more Bitcoin while using less energy.

Besides, Bitcoin’s growing popularity and its acceptance by more businesses and big institutions might also push its price up. More transactions are likely to happen as more people start to use Bitcoin and blockchain technology.

Time to buy Bitcoin?

Bitcoin, the world’s largest cryptocurrency, is currently at a low point, trading around $27,300, after dropping almost 2% recently. This dip came as Binance, a significant cryptocurrency exchange, temporarily stopped Bitcoin withdrawals twice in one day due to technical issues. However, these operations have since resumed, and there are signs that Bitcoin could be gearing up for a recovery.

Despite the recent dip, Bitcoin showed promising resistance last week at $29,000, indicating the potential to climb back to $30,000.

Many Bitcoin investors are hopeful due to anticipated pauses in U.S. interest rate hikes and shifting trust from traditional finance to decentralized finance (DeFi). Combined with the upcoming Bitcoin halving event in 2024, which typically brings a surge in Bitcoin’s value, some experts predict Bitcoin could reach $35,000.

Still, it’s important to remember that Bitcoin is trading 50% lower than its all-time high of $69,000 in November 2021, and the journey to recovery may be lengthy. Also, external factors such as regulatory changes in countries like India could influence the market.

So, is it time to buy Bitcoin? It seems like a potentially advantageous time, given the low price and positive future prospects. But, as always with cryptocurrencies, it’s crucial to be vigilant and cautious due to their volatile nature. It’s best to stay informed about the current macroeconomic conditions and regulatory developments.

Zimbabwe’s central bank is launching a digital currency backed by gold.

They plan to start selling these digital coins to investors on May 8th, 2023. Individual buyers can get them for at least $10, while companies and other groups need to spend a minimum of $5,000.

The Reserve Bank of Zimbabwe announced that people can buy these gold-backed digital coins with U.S. dollars or local currency.

However, if using local currency, the price will be 20% higher than the average market rate. Investors can join in and buy these coins starting May 8th, but the opportunity will end two days later.

The “willing-buyer willing-seller interbank mid-rate” is a middle point between the rates banks are ready to buy and sell different currencies to one another.

It depends on factors like how much of a currency is available and how much people want it. This rate helps set prices for many financial deals, and banks and other financial institutions often use it as a reference.

On April 28th, the Reserve Bank of Zimbabwe shared their plans to create a digital currency supported by gold, which can be used as official money in the country.

Zimbabwe has faced issues with unstable currency and high inflation for over a decade. After a period of extreme inflation, the country started using the U.S. dollar in 2009. Nigeria was the first African country to introduce its own digital currency, called the eNaira, in 2021.

Zimbabwe and hyperinflation

This new digital currency is part of Zimbabwe’s efforts to strengthen its local currency. Zimbabwe has been trying hard to overcome the effects of hyperinflation over the past decade.

In 2009, Zimbabwe replaced its valueless local currency with the U.S. dollar. However, their economy has faced difficulties due to a significant shortage of U.S. dollars in the country.

In early 2019, Zimbabwe’s central bank revealed plans to reintroduce the Zimbabwe dollar as legal tender, after using the US dollar and seven other global currencies for a decade. The reason for this change was that extreme hyperinflation had severely weakened the local currency.

However, many people ignored this, the black market flourished, and the local currency devalued quickly. The government then allowed the use of the U.S. dollar again.

Due to the previous severe inflation, many people now prefer to find scarce U.S. dollars on the illegal market for their savings or daily transactions. Confidence in the Zimbabwe dollar is so low that numerous retailers and even some government institutions don’t accept it.

On the official market, the exchange rate is slightly above 1,000 Zimbabwe dollars to the U.S. dollar. But on the thriving illegal street market, it’s about double that amount in local currency.

Zimbabwe has tried unusual ideas to prevent its currency from losing value.

In July 2022, Zimbabwe introduced gold coins as legal tender to stabilize the local currency and preserve its value. However, many people found them too expensive to purchase everyday items like bread.

In March 2023, the Monetary Policy Committee approved a plan to support Zimbabwe’s local currency.

This came eight months after the country introduced gold coins as a way to maintain the currency’s value. This plan seemed to have worked. In January 2023, according to the Committee’s monthly report, the price of gold increased by 5.7% (from US$1,795.97 to US$1,898.95 per ounce). While the price in February has slightly retreated (by 2.3%), the Committee decided to go through with its plan.

According to the bank’s statement, the pricing of the gold-backed tokens in Zimbabwe will be based on international gold prices set by the London Bullion Market Association.

Both Mastercard and Visa continue to expand their presence in the crypto sector with new initiatives and collaborations.

Visa’s crypto division is building the “next generation of products” for digital commerce and is seeking to hire software engineers with Web3 and blockchain experience.

Mastercard launches “Mastercard Crypto Credential,” a Web3 user verification solution designed to enhance user verification standards and reduce opportunities for bad actors in the digital asset space.

Mastercard partners with crypto wallet providers Bit2Me, Lirium, Mercado Bitcoin, and Uphold, as well as blockchains Aptos, Avalanche, Polygon, and Solana.

Visa is paving the way for the mainstream adoption of stablecoin

Visa is working on a new crypto project that aims to make public blockchain networks and stablecoin payments more popular and widely used.

As a major global payment company, Visa is looking into how cryptocurrencies can be helpful by focusing on a new plan related to stablecoin payments. On April 24, Cuy Sheffield, the person in charge of crypto at Visa, shared news about this new project on Twitter.

We have an ambitious crypto product roadmap @Visa and just opened a few reqs for senior software engineers to help us drive mainstream adoption of public blockchain networks and stablecoin payments. https://t.co/UQRJNcOJtB

Visa is working on a new crypto project that aims to make blockchain networks and stablecoin payments more common and widely accepted. Sheffield, who’s in charge of the project, mentioned this in a tweet.

On April 20, Visa shared a job ad, saying they’re creating new, advanced products to help with everyday digital shopping.

To create this product, Visa wants to hire software engineers who know about programming, backend systems, and Web3 technologies. Sheffield tweeted that they’re especially interested in those with experience using Github Copilot and other AI tools for writing and fixing smart contracts.

Ideal candidates should know about layer 1 and layer 2 solutions and have experience with Solidity, a programming language used for smart contracts on the Ethereum Network. Solidity helps create smart contracts on blockchain platforms and keeps track of transactions in the system.

The job also needs candidates to know about different types of distributed ledger networks (public and permissioned), security measures, handling private keys, and new improvements in Ethereum, like ERC-4337.

Visa, one of the biggest payment companies, started getting involved with crypto in 2020. They teamed up with blockchain company Circle to allow USD Coin (USDC) stablecoin on some credit cards.

Visa has been slowly growing its crypto services, but they stopped some new partnerships because of the 2022 crypto market downturn and big failures like Celsius and FTX.

Mastercard is enhancing user verification and strengthening security in the digital asset space

Mastercard’s new approach focuses on offering safe transactions between users, verified based on the company’s standards.

The worldwide financial company, Mastercard, introduced a new Web3 solution to improve user verification and limit chances for wrongdoers in the digital asset area.

They announced the “Mastercard Crypto Credential” solution on April 29. In a video shared on Twitter, the company explained that they are creating a method for Web3 and blockchain services to ensure secure transactions between users, following Mastercard’s verification standards.

With this solution, users get a unique “Mastercard crypto credential” identifier, allowing them to quickly check if a receiving address is approved by Mastercard and follows the company’s rules. Mastercard’s solution also supports regulatory compliance by exchanging important metadata needed to meet requirements. This helps limit chances for wrongdoers and reduces the risk of losing funds permanently.

If any bad actors manage to get a unique identifier, Mastercard can quickly take away their verification if they’re found involved in harmful activities. The company has partnered with many others for this solution:

For crypto wallets, they’ve joined forces with Bit2Me, Lirium, Mercado Bitcoin, and Uphold.

For blockchains, they’ve teamed up with Aptos, Avalanche, Polygon, and Solana.

Mastercard also plans to use CipherTrace’s services, including CipherTrace Traveler, to verify addresses and ensure compliance with the Travel Rule for cross-border transactions.

Over the past few years, Mastercard has been increasing its involvement in the crypto sector. Recently, they announced a nonfungible token (NFT) musician accelerator program in partnership with Polygon.

The program provides free access to resources, unique AI tools, and other experiences for holders of Mastercard’s Music Pass NFT until the end of April.

The 2020-created regulatory package now awaits the European Council’s approval before being enforced. Following two previous postponements, the European Parliament has held the final vote on the Markets in Crypto-Assets Act (MiCA).

The legislation, initially proposed in 2020, must be approved by the European Council before taking effect.

The vote took place on April 20. Stefan Verger, the European Parliament member and crypto advocate, said this to be a milestone for the crypto industry.

What’s the point of the Markets in Crypto-Assets Act (MiCA)?

MiCA aims to establish standardized regulations and harmonized rules for crypto assets across the European Union (EU), providing legal certainty for the crypto industry and investors.

The regulation will set guidelines for the operations, structure, and governance of digital asset token issuers and impose rules on transparency and disclosure requirements for crypto issuance and trading.

MiCA’s specific provisions regarding stablecoins will be enforced in July 2024, while other provisions, including those for crypto asset service providers, will come into effect in January 2025.

The regulation has been met with cautious optimism. However, the regulations mentioned in the 400-page document have also presented concerns by specialists.

For instance, the current draft, which was submitted to vote, does not mention decentralised finance (DeFi), address the growing crypto lending and staking sector, or establish rules for nonfungible tokens.

The industry speaks strongly for the need for cooperation between governments, regulators, and industry stakeholders. This was one of the topics at Paris Blockchain Week 2023.

While the future is uncertain, EU officials say that MiCA should help mitigate the negative impacts of incidents such as FTX’s insolvency in the future.

Limitation of MiCA

MiCA will become the first comprehensive pan-European crypto framework, set to take effect in 2024. During the latter half of last year, when most of the MiCA text had been drafted, the industry experienced several shocks, creating new challenges for regulators.

However, given the rapid expansion and dynamic nature of the crypto industry, there will always be new issues that will need to be addressed.

This raises the question of whether MiCA, given its current imperfections, can be considered a truly “comprehensive framework” a year from now.

More importantly, will it be an effective set of rules to prevent future failures similar to those involving TerraUSD or FTX?

EU DeFi regulations need to improve

A significant oversight in the MiCA is its treatment of decentralised finance (DeFi). The current draft largely omits any mention of this more recent organisational and technological development in the crypto space, which could pose a problem when MiCA is implemented.

If and when more users turn to DeFi, after the countless failures of the centralized platforms, customers will need regulations to receive protection. And there’s also the money laundering issue. However, given the decentralisation of DeFi, regulating this branch is a huge hurdle for authorities. Customers are still new to the crypto market, and many take their first contact using centralised exchanges.

But the absence of a specific section devoted to DeFi does not imply it is impossible to regulate. DeFi is essentially a collection of derivatives, bonds, loans, and equity financing presented as something new and innovative. In this sense, industry thought leaders believe that the yield-bearing, lending, and borrowing of collateralised crypto products are areas of interest for investment and commercial banks and should be regulated similarly. In this context, the suitability requirements outlined in MiCA could be helpful. For example, DeFi projects might be classified as providing crypto asset services in MiCA’s terminology.

Lending and staking

DeFi might be the most prominent, but it is not the only shortcoming of the forthcoming MiCA. The EU framework also neglects to address the burgeoning sectors of crypto lending and staking.

Considering recent failures involving lending giants like Celsius and the increasing attention of American regulators to staking operations, EU lawmakers will need to develop appropriate regulations as well.

The market collapse last year was driven by poor practices in this space, such as weak or non-existent risk management and reliance on worthless collateral.

On the other side of the financial system are banks. Legacy commercial or investment banks and even “traditional” fintech companies face more stringent regulations. Some believe the EU should provide a standard that should apply to all these services and products, which includes both investment banks and crypto platforms offering lending and staking services.

Non-fungible tokens (NFTs) are another area to monitor. In August 2022, European Commission Adviser Peter Kerstens revealed that despite the lack of a specific definition in MiCA, NFTs would be regulated like cryptocurrencies in general. In practice, this could imply that NFT issuers would be considered crypto asset service providers and required to submit regular reports of their activities to the European Securities and Markets Authority through their local governments.

Is the EU’s regulation (MiCA) a good thing?

While MiCa still has some unresolved issues, the industry is moving forward and helping legitimise the market.

However, it’s necessary that European lawmakers keep pace with regulatory updates. There’s a need for a more robust approach to some of the technical standards and guidelines currently being developed as part of the MiCA regime. The process of developing and putting these regulations in place is also slow in the EU.

On the other hand, the EU has legislation for the crypto industry, whereas other economic powers do not.