NYU law professors Richard Epstein and Max Raskin published a paper to explain the potential hazards of central bank digital currencies, highlighting the risk of overstepping governmental boundaries and the importance of maintaining the ‘separation of money and state’.

Central banks worldwide are swiftly progressing with their explorations in creating digital currencies.

Numerous examples, such as the recent announcement of a successful prototype by the New York Federal Reserve or the Bank of England’s achievement in the subsequent phase of its digital pound trial, indicate that over 130 nations globally are considering the idea of central bank digital currencies (CBDCs).

The reasoning behind this is twofold.

Firstly, central banks can position themselves as protectors of consumers and innovators in cost-saving technologies by eliminating the role of private banking intermediaries.

Secondly, they can acquire an additional mechanism for policymaking.

However, the proposition of excluding these intermediaries raises an important question of who would be responsible for the other end of the financial transactions.

The inevitable answer is a far-reaching and intrusive government capable of monitoring every single expenditure.

Digital cash?

Max Raskin, an adjunct professor of law at New York University and a fellow at the school’s Institute for Judicial Administration, and Richard Epstein, a law professor at New York University, a senior fellow at the Hoover Institution, and a senior lecturer at the University of Chicago, are exploring this topic in a paper called “A Wall of Separation Between Money and State: Policy and Philosophy for the Era of Cryptocurrency,“ published in The Brown Journal of World Affairs.

Their argument suggests that a central bank, for instance, the Bank of England, would issue a “digital pound,” which would be a direct claim on the central bank, much like current cash is.

This process would involve creating the necessary infrastructure for individuals to store digital pounds in digital wallets and facilitate interactions with retailers and other users.

Contrasting current practices where central banks such as the Federal Reserve and the Bank of England do not offer accounts to direct depositors, the proposed model would eliminate the costly private banking system that presently stands between the central bank and the accounts held by businesses and individuals.

At a glance, it seems that CBDCs might cut unnecessary costs.

However, these apparent efficiency benefits can be deceptive and hazardous.

Intermediaries function in thousands of markets, with representatives, aggregators, and monitors in almost every significant business line. These participants can’t be easily deemed obsolete.

Intermediaries often provide value as they are motivated to offer more than the bare minimum to stand out – such as new banking products and services.

The variety of services banks can offer due to competitive pressures that ultimately benefit consumers. Restricting these forces can hamper the market economy.

CBDC implementation can be risky

The implementation of CBDCs is not without risks.

The idea of providing extensive power and confidential information to a faceless government entity can be alarming. The system can use that data against you in numerous ways.

By removing the private banking intermediaries, CBDCs would eliminate a crucial barrier that currently safeguards individuals and firms from government intrusion and overstepping.

The use of cash and bearer instruments is currently untraceable by the central government.

However, the use of digital cash would be.

It’s clear that even those who decide to stick with private bankers will still be scrutinised by the state, which holds control over all transactions.

Moreover, these digital funds would empower central banks to direct personal loans and mortgages to specific private parties with minor competition, raising concerns around state industrial policies. It’s not hard to imagine potential nightmare scenarios, yet they are difficult to avert.

The question remains: can we trust thousands of new banker-bureaucrats to perform any better?

Can we trust banks?

The Bank of England, in its digital pound argument, emphasised the British government’s commitment to fighting climate change, stating that the digital pound would be designed with this objective in mind.

Why should a topic as intricate and contentious as climate change be regulated through the financial system?

Similarly, U.S. financial regulators have started to wade into political issues like climate change.

If such explicit political objectives are considered, it is not a stretch to imagine a government-run bank using its powers to favour certain energy producers and punish others through their bank accounts.

The power to impact credits and debits must be a feature of the central banks’ proposed code, which introduces a covert system of industrial policy.

If CBDCs become a reality, officially favoured energy sources like solar and wind power could witness their bank accounts receiving subsidies without the need to attract private investors or undergo the scrutiny of the private banking system.

Bank accounts could become vulnerable to political manipulations, bureaucracies, or even disenfranchisement overnight with limited recourse.

Furthermore, these CBDC initiatives in the U.S. were originally proposed in the context of directly providing pandemic stimulus to the economy. However, the evidence is overwhelming that this hasty system of government payments was incredibly wasteful.

Moreover, central banks could implement countercyclical monetary policies, such as providing cash boosts to individuals in specific regions or sectors, which again becomes a political football.

Money and new technologies

We should undoubtedly strive to leverage new technologies, but only when implemented correctly. According to the paper in the Brown Journal of World Affairs, “Money should be a neutral unit of measurement, like inches or kilograms.”

This concept, referred to as the “separation of money and state,” aims to stabilise all currencies over time, minimising the need for private parties to design complex and costly mechanisms like adjustable-rate mortgages to handle financial instability.

For instance, Bitcoin has a predetermined supply of no more than 21 million units, not governed by any individual institution but rather by the network’s consensus mechanism.

This feature provides a robust defence against value dilution that no government-centric system could hope to match.

This fixed system could offer additional institutional support for developing countries seeking modernisation.

Countries with a history of mismanaging their monetary systems could benefit from the discipline that comes with certain forms of digital currency.

For instance, a central bank like Zimbabwe‘s or Argentina’s, plagued with mismanagement, could adopt an innovative form of dollarisation using Bitcoin or another form of programmed cryptocurrency.

Why are NFT prices falling? What to avoid when buying NFTs from a crypto project?

Remember the popular NFT collection called Bored Ape Yacht Club (BAYC)?

This collection became extremely valuable in early 2022, but as of 2023, its popularity has faded, causing prices to drop dramatically.

The lowest price for one of these NFT artworks, also called the ‘floor price’, has fallen from 153.7 ETH (a type of digital currency) to 27.4 ETH.

This ‘floor price’ helps indicate the overall worth of the art collection, so a big drop in the floor price means that the value of individual pieces has also taken a big hit.

One popular example of a BAYC NFT price decrease that has been circulating on social media is a piece owned by Justin Bieber, which was once valued at $1.3 million and is now only fetching offers of around $58,000.

That being said, those who bought these artworks early are still doing okay, as these pieces are still quite valuable compared to other NFTs.

However, this isn’t the only digital asset that’s seen prices skyrocket and then crash in recent years. In fact, it’s pretty much keeping pace with the overall NFT market, which is at its lowest in two years.

However, there are important lessons to be learned from this situation.

Many people, especially those who invested heavily, have paid a steep price to learn these lessons. So if you can learn from their experiences without losing money yourself, it’s wise to do so.

Beware of projects which use extreme marketing

The Bored Apes always had an intense marketing campaign going on.

Such unnatural hype can artificially inflate an asset’s value and make its market more fragile. For digital assets like these, it can result in investors who don’t really understand what they’ve bought into.

It encourages risky speculation over genuine engagement, weakening the market. A stable market should be built on cultural value and real affection for the asset, not just a flashy advertisement.

Additionally, when these NFTs are showcased in mainstream media, it might prompt wealthy individuals to buy many, raising the entry price for new investors and creating potential points of failure.

For instance, when a major Ape owner rapidly sold dozens of NFTs earlier this year, it drove the market to a five-month low.

A healthy digital art market needs a diverse community of engaged, individual owners, not a bunch of speculators ready to sell at the first sign of trouble.

Don’t rely on digital assets to maintain a stable value

Some Bored Ape owners have used their Apes as loan collateral and are now facing losses as values fall.

For example, BendDAO, a loan service, is selling dozens of Apes that were taken as collateral for unpaid loans.

This is just one of many similar services, and these forced sales might even be causing Bored Ape values to spiral downwards.

The notion that NFTs could be used as reliable financial tools this early in their existence is highly doubtful, even though providing such a service might be profitable.

But borrowing against a volatile asset, whether it’s a digital one or not, is a terrible idea.

Now these borrowers are seeing their Apes being sold off at the market’s lowest point instead of potentially waiting for a better time.

Joining late can be costly

Those suffering the most right now are the latecomers who bought Apes NFTs at peak prices.

Some have suffered larger losses than even Justin Bieber, and it’s unlikely they’ll recover their investments.

The issue with this is that investors, especially new crypto investors, will find it challenging to identify when a market is overpriced.

However, there are a few red flags to watch out for. Be wary if you see heavy marketing (such as an Ape being promoted on late-night TV shows). Such hype could be driving up the asset’s price beyond its real value.

A cautious approach is to realize that if others are already making huge profits, it’s probably too late for you to benefit from that surge, regardless of the asset. You might end up being the one left holding the bag.

This is especially true for community-driven NFTs.

If everyone around you is buying into a rising asset expecting future profits, they’re probably all doing the same thing.

A bubble in NFTs can actually harm the organic growth of its community.

Of course, another aspect is also the utility of that said digital asset. While some projects have a blockchain game, such as Footballcoin, which gives true utility to their NFTs, most do now.

Most projects will use words such as “unique” or “innovative” to describe their assets but will spend little time explaining the mechanics of the project. These are other red flags that you should consider when judging an NFT project.

Don’t mix arrogance with digital assets

Remember the exclusive BAYC yacht parties?

Some of the negative feelings towards Apes stem from typical behavior seen during a booming crypto market, such as over-the-top parties.

However, Ape owners also seem to have earned a reputation for being unusually arrogant and self-centered. To many people, an Ape picture is like a rude tweet mocking those who don’t understand why a digital monkey image could be worth half a million dollars.

While this behavior might have been a reaction to widespread ridicule towards the Apes, it was a strategic blunder (similar to what we see with Bitcoin). Now, the lack of goodwill towards Apes, whether within the crypto community or in general, is resulting in less financial support for these assets.

This is because the community of owners plays a vital role in the value of NFTs like these. For instance, the communities of other NFT collections, like Wassies and Miladies, have done a much better job at maintaining their value compared to Apes over the past year, although they started from a lower price point.

This may not be a lesson you’d learn in a traditional market, but it’s an important one. Most of us are now paying more attention to the Apes’ downfall partly because of how the owners behaved when things were going well.

Navigating the dynamic landscape of the crypto industry, we explore the crucial role of security, education, and regulation in mitigating escalating crypto scams. How can these new-age digital assets, despite their rapid evolution and growth, can be protected from the increasing threats posed by bad actors?

The amount of money stolen by criminals in the cryptocurrency world has gone up a lot in the past two years. Even so, people who specialize in online security aren’t worried. They say that new technology often gets taken advantage of when it’s first introduced.

CertiK, the blockchain security company, published a report about online security in 2022. According to the report, wrongdoers stole more than $3.7 billion from Web3 technologies last year. This was a huge jump – 189% more than the $1.8 billion stolen in 2021.

In another report about the first three months of 2023, CertiK said that hackers got their hands on over $320 million.

You can also watch the key findings in the 2022 Certik report on their YouTube channel: https://youtu.be/lWZscaMAR0s

While this is worrying tech developers and investors, it’s also a normal phenomenon. The more projects and technologies are launched, the more there will be people who will search for ways to misuse that technology. This is because new stuff often has weaknesses and opportunities for misuse.

We’ve seen this pattern before, from the beginning of the internet to the spread of email and, most recently, with the introduction of blockchain and digital money.

At the same time, we need to remember that the crypto industry is still new. Some people in the industry are more interested in growing and creating new things than they are in making sure everything is secure. This could be why we’re seeing so many thefts.

Statista, a company that collects data, offers data that may anticipate more growth in the crypto industry. According to their report, the cryptocurrency market is projected to reach US$37.87 bn in 2023. The number of cryptocurrency users is expected to reach 994.30 million by 2027.

Why are there so many scams in crypto?

The fast growth in the number of users and earnings in the crypto industry, along with its new ideas, may lead to more misuse. In the end, we must remember that blockchain technology and smart contracts, which is the infrastructure for digital currencies, are very complicated.

This complexity can lead to weak security spots that talented hackers can misuse. Because digital currencies have real value and can be exchanged for fiat money in many parts of the world, they’re tempting for hackers who can quickly take and possibly cash in the stolen digital money.

In the future, the crypto world will become more secure, and as Web3 gets more mature, there will be fewer successful hacks, misuses, and scams.

However, there will always be a never-ending fight between the wrongdoers and the blockchain security experts, as they both work towards their goals in this constantly changing industry.

But industry leaders see it as a wake-up call for us to double our efforts to secure our funds. And for the financial authorities to oversee these game-changing technologies and make it possible for everyday users to access them safely and responsibly.

Artificial Intelligence – is it secure?

Artificial intelligence (AI) has been a hot topic recently. Some people are talking about how it might change the way we work, while others, like tech entrepreneur Elon Musk, are saying we should be careful about how it’s developed.

We will probably see AI gets used more and more, and it’ll probably face its own security problems, just like Web3 and other new types of technology.

As AI becomes a bigger part of our everyday lives, especially in areas where security is important, like self-driving cars or financial systems, the chance for hacks, misuse, and scams will likely go up.

AI systems can be taken advantage of in several ways, from messing with machine learning algorithms to data tampering and hostile attacks.

Sensitive data can also be accidentally shared from large language models as people interact and share info with AI chat platforms like ChatGPT.

However, as long as there is no immediate money-making opportunity with AI, scammers will probably not start using AI just yet.

But AI can certainly aid any researcher in doing their job, whatever that may be. For instance, AI capabilities may allow for a more advanced set of attack methods. Machine learning can be used by security researchers to check smart contracts to find weak spots more efficiently,

The pain points of the crypto industry

The cryptocurrency industry, being relatively new, is experiencing a number of pain points.

These include:

Rapid Evolution. The speed at which the industry evolves makes it challenging for security measures and best practices to keep up, leading to vulnerabilities.

User Knowledge. Users are still learning how to use crypto technologies safely, making them easy targets for exploitation.

Smart Contracts. Their open and visible nature means that if a contract has a flaw, it can be exploited by anyone, at any time.

Decentralization. Unlike traditional systems that can add extra layers of security through centralized servers, the decentralized nature of blockchain technologies can expose them to more threats.

However, the industry is continually improving its security practices, with some decentralized finance (DeFi) platforms implementing additional measures such as multi-signature wallets and time locks.

In addition, there’s an increased focus on regulatory scrutiny and user education to reduce future scams and hacks.

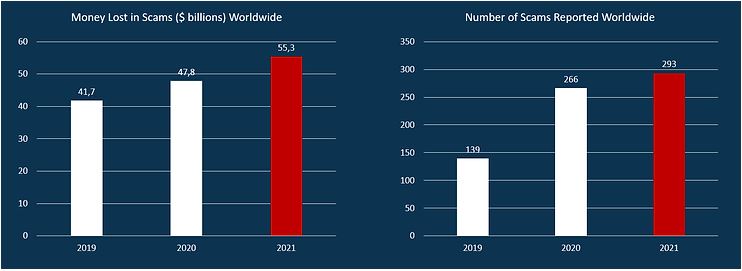

Crypto scams get more attention than traditional thefts

But crypto scams represent only a fraction of the total financial scams. The traditional money system continues to set records for losses through malicious actions each year.

Crypto is often highlighted in the news for theft and fraud, but the total losses are actually much less than fraud involving credit cards, automated clearing house transactions, and wire transfers worldwide.

Source: Global Anti-Scam Alliance

According to the Global Anti Scam Alliance, a nonprofit group dedicated to protecting consumers from financial crime and scams, traditional money lost to scams has been increasing, with $47.8 billion lost in 2020 and $55.3 billion in 2021.

The United Nations estimates that globally, the amount of money laundered around the world in a year is guessed to be 2 – 5% of global GDP, which is about $800 billion – $2 trillion in today’s US dollars. However, since money laundering is done in secret, it’s hard to figure out the total amount of money that’s actually laundered.

What draws so much attention to crypto scams is the very thing that attracted investors in the first place – its transparency.

Crypto transactions happen on the blockchain and are visible to everyone. This transparency can help track stolen funds and may explain why losses in crypto get more attention.

When a major theft occurs, everyone around the world can help track the funds to see exactly where they go. This isn’t possible in traditional financial systems where fund movements happen behind closed doors on private networks.

As more people around the world start using crypto, total losses will probably increase accordingly. However, better education and understanding of cryptocurrencies will ensure this increase isn’t disproportionate to other payment methods.

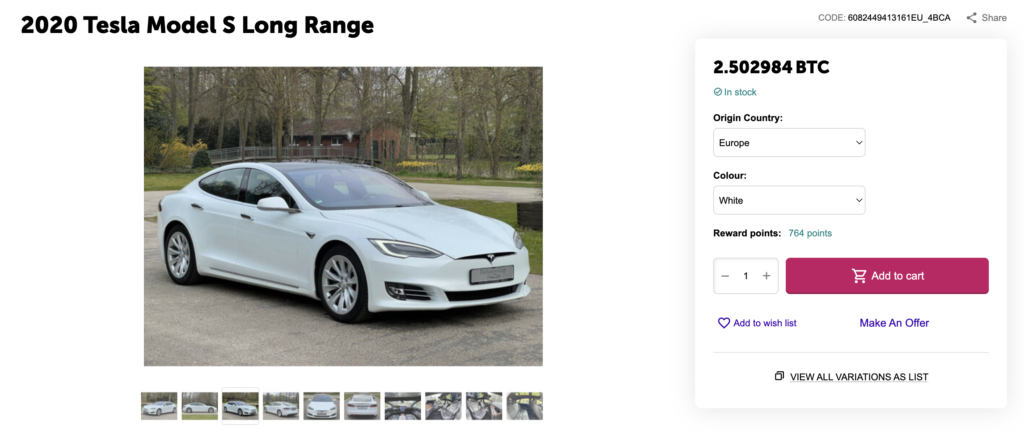

Are you planning on buying a car with Bitcoin? Cryptocurrency is now used to buy real-world assets such as cars and even real estate. While this payment method isn’t accepted worldwide, more and more services are starting to consider it. And car dealerships are no exception.

In 2021, Tesla’s CEO, Elon Musk, announced that it would accept Dogecoin as payment for Tesla. Meanwhile, the offer is no longer standing, but that doesn’t mean you can’t use Bitcoin to buy a car in 2023.

Is it legal to buy a car with Bitcoin?

Yes, it is indeed legal to purchase a car using Bitcoin. You can also use other popular cryptocurrencies, such as Dogecoin and Shiba Inu. However, similar to any other online transaction, it is important to exercise caution and adopt certain safe practices.

The first thing you need is to find a reputable car dealership that accepts Bitcoin as a payment method.

You can do this by checking out reviews on third-party consumer forums to discover the best places to purchase cars with cryptocurrencies. Platforms such as Crypto Emporium and BitCars have supported crypto payments for some years now and have excellent reputations in the market.

One of the advantages of using cryptocurrencies like Bitcoin for transactions is that they are generally secure. This means that you do not need to disclose any personal financial information, as transactions take place directly between two digital wallets. This method of payment contributes to your safety and security during the transaction.

While there is no car manufacturer that accepts cryptocurrency throughout their distribution network as a whole, there are specific car dealerships that have implemented cryptocurrency payment services to serve customers who wish to complete their purchases using digital assets.

In the end, it’s up to you to find a platform that allows crypto payments for products such as cars. Some of the most popular options for such purchases include:

One of the most popular payment services is BitPay, which is already used by some Lamborghini and BMW dealerships thought Europe, the UK and the USA.

Finding out if a car dealership accepts Bitcoin or other cryptocurrencies is simple. The quickest way is to call local dealerships and ask. Salespeople might need to check with management, but they should give you an answer soon.

You can also look at car dealership websites to see if they accept Bitcoin. However, these sites mainly focus on selling cars and might not clearly mention payment methods, so it could be a bit frustrating unless the dealership prominently displays this option.

How to buy a car with Bitcoin (or any other cryptocurrency)

Buying a car with cryptocurrency can be done from a dealer that accepts it or from a private seller who is comfortable with crypto. Usually, dealing with a dealer is easier. Here’s a simplified plan:

Find out which dealerships accept cryptocurrency.

Research different cryptocurrency exchange apps and learn how they work. The dealer might prefer a certain app like BitPay. Depending on the payment processor, you might need to set up an account.

Confirm that the dealer accepts the cryptocurrency you own. Bitcoin is one of the most commonly accepted.

Choose the car you want to buy.

Follow the dealership’s instructions for the exchange.

What’s the advantage of buying a car with Bitcoin?

There are several reasons why some crypto investors prefer to use Bitcoin to buy a car:

Fast Payments. Bitcoin transactions are usually faster than traditional fiat payments. Traditional payments rely on bank transfers or credit/debit cards, which require multiple intermediaries for processing. In contrast, Bitcoin transactions are decentralised and don’t involve intermediaries, allowing for quicker transactions that often take only a few minutes.

Highly Secure Payments. Bitcoin transactions use advanced encryption techniques, making them highly secure. They are recorded on a public ledger called the blockchain, which is virtually impossible to counterfeit or alter. Once a transaction is recorded on the blockchain, it can’t be amended or deleted. This immutability makes all transactions permanent and tamper-proof, hindering anyone from manipulating network records.

Lower Transaction Fees.Bitcoin transactions typically have lower fees than traditional payment methods such as credit cards or wire transfers. This advantage becomes especially significant for international transactions, where traditional remittance fees can be high. Crypto transactions could potentially eliminate 97% of these fees, making large, cross-border transfers more cost-effective.

No Transaction Limits. When purchasing a car with Bitcoin, you don’t need to worry about transaction limits. This is important when making big purchases like cars. Credit card companies and banks may decline a purchase exceeding a certain amount, but cryptocurrencies have no such limitations. This ensures that the transaction proceeds without any delays.

Should you buy a car with Bitcoin?

Whether or not you should buy a car using Bitcoin greatly depends on your comfort level with risk and volatility.

Cryptocurrencies, including Bitcoin, are known for their dramatic price swings.

Take, for example, Bitcoin’s performance in November 2021, when it reached a high of nearly $69,000. At that point, you could have purchased a new Porsche 718 Cayman with just one Bitcoin. Fast forward to the present, Bitcoin’s value is around $17,000, so the same Bitcoin would only be enough to buy an average city car.

The value of cars doesn’t fluctuate as significantly as cryptocurrencies, which makes this kind of transaction risky. However, a workaround for this volatility could be to use stablecoins, which are cryptocurrencies designed to maintain a stable value relative to a specific asset or a pool of assets. A good example is the USDC or USDT, which you can store in a crypto wallet and use for car payments, thus mitigating the risk of your crypto’s value suddenly dropping.

That being said, if you are a firm believer in the future of cryptocurrencies and their potential to revolutionise our financial system, buying a car with Bitcoin could be an exciting way to apply this innovative technology. Plus, there is a certain novelty factor in being able to tell your friends that you bought a car using Bitcoin.

Ultimately, the decision to buy a car with Bitcoin should be based on your personal financial situation, your tolerance for risk, and your belief in the future of cryptocurrencies.

Payment apps may lack protection: A recent warning from the US Consumer Financial Protection Bureau emphasizes that the FDIC might not protect money stored in mobile payment apps. Customers could be concerned about whether their funds are insured, highlighting the risks associated with these platforms.

The US Consumer Financial Protection Bureau (CFPB) has advised Americans to keep their money in a secure, insured bank account rather than in an unprotected app.

The Bureau expressed concern over the growing use of peer-to-peer payment apps, which also handle cryptocurrency transactions, due to the increased risk of losing money if things go wrong.

The public has become more aware of the protection offered by the Federal Deposit Insurance Corporation (FDIC). This comes after the failure of several cryptocurrency platforms and a banking crisis that resulted in the loss of a huge amount of customer money.

Despite this, the CFPB warns that a lot of money is still being held in these payment apps, which aren’t covered by the FDIC.

Payment services don’t offer insurance for your funds

The CFPB says that many peer-to-peer apps like PayPal, Venmo, Cash App, Apple Pay, and Google Pay have features that work much like bank accounts, although Meta Pay doesn’t have that feature.

The companies behind these apps actually like it when you keep your money in their apps because they can then use your money for their own investments (within legal limits), while they hardly ever pay you any interest on the money you store. However, there is a risk involved for these companies, as they could potentially lose money on the investments they make.

The CFPB explains that if your money is in an FDIC-insured account and something goes wrong, whether you’re covered by their insurance is only decided after the fact.

Plus, the insurance only covers the bank’s failure. It doesn’t cover the failure of the payment app, which is usually controlled by state laws and not watched over by the federal government. Most of the time, these state laws are meant for transferring money, not storing it.

So, if you have money in PayPal or Venmo, it could be protected by this pass-through insurance when it’s in their partner banks, but not if they’ve used your money for investments. Also, it might not be clear to you where your money is actually kept.

More and more, these mobile payment services are letting you handle cryptocurrencies. But remember, payment apps may lack protection and cryptocurrencies aren’t insured, even though services like PayPal and Venmo let you keep crypto in your accounts.

In October 2022, the EU published a report to describe the risks of crypto assets investments.

According to the report. “The pseudonymity that prevails in crypto-asset markets makes it virtually impossible to assess the creditworthiness or aggregate exposures of participants.” The paper also talks about the leverage offered by crypto exchanges to individual investors, which can raise up to 125x.

While some jurisdictions try to adopt regulations to protect investors (e.g., MiCA), these regulations often fall short in the face of the ever-expanding crypto industry.

All in all, keeping your crypto investments is a very risky business, and you should be aware of the risks.

Why aren’t crypto insurance policies good enough yet?

Insurance companies still need to improve their crypto insurance plans. Right now, these plans don’t cover everything. To fully protect all your crypto assets, you might have to combine different plans. One might cover the loss of your private key, another might cover errors in smart contracts, and you might need a third in case your wallet company goes under.

What are the risks of investing in cryptocurrencies?

Cryptocurrencies are pretty risky. Their prices can go up and down much more than things like stocks. Future prices could also be impacted by changes in laws, which might even make cryptocurrencies worthless. Plus, cryptocurrencies are always at risk from cyber threats like hacking and theft.

Are cryptocurrencies insured by the FDIC?

No, they’re not. The FDIC insures normal bank accounts up to $250,000, but it doesn’t protect cryptocurrencies at all. If you’re not from the US, you should check your country’s financial authority and see their conditions for insured investments and their limitations.

Can I get insurance for my cryptocurrency investments?

Yes, you can get insurance that offers limited protection against cryptocurrency theft. But these policies often only cover specific situations. They generally don’t protect you against losses due to market changes, hardware damage or loss, sending cryptocurrency to someone else, or problems with the blockchain technology that supports the asset. If you want more comprehensive coverage, you’ll probably need to buy multiple policies.

The next Bitcoin halving will take place in 2024. Is this a ‘buy the dip’ opportunity? With less than one year to the next big crypto event, investors are getting anxious.

Is it time to invest in Bitcoin as the halving approaches? Historical patterns suggest that Bitcoin’s price behaviour tends to follow a distinct cycle aligned with these halving events, which occur every four years.

These cycles, known as “epochs,” typically encompass a significant high and low point in Bitcoin’s value, with these events being roughly four years apart.

Interestingly, in each epoch, the significant low point usually materializes just over a year prior to the next halving. Therefore, long-standing Bitcoin advocates see little evidence to suggest a significant deviation from this pattern in the future.

Ultimately, the Bitcoin halving is just a reminder that the world’s most valuable crypto is designed to become increasingly scarce as time passes by. Even if your crypto investment isn’t in Bitcoin, this even still has a massive effect on the entire market, as Bitcoin represents almost 50% of the market.

What is Bitcoin halving?

Bitcoin is created by powerful computers which solve complicated mathematical puzzles to validate each blockchain block and generate new Bitcoins. Every four years (210,000 blocks, to be more exact), the reward for generating a new block is cut in half. Hence the name Bitcoin halving.

When Bitcoin started, miners got 50 Bitcoins for every block they added. This was a lot, but it helped attract people to the system.

For example, the first halving happened in 2012 when the reward dropped from 50 to 25 Bitcoins. The second halving, in 2016, cut the reward down to 12.5 Bitcoins. The most recent halving in 2020 reduced the reward to just 6.25 Bitcoins.

The next halving is expected to happen in 2024. This halving process will continue until we hit around the year 2140, by which time all 21 million Bitcoins should have been mined.

Why does Bitcoin halving happen?

Imagine the Bitcoin system as a digital gold mine that’s programmed to dig up a new chunk of gold every 10 minutes. As more miners (people with powerful computers) join the hunt, they’re able to dig up gold faster. But to keep things fair and maintain the 10-minute digging goal, the digging process is made harder every couple of weeks. Despite the growth of the Bitcoin network over the past decade, the average digging time has stayed below 10 minutes, around 9.5 minutes, to be exact.

Now, the total amount of Bitcoin that can ever exist is capped at 21 million. When this number is hit, no more Bitcoin can be created. Bitcoin halving is a process that gradually reduces the amount of new Bitcoin that can be mined each time a block is added to the blockchain. This makes Bitcoin scarcer and potentially more valuable over time.

You might think that halving the reward for mining would make people less interested in doing it. But Bitcoin halvings have historically been associated with big jumps in Bitcoin’s price. This keeps miners motivated to mine more, even though they’re getting less Bitcoin each time they mine a block.

So, miners are encouraged to keep digging as long as the price of Bitcoin keeps going up. If the price doesn’t rise and the reward for mining keeps getting smaller, miners might be less interested in mining Bitcoin. This is because it takes a lot of time, computer power, and electricity to mine Bitcoin.

If you want to know more about Bitcoin, check out this Bitcoin hard fork guide, which explains all past forks which affected all BTC holders.

Should I buy Bitcoin?

Investor and entrepreneur Alistair Milne shared his perspective, recommending that those seeking to benefit from Bitcoin should consider purchasing now, as the period preceding the halving might not present as advantageous an entry point. He advised, “Avoid shorting when it’s dark green and ensure you’re fully invested before it turns blue.”

In the earlier part of the month, a well-known yet contentious figure in the Bitcoin industry used the halving narrative to argue that the pricing cycles aren’t a matter of coincidence. PlanB, the anonymous creator of the Stock-to-Flow (S2F) Bitcoin price prediction models, noted that about half of the market participants believe the link between halvings and price is random.

Why is bitcoin S2F/halving not priced in?

Because ~50% thinks the BTC price jumps after last 3 halvings (red) are a coincidence. Halvings are key to S2F, but these critics focus on auto-correlation between halvings and conclude there is no relation between S2F/halvings and… pic.twitter.com/8VaIy6oM5i

PlanB’s comments were framed within the debate over the relevance of the S2F theory to halvings, a theory that has faced considerable criticism due to unmet price predictions from 2021 onwards. However, PlanB also asserts that the current BTC/USD value is low, and the market hasn’t adequately factored in the upcoming halving.

PlanB questioned, “Why is bitcoin S2F/halving not priced in? Because ~50% thinks the BTC price jumps after last 3 halvings (red) are a coincidence.

Why isn’t the Bitcoin S2F/halving reflected in the price? Approximately 50% believe the price spikes following the last three halvings are coincidental,” adding an explanatory chart to his statement. He continued, “Halvings are key to S2F, but these critics focus on auto-correlation between halvings and conclude there is no relation between S2F/halvings and price. I disagree, obviously. 2024 halving will be very interesting!”

What does the Bitcoin halving event mean?

Think about Bitcoin miners like gold miners. They get paid in Bitcoin for their hard work of adding new transactions to the blockchain. But when Bitcoin halving happens, miners earn less for their work. This means fewer new Bitcoins enter circulation, similar to how less gold would be available if miners dug up less gold.

Here’s where the basic rules of supply and demand come in.

When the supply of something goes down, but demand stays the same or even goes up, the price usually goes up.

The halving event also slows down how fast new Bitcoin is made, which helps control inflation. Inflation is like when a dollar can’t buy as much as it used to. But Bitcoin is designed to be the opposite – it’s supposed to become more valuable over time. The halving event helps make this happen.

For instance, Bitcoin’s inflation rate was 50% in 2011, but it dropped to 12% in 2012 after the first halving and 4-5% in 2016 after the second halving. Currently, it sits at around 1.77%. So, after each halving, Bitcoin tends to become more valuable.

However, this process isn’t without its issues. Mining Bitcoin uses a lot of electricity, and miners might struggle to break even if the reward they’re getting is halved but the price of Bitcoin doesn’t go up enough to cover their costs.

Also, because of this, miners will be on the lookout for newer, more efficient technologies that can help them mine more Bitcoin while using less energy.

Besides, Bitcoin’s growing popularity and its acceptance by more businesses and big institutions might also push its price up. More transactions are likely to happen as more people start to use Bitcoin and blockchain technology.

Time to buy Bitcoin?

Bitcoin, the world’s largest cryptocurrency, is currently at a low point, trading around $27,300, after dropping almost 2% recently. This dip came as Binance, a significant cryptocurrency exchange, temporarily stopped Bitcoin withdrawals twice in one day due to technical issues. However, these operations have since resumed, and there are signs that Bitcoin could be gearing up for a recovery.

Despite the recent dip, Bitcoin showed promising resistance last week at $29,000, indicating the potential to climb back to $30,000.

Many Bitcoin investors are hopeful due to anticipated pauses in U.S. interest rate hikes and shifting trust from traditional finance to decentralized finance (DeFi). Combined with the upcoming Bitcoin halving event in 2024, which typically brings a surge in Bitcoin’s value, some experts predict Bitcoin could reach $35,000.

Still, it’s important to remember that Bitcoin is trading 50% lower than its all-time high of $69,000 in November 2021, and the journey to recovery may be lengthy. Also, external factors such as regulatory changes in countries like India could influence the market.

So, is it time to buy Bitcoin? It seems like a potentially advantageous time, given the low price and positive future prospects. But, as always with cryptocurrencies, it’s crucial to be vigilant and cautious due to their volatile nature. It’s best to stay informed about the current macroeconomic conditions and regulatory developments.