The biggest Russian bank has announced that it will create its own blockchain and it will incorporate it with Ethereum to expand into DeFi and Web3 markets. The Russian government plans to create its own crypto exchange.

Sber (formerly known as Sberbank) officially announced new opportunities on its proprietary blockchain platform. This includes compatibility with smart contracts and applications on Ethereum. The bank stated that this would enable developers to transfer smart contracts and entire projects between Sber’s blockchain and other public blockchain networks.

Sber’s latest additions include integration with MetaMask, a major software cryptocurrency wallet that interacts with the Ethereum blockchain. According to the announcement, users can now make transactions with tokens and smart contracts placed on Sber’s blockchain platform.

Alexander Nam, head of the blockchain lab, said that “Sber Blockchain Lab collaborates closely with external developers. I am happy that our community will now be able to run DeFi apps on Sber’s infrastructure.” The new integrated features will allow Sber to bring together developers, financial institutions, and corporations to explore the practical applications of blockchain, Web3 and decentralized finance (DeFi).

Sberbank, as previously reported, has been actively developing blockchain products in recent years, submitting an application to the Bank of Russia in order to launch a platform on blockchain for its “Sbercoin” stablecoin in 2021. Sber finally announced its first digital currency transaction after receiving approval from the central bank in spring 2022. The government of Russia is Sber’s majority shareholder, owning 50% + 1 share.

Sber’s announcement was made shortly after Russian President Vladimir Putin demanded an open, blockchain-based settlement network. He condemned the monopoly of global financial payments systems and expressed confidence that digital currencies-based technology would allow for greater independence from banks. Putin’s government, however, does not allow citizens to use crypto for payment. In early 2020, it imposed a blanket ban against payments using Bitcoin.

Russian lawmakers discussed possible legal amendments to enable the government to launch a national cryptocurrency exchange. The Bank of Russia and the Ministry of Finance support this effort, which is known for being a source of much disagreement in regulating the local crypto market.

Russia wants to launch its own crypto exchange

Russian lawmakers are currently working on amendments that would allow for the launch of a national cryptocurrency exchange. The effort is supported by both the Ministry of Finance as well as the Central Bank of Russia.

Local media reported that members of Russia’s lower chamber, the Duma, have been meeting with market participants to discuss amendments to its existing cryptocurrency legislation “On digital financial assets.” First, the amendments that would establish a legal framework to allow for a national currency exchange will be presented to the central bank.

Sergey Altuhov was a member of the Committee of Economic Policy of Duma, and he highlighted the fiscal sensibility of these measures:

“It makes no sense to deny the existence of cryptocurrencies, the problem is they circulate in a large stream outside of state regulation. These are billions of tax rubles of lost tax revenues to the federal budget.”

In June 2022, Anatoly Aksakov (head of Duma’s Committee on Financial Market), suggested a Russian national crypto exchange could be launched under the Moscow Exchange, as this is seen as a “respectable organization with a long tradition.” In September, the Moscow Exchange created a bill on behalf of the central bank to allow the trading of digital financial assets.

A bill that would allow cryptocurrency mining and the sale of cryptocurrency mined was presented to Duma earlier this month. Although the bill will create a Russian platform to sell cryptocurrency, local miners can also use foreign platforms. The Russian regulations and currency controls would not apply to transactions in this case. However, they would need to be reported to Russia’s tax service.

Belgia’s financial regulator has confirmed that Bitcoin, Ether, and other cryptocurrencies issued only by computer code are not securities.

However, this contradicts the views of Gary Gensler, Chairman of the U.S. Securities Exchange Commission, who has a different set of conditions to determine which crypto assets can be deemed a security.

Belgium releases a report about the classification of crypto

This explanation was provided by Belgium’s Financial Services and Markets Authority (FSMA) in a report released on November 22, 2022. This clarification was necessary due to the increased demand for information about how Belgium’s financial laws and regulations related to digital assets.

Although not legally binding according to Belgian or European Union law, the FSMA stated that cryptocurrencies would be classified as security if issued by an individual or organization:

The report states as follows:

“If there is no issuer, as in cases where instruments are created by a computer code and this is not done in execution of an agreement between issuer and investor (for example, Bitcoin or Ether), then in principle the Prospectus Regulation, the Prospectus Law and the MiFID rules of conduct do not apply.”

Belgian regulators noted that cryptocurrencies, even if they aren’t classified as securities, may still be subjected to other regulations if used by a company as a medium for exchange.

“Nevertheless, if the instruments have a payment or exchange function, other regulations may apply to the instruments or the persons who provide certain services relating to those instruments.”

Belgians regulators classify all digital coins, not just blockchain-based crypto

FSMA noted that the stepwise plan was neutral to technology, suggesting that it doesn’t matter whether digital assets are created and facilitated through a blockchain or other traditional methods.

In July 2022, the FSMA drafted the first report. This was to answer frequently asked questions from Belgian-based offerers and issuers of digital assets.

FSMA stated that the stepwise approach would be used as a guideline for the European Parliament’s Markets in Crypto Assets Regulations (MiCA), which will take effect at the beginning of 2024.

The clear guidelines of Belgium are contrary to the U.S. Securities Exchange Commission’s (SEC) “regulation by enforcement” approach. This is currently competing for control over digital asset regulations together with the U.S. Commodity Futures Trading Commission.

Gary Gensler, the chairman of SEC, has always considered BTC a commodity. However, he recently suggested that post-Merge Ether or other staked coins may be considered a security under the Howey test.

Belgium isn’t a big adopter of digital assets yet. A recent study by blockchain data platform Chainalysis ranked Belgium 94th on its Global Crypto Adoption Index.

But Bitcoin seems to have a lot of public support in Belgium.

A Belgian politician received his salary in crypto

Christophe De Beukelaer was the first European politician to convert his salary to Bitcoin. He started doing this at the beginning of 2022. He hopes to increase awareness about Bitcoin, and other alternative monetary models, to encourage financial literacy and get people talking.

De Beukelaer was first introduced to Bitcoin and blockchain in 2017. He foresees a future where Bitcoin and other cryptocurrencies will be an alternative to traditional financial systems.

“The political people don’t have the time to travel. They are busy running the daily administrations of cities and countries. But they don’t stop to ask, “OK, what’s the next step?” What are the major changes that will take place in the next 10, 20, or 50 years? That’s what you do.

The Brussels politician acknowledged that there is a lack of awareness about cryptocurrency and Bitcoin. He also said that if Europe doesn’t get its hands dirty in space, then “Asia (or] the U.S.A. will decide everything.”

He believes that being paid in Bitcoin can raise awareness and add credibility to the space.

Binance and other big centralized exchanges plan to use the Proof of Reserves as an auditing technique to reassure their customers of the safety of their funds.

As trust in its accounting of billions in assets disappeared, crypto exchange FTX went bankrupt at the beginning of November 2022.

Some critics have slammed the existence of centralized exchanges, such as FTX. Its CEO, Sam Bankman-Fried, posted many messages on Twitter trying to convince his customers that he had made a terrible but honest mistake that he would try to repair. However, CEX customers are now all wondering just how safe their assets are on any of these exchanges. And the truth is that without total transparency from the exchanges, the FTX collapse could happen again at any given time.

The controversy has brought back the debate about a possible solution. It is called proof of reserves, or PoR. This method shows, without any doubt or ambiguity, how many tokens are on each exchange that uses the technique. Proof of reserves, if in place at FTX, could have, in theory, stopped customers’ money from being moved to places it shouldn’t. In this case, the assets wouldn’t have moved to Bankman-Fried trading firm Alameda Research.

Binance, the largest cryptocurrency exchange in the world by volume, has shared its wallet accounts and said it would conduct a proof of reserves snapshot within the next few weeks. Other CEXs that made similar statements include Gate.io, KuCoin, Poloniex, Bitget, Huobi, OKX, Deribit and Bybit.

What is proof of reserves?

Proof of reserves is an audit technique that confirms assets in custody. It is used by stablecoin issuers Paxos to show they have enough assets backing their tokens. Exchanges like BitMEX use the technique to prove that customer deposits correspond with assets in custody.

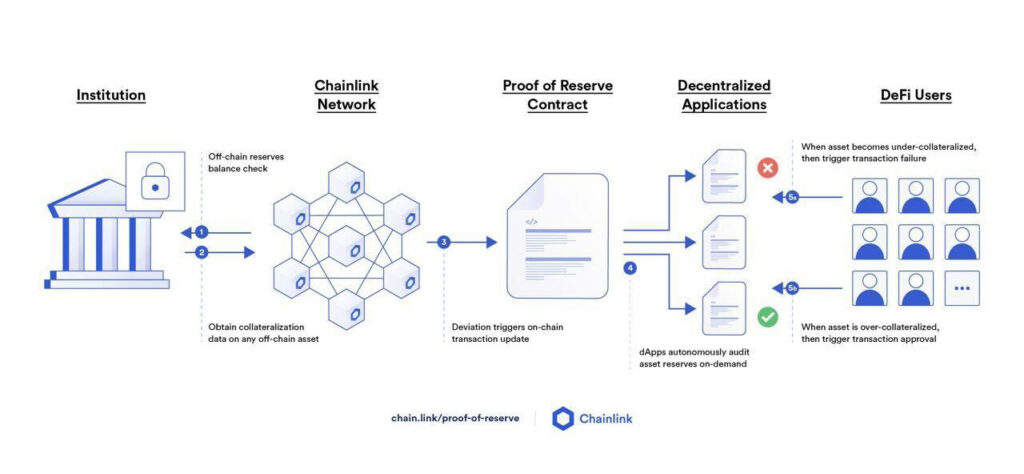

Sergey Nazarov, the co-founder of Chainlinks Labs, stated that the use of this auditing solution could have made it possible to avoid all of this: “It would have been quite a solvable problem if there had been more transparency in the balance sheet.” Chainlink offers the proof of reserves (PoR) auditing mechanism as a product. Their PoR solution already powers multiple stablecoins and gold coins.

How does proof of reserves work?

An entity can prove its assets reserves in a variety of ways. These include traditional third-party audits that are performed by companies such as Armanino, to Merkle tree proofs (cryptographic verification using data structures called Merkle branches).

There are also methods that blockchain analytics companies employ. Chainlink is an example of a company that separates proof-of-reserve implementation into two categories: on-chain and off-chain.

An off-chain alternative is a third-party provider, such as Chainlink, that receives API access (application programming interface) from an exchange. This allows the auditor or custodian to verify the exchange’s holdings.

Off-chain proof of reserves (Chainlink)

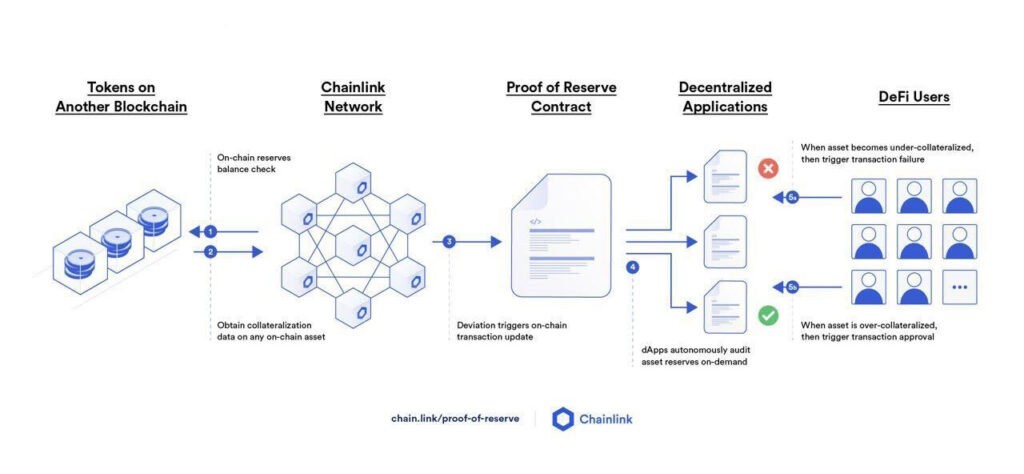

On-chain routing is a proof of-reserves smart contract on one network (usually Ethereum). It receives data feeds from Chainlink’s Oracle network (on a block-by-block basis) about a provider’s on-chain wallet balances in another network (e.g., Bitcoin). This empowers users and allows them to check whether the company or the exchange actually has the assets they claim to have.

On-chain proof of reserves (Chainlink)

Should proof of reserves be used?

Investment brokers that offer services to retail customers are already producing regular reports to show the client’s assets and liabilities. But this is done because of the harsher regulations that are already in place for them. For the most part, cryptocurrency exchanges remain unregulated financial services, and customers have nobody to lean on when it comes to a lack of liquidity or bankruptcy.

A first step may be self-regulating services that may regain the trust of customers. Authorities might also be willing to adapt their regulations to the crypto industry when existing exchanges collaborate.

Over the last few years, many exchanges have collapsed, causing crypto investors to lose a lot of money. While many never got their funds back, this also caused existing services to practice much better security and transparency.

The Bahamas-based company, FTX.com crypto exchange, announced Friday (November 11, 2022) that the crypto exchange had filed for bankruptcy protection in the United States.

Sam Bankman-Fried, the founder and CEO of FTX, has also resigned but said he would assist with an orderly transition. John Ray III will be the new CEO. Ray seems to be the same person who oversaw Enron Corporation’s bankruptcy.

According to Ray, FTX employees will feel the pressure in the near future: “In the short-term, we have some long and hard work ahead.” He also described the bankruptcy filing as “the beginning of a journey forward.”

Respective bankruptcy filings stated that FTX US (and Alameda Research) had between $10 billion to $50 billion in liabilities, as well as a similar range of assets. They also estimated that the funds would be available for distribution to unsecured creditors.

Why did FTX collapse?

This is the context that will help you understand this story. This includes the unexpected crisis of confidence caused by revelations about Sam Bankman Fried’s accounting practices, the shock at Bankman Fried’s reputation as a golden boy, and the complex role played by Binance and Changpeng Zhao, its founder in the crisis.

Let’s start with the background story of Sam Bankman Fried and his other company, Alameda Research, which played a major role in this series of unfortunate events.

At the beginning of November 2022, Alameda was holding around $5.8 billion out of its $14.6 billion assets in FTT, FTX’s exchange token.

Based on leaked documents, this finding was shocking because of the close relationship between Alameda & FTX. Both were established by Bankman-Fried. There has been considerable anxiety about the nature and extent of their fraternal relationships. This raises questions about the open-market, real-world value of FTT tokens that are held in reserve by affiliated entities.

Negative speculation about financial institutions can become a self-fulfilling prophecy. It can trigger withdrawals from a feeling of uncertainty and lead to liquidity problems.

But simple facts can be enough to cause a bank run. FTX token and Alameda have a history of close ties. This led to a mass exodus on November 8th. According to internal messages, Reuters saw $6 Billion in withdrawals on the exchange before things turned sour. What’s more, at the time, FTX exchange has an internal balance of only 1 BTC. Meanwhile, the exchange’s bitcoin balance reached 36 BTC, but this is still minute compared to the half a million BTC held by Binance or Coinbase.

Bankman-Fried’s team began to search for acquisition partners in a rush and approached a range of potential partners just before Binance was involved.

It is still unclear why FTX would want to be rescued even if there was such a rush for exits. Users were promised that the exchange would not speculate on cryptocurrencies in their accounts. If that policy had been followed, then there shouldn’t have been a pause in withdrawals or a balance sheet gap to fill. Coinmetrics analyst Lucas Nuzzi has provided evidence that FTX transferred funds in September to Alameda, possibly as a loan to cover Alameda’s losses.

Alameda’s vast FTT-linked assets seemed to confirm fears about the stability of Bankman-Fried. The token’s market value decreased by 90% between November 7 and November 10.

FTX announced that it had temporarily suspended all crypto withdrawals late in the evening on November 8, following the announcement of a tentative agreement with Binance.

According to a press release, the FTX.com entity, as well as FTX USA, Alameda Research, and “approximately 13 additional affiliated companies,” has filed for Chapter 11 bankruptcy proceedings. Chapter 11 bankruptcy proceedings can be filed by companies that hope or expect to be able to restructure their operations. This is in contrast to Chapter 7 bankruptcy which only liquidates assets.

Companies that file for Chapter 11 bankruptcy can continue to operate their daily operations.

Bankman-Fried posted a tweet after the bankruptcy and apologized. He said, “Hopefully things can find a way to recover. Hopefully this can bring some amount of transparency, trust, and governance to them.”

5) I'm piecing together all of the details, but I was shocked to see things unravel the way they did earlier this week.

I will, soon, write up a more complete post on the play by play, but I want to make sure that I get it right when I do.

The release stated that FTX Digital Marketplaces, FTX Australia and FTX Express Payment are not included.

Ray stated that the FTX Group’s valuable assets can only be efficiently managed in an organized, collaborative process. “I want to assure every customer, employee, creditor, contract partner, stockholder, investor and other stakeholder that this effort will be conducted with diligence, thoroughness, and transparency.”

He said that events have been “fast-moving,” and the new team has just begun.

The FTX bankruptcy sent shockwaves on the crypto market

Bitcoin immediately plunged to $1,000 after the bankruptcy news and fell to $16,500 in just minutes.

Bankman-Fried reported FTX’s “liquidity” issues earlier in the week.

Firstly, it was stated Binance had offered to purchase the company. Then, Justin Sun of Tron announced a deal to support TRX-based tokens. FTX halted withdrawals, but FTX US withdrawals remained unchanged. FTX announced that certain jurisdictions had initiated partial withdrawals.

According to a bankruptcy filing, the complete list of companies includes Alameda, various local holdings, and Blockfolio. Quoine and over a dozen FTX entities are also included.

“I was shocked to see that FTX listed BTC Africa S.A. and other AZA Finance entities today,” stated Elizabeth Rossiello in a statement. She is the CEO and founder of BitPesa as well as AZA Finance. To be clear, AZA Finance entities aren’t affected by the FTX bankruptcy. We are taking steps to rectify the erroneous court files,” she said, adding that “in its disorganized haste, FTX erroneously listed their entities in bankruptcy filings.” Here’s the AZA Finance statement regarding the FTX bankruptcy statement.

The crypto market is interconnected

The collapse of the Three Arrows Capital hedge fund has shown that crypto is extremely interconnected. Evidence suggests that Alameda’s financial problems began after it lost half a million dollars to Voyager Digital. Voyager Digital was later purchased by SBF, as it had been insolvent after Terra collapsed.

Unfortunately, as more people are attracted to the crypto and blockchain space, they are drawn by big marketing campaigns to these massive centralized exchanges. the industry has re-created the centralized financial system, including “bank runs” and all. Instead of interfacing directly with peers and blockchains, people now store their money on centralized exchanges. Instead of trusting financial protocols that are not reliable, they place their faith in Wall Street-respected megalomaniacs.

The Securities and Exchange Commission (SEC) also took notice of the FTX and has ongoing investigations. Gary Gensler, Chairman of the SEC, almost gloated about this moment, noting the “toxic mixture” at FTX. He repeated the familiar line that cryptos are securities and should be under his agency’s supervision. Gensler also noted that the industry had been “significantly non-compliant” and that exchanges should “come into and talk to us.”

It is notable that FTX.US, the independent wing of SBF’s trading empire, seems to be solvent. It could all go down tomorrow, but it seems that SBF wouldn’t have done the same shenanigans using FTX.US user funds as he did with the parent company, no matter how tired he was.

Yet, it is important to mention the role that U.S. crypto regulation played in the FTX downfall. Coinbase’s CEO Brian Armstrong argued on Twitter that the stringent-yet-unclear regulatory landscape pushed people like Terra’s Do Kwon and Bankman-Fried overseas, where oversight is lax, and taxes go unpaid. According to Gary Gensler, 95% of crypto trading occurs outside the U.S.

Crypto may fail because it is not regulated

Cryptocurrency was created to allow people to be their own bank by allowing them to be independent and responsible for their finances. Instead, Three U.S. regulators – the Commodity Futures Trading Commission, the Securities and Exchange Commission, and the Department of Justice – have intensified their investigations into FTX. Some of these investigations had been ongoing for months.

In an interview with CNBC, Gensler may be correct in stating that there are rules that could protect crypto investors. Armstrong is protecting his interests here, while Sen. Elizabeth Warren (D.Mass.) and others are calling for tighter regulation. Gensler and Armstrong are calling for tighter regulation on U.S. exchanges. While more explicit regulations are essential, they must be followed. Because crypto is not a country-specific currency, regulators who make it too burdensome will only be able to create the next Terra-based in Singapore or Bahamas-based FTX. Armstrong said that it was absurd to punish U.S. companies like this.

The largest metaverses have lower daily active users than other smaller and independent blockchain games. Top metaverses are trying to make things appear better than they actually are.

The metaverse received a lot of attention in 2021 when the concept of non-fungible tokens (NFTs) became the most controversial investment opportunity. Recently, people started to wonder what is the exact number of daily active users (DAUs) on the most popular metaverses. Decentraland and The Sandbox tried to explain how they calculate the users, but numbers don’t lie.

According to DappRadar, the two most famous metaverses are lacking users. And people have started to notice that.

Even if the numbers are a rough estimate, the DAU controversy raises serious concerns about online user behavior. And it suggests that online users are not quite ready to jump into the metaverse and exist there. While this wouldn’t be an issue with any random online game, having a metaverse that is literally worth over $1 billion in crypto is an essential aspect of the blockchain industry.

Decentraland is an expensive but lonely metaverse

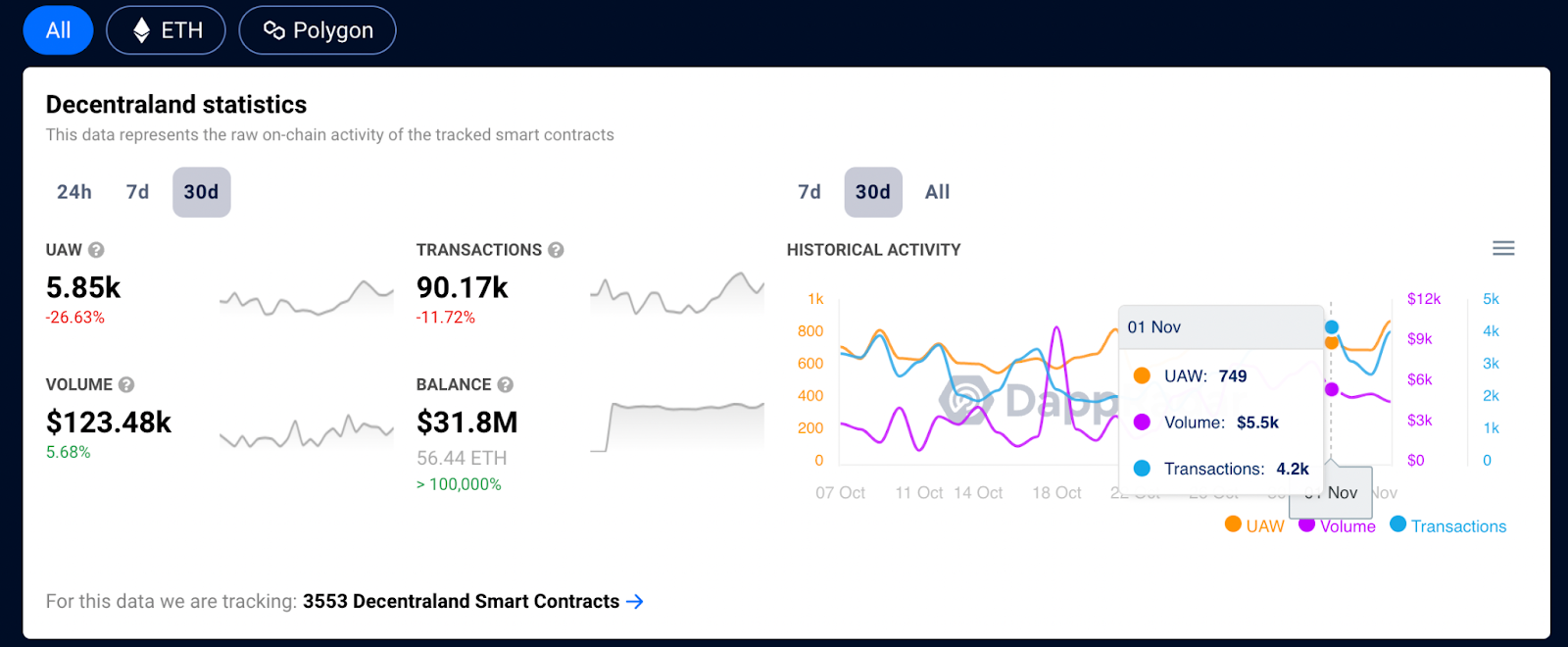

DappRadar is a data blockchain aggregator and tool that analyzes DApps on the main blockchains. Recently, DappRadar revealed that the Ethereum-based virtual universe Decentraland had 38 active users in the last 24 hours, while its competitor Sandbox had 522 active users in the same period.

The DappRadar tool has no way to determine the active users of any metaverse, but it can count the unique wallet address that interacts with the platform’s smart contracts. An example of active use is logging onto The Sandbox or Decentraland to make a purchase using SAND or MANA (each platform’s native utility token).

DappRadar doesn’t include people who log in to interact with others on metaverse platforms or drop by for events, such as concerts. This could also mean that there are fewer transactions on these platforms, from buying or selling NFTs than people who visit them.

According to DappRadar, an estimated 749 were active on November 1st, and this number never goes above 880 in the entire month of October. The tool counts around 5,850 wallet addresses that have interacted with the DApps’ smart contracts in the entire month of October 2022. While this number doesn’t tell us exactly the number of users, it is considered a way to track the “active users” per day on Decentraland.

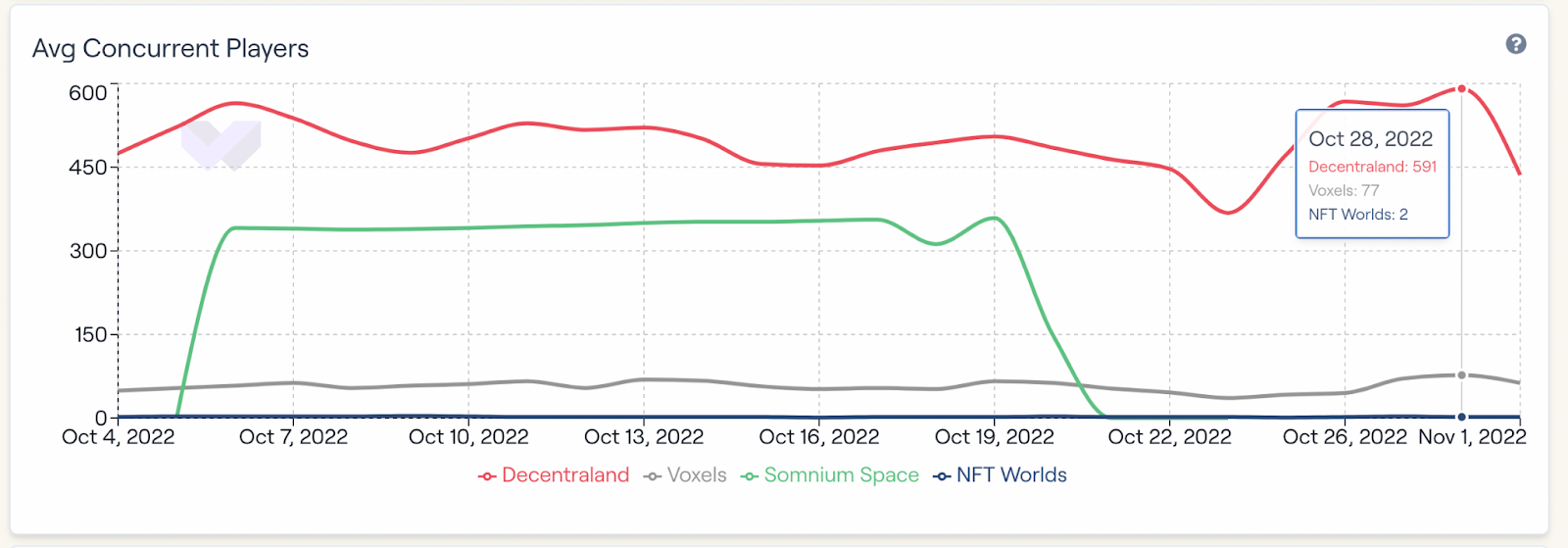

WeMeta, a metaverse analytics tool, provides the average concurrent players, which can only give you the number of users on Decentraland servers at a specific time. This tool only counts around 600 daily users.

In contrast, DCL Metrics, an analytics platform built by the Decentraland community, offers an estimate of almost 8,000 of the number of unique users.

As you can see, there isn’t a sure way to determine how many users are in the Decentraland metaverse every day, and the platform said that they are not counting them.

According to Decentraland, they had over 56,000 monthly active users in September and about 1,000 users interacting with smart contracts.

Let's have a look at some of September's data:

56,697 MAU 1,074 Users interacting with smart contracts 1,732 minted Emotes 6,315 sold Wearables 300 Creators received royalties 161 created Community Events 148 DAO Proposals

Take into account that Decentraland (MANA) is valued at $1.18 billion, according to CoinMarketCap.

The Sandbox is also struggling to attract users

Let’s look at Decentraland’s competing metaverse, The Sandbox, which has a token also evaluated at over $1.23 billion, according to CoinMarketCap.

According to DappRadar, The Sandbox has about 2,160 UAW (Unique Address Wallets) active in a 24h timeframe that interact with the DApp smart contracts.

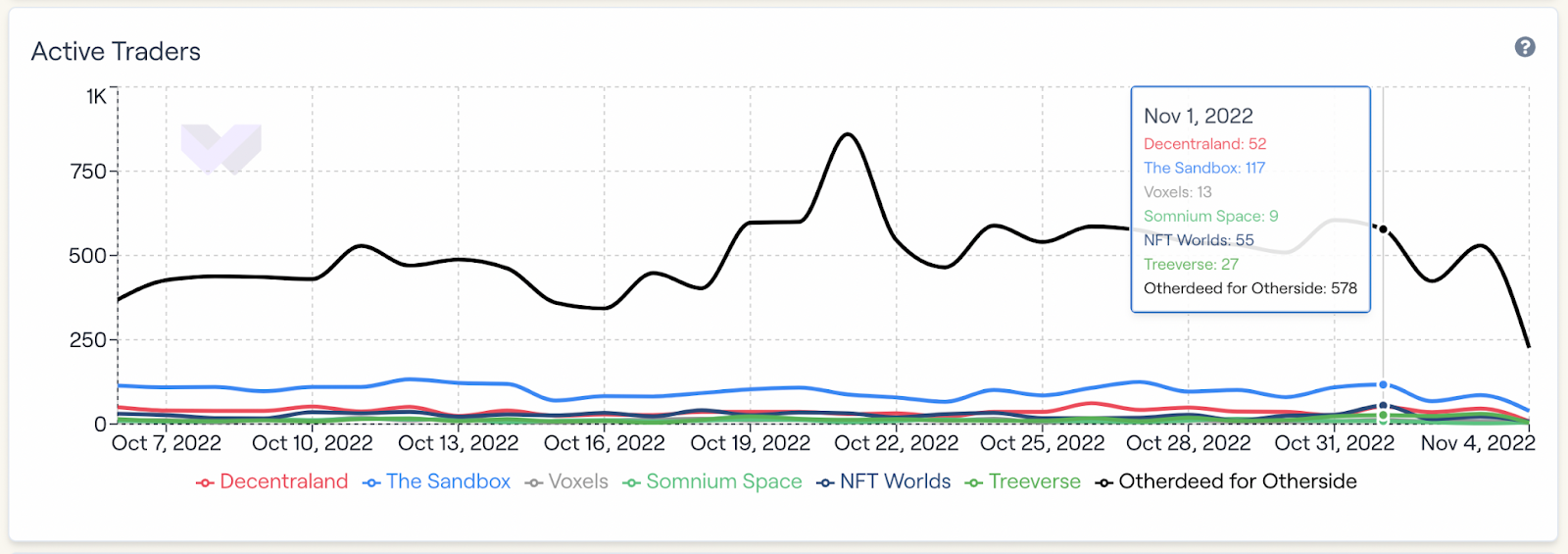

Again, there is no tool to tell us the daily active users in The Sandbox, but WeMeta gives us a hint of the active traders in the SAND metaverse. As of November 1st, 2022, there were 117 traders in The Sandbox, while only 52 traders in Decentraland.

The Sandbox also tweeted some of their monthly stats, which say that the metaverse has over 39,000 daily users.

Independent blockchain game is more successful than these $1 billion metaverses

Aside from these heavily marketed metaverses, other blockchain games are indeed free to play and deliver an enjoyable experience to passionate gamers. One such example is FootballCoin, a fantasy football manager built entirely on their own blockchain.

The game allows anyone to create an account and play the game for free, offering daily rewards.

Without any dependency on any other chain, FootballCoin has around 1,000 active players. While this is not a metaverse, the game’s community is highly engaged on other communication platforms, such as Telegram and Discord, where they negotiate NFT trades and create joint competitions.

According to CoinMarketCap, FootballCoin has a market cap of about $2,8 million and has an ascending trend.

As with anything in the crypto space, people choose to invest their time into projects that offer value and potential future profits.

Terra co-founder Do Kwon and others are accused of making fraudulent claims regarding UST, either knowing they were false and unverifiable or recklessly not caring if they were true or false.

Do Kwon is the co-founder of Terraform Labs. In May 2022, the Terra blockchain collapsed in only a matter of hours as its algorithmic stablecoin was strategically exploited. This left Terra investors liquidated, and many lost their life savings. After many months of controversy and accusations against authorities for not doing anything, the case is going to court.

Do Kwon may face legal action in South Korea and the United States. Do Kwon will also be sued in Singapore, along with the Luna Foundation Guard (LFG) and Terra’s other founding member, Nicholas Platias.

The lawsuit against Kwon Terra’s co-founder Do Kwon

On September 23rd, 359 people filed a lawsuit in Singapore’s highest court. According to their accusations, Kwon, Platias, and Terra made fraudulent claims. After the collapse of Terra’s stablecoin TerraUSD (UST), Do Kwon stated that they are creating a Terra hard fork, and that the old stablecoin is now TerraUSD Classic (USTC). What we all agree on is that Terra’s U.S. dollar peg could not be maintained due to its unstable design, which is basically a flaw of algorithmic stables.

The plaintiffs are asking for compensation for $57 million in “loss and damages” based on the UST tokens that they bought, held, or sold during the May market crash. They also ask for an order to cover “aggravated damages.”

The lawsuit claims that Terra and other parties related to it knew or should have known that the claimants wanted to purchase and hold stablecoins that would not be subject to volatility, and that could earn passive returns. The document is also indicating that Do Kwon’s experience in an earlier project (Basis Cash) would have made it impossible for him not to be aware of the structural weakness of algorithmic stablecoins.

The main accusation is that Do Kwon and the other defendants made the fraudulent representations either knowing they were false and untrue or recklessly not caring if they were true or false.

Terraform Labs spokesperson for Terraform Labs stated that both LFG and the company are trying to protect themselves from the claims:

“There is a fundamental difference between a public market event and fraud. Terraform Labs and the Luna Foundation Guard committed no wrongdoing — the risks were publicly known and discussed, and the underlying code was open-sourced.”

What happened to Do Kwon after Terra’s collapse?

Since the May collapse of Terra’s blockchain ecosystem, Kwon has been subject to numerous legal actions and threats. In September, South Korean authorities issued an arrest warrant for Terra co-founder, but it was later dismissed. Interpol also added Kwon to its Red Notice List, asking law enforcement to locate him and possibly detain him.

Since Do Kwon is a Korean citizen, the South Korean foreign ministry demanded that the Terra co-founder surrender his passport. Otherwise, it would be canceled. On Oct. 6, the Ministry of Foreign Affairs in South Korea issued an order to Do Kwon, Terraform Labs CEO, to surrender his passport.

Within 14 days of receiving the order, the fugitive cofounder must turn over his Korean passport. Refusal to comply with the order will result in his passport being canceled, and any future requests to reissue it will be rejected.

Another local report stated that six Terraform Labs employees, including Kwon, received a passport return order.

Kwon was active on social networks during the controversy. He stated in September that he was making “zero effort to hide” his location despite not disclosing it. In response to the lawsuit, it stated that Kwon was “doing an awful job of acting innocent for someone who is innocent”. Many others speculated that Kwon had undergone plastic surgery to hide his appearance.

Kwon was listed as residing in Singapore by the Sept. 23 lawsuit, although some reports suggest that he could have fled the country. His current location is unknown.

Terraform Labs claimed the case against Kwon was highly politicized. According to a spokesperson for the company, prosecutors agreed to expand the definition of security following the collapse of associated cryptocurrencies.

Terra investors are also on the lookout for Kwon

A Discord group of over 4,400 people has created the UST Restitution Group (URG). This Discord group has been trying to find Terra co-founder Do Kwon.

The group uses the internet to find clues and share them with one another to locate Kwon. This may be done out of frustration at not receiving any results from law enforcement agencies.

Some members suggested he could live in Russia, Dubai, Azerbaijan, or even on a yacht.

They continue to work despite South Korean authorities taking significant steps to bring Kwon justice.

URG was initially formed on May 16th as a chatroom for Terra ecosystem investors. Some members are claimants in lawsuits to recover funds from TerraUSD Classic (USTC).