While Ethereum staking is on the rise, it brings with it the challenge of increased centralization. Even Ethereum co-founder Vitalik Buterin acknowledges this as a core issue, suggesting that a comprehensive solution may be decades away.

The growth in Ethereum staking has surged since the Merge update.

But this has led to two issues: the network becoming more centralized and people earning less from staking.

The team at JPMorgan, headed by top executive Nikolaos Panigirtzoglou, cautioned investors about these rising concerns related to Ethereum’s increasing centralization.

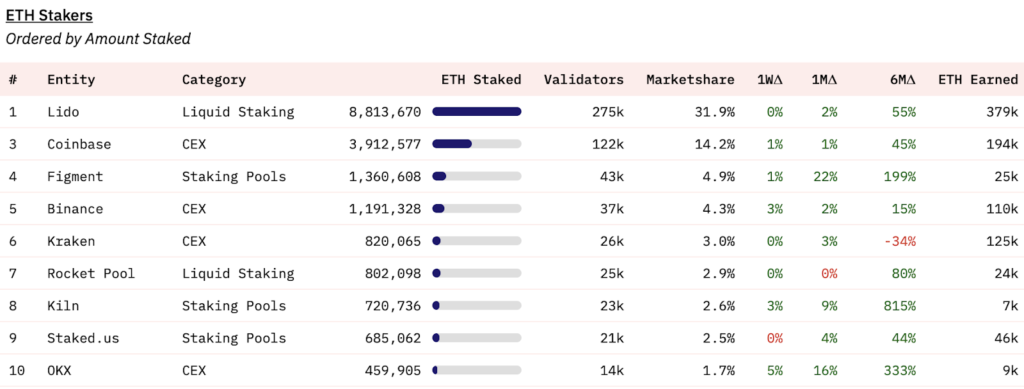

The leading five easy-staying services—Lido, Coinbase, Figment, Binance, and Kraken—hold more than half of all staked Ethereum.

According to Dune Analytics, over 31% of all ETH staked belong to the Lido pool.

While people in the crypto world have viewed Lido as a better option than centralized services like Coinbase or Binance, the reality is different.

Even decentralized platforms like Lido still have a lot of control concentrated in a few hands. For example, one Lido node operator alone manages over 7,000 sets of validators, holding 230,000 Ether.

This concentration of power occurs because Lido’s decision-making is controlled by a small number of wallet addresses in their decentralized organization, known as a DAO.

While there was a general market proposal to limit each staking service to no more than 22%, Lido’s DAO voted against it in June 2023. In general, a DAO is a self-governing platform, but in this case, its decision to not limit its Ether staking is making the entire Ethereum ecosystem more centralized and, thus, more vulnerable.

Having too much control in one place poses a risk to the Ethereum network. A small group of major stakeholders or node operators could become a weak point in the system, or even collaborate to gain unfair advantages.

In addition to concerns about centralization, the Ethereum network has also seen staking yields go down since the big updates like the Merge and Shanghai.

The average block rewards have dropped from 4.3% to 3.5%, and overall staking yields have gone from 7.3% to around 5.5%.

It’s not just JPMorgan ringing the alarm bells about Ethereum’s growing centralization after the Merge, which was launched on September 15, 2022. This update is viewed as a stumbling block to Ethereum’s goal of being fully decentralized, and it has also led to reduced earnings from staking.

Even Ethereum’s co-founder, Vitalik Buterin, acknowledges the issue. In September 2023, he admitted that tackling the problem of node centralization in Ethereum is a big challenge, and finding an ideal solution could take up to two more decades.

Simplify node operations on Ethereum

Ethereum co-founder Vitalik Buterin says that making it simpler and less expensive to operate nodes is crucial for addressing the Ethereum network’s centralization issue.

Right now, most of the nearly 6,000 active Ethereum nodes are hosted by centralized services. The top service used it Amazon Web Services, posing a vulnerability for the network.

While speaking at Korea Blockchain Week, Buterin identified six critical challenges to overcome to ensure Ethereum stays decentralized over time.

One major aspect is making it technically easier for people to operate nodes. “Statelessness is a key technology to make this possible,” he added.

As of now, running a node requires hundreds of gigabytes of data storage.

With stateless clients, however, you could operate a node without needing almost any storage space at all. This statelessness means eliminating the need for centralized services to verify network activities.

According to the Ethereum Foundation, true decentralization can only happen when running an Ethereum node becomes accessible and affordable.

Buterin emphasized that statelessness is a significant part of Ethereum’s future plans. Major progress towards this goal is expected in upcoming phases called “The Verge” and “The Purge.”

He mentioned that the long-term vision is to have fully verified Ethereum nodes that are so streamlined you could literally run one on your phone.

Buenos Aires plans to issue blockchain-based identity documents, including birth and marriage certificates, while Brazil aims to make its new blockchain-powered national ID program available across the country. Both initiatives signify a major leap in government services and personal data security.

More than 214 million people in Brazil are about to start using blockchain technology for their digital IDs, according to a recent announcement by the government. The states of Rio de Janeiro, Goiás, and Paraná will be the first to start rolling out these blockchain-based identification documents.

They’re using a special, secure system created by Serpro, Brazil’s national data service. The plan is to have this technology available across the entire country by November 6, 2023.

Alexandre Amorim, the head of Serpro, explained that blockchain was chosen for this project because it’s a secure and decentralised way to manage digital IDs.

Blockchain technology is key in making personal data more secure and in reducing fraud, creating a safer digital environment for people in Brazil.

The use of the b-Cadastros blockchain platform improves the safety and trustworthiness of the National Identity Card project.

According to the government, this project is important for tackling organised crime and encouraging different parts of the government to collaborate. It also makes it easier for people to get government services and helps simplify record-keeping.

In recent years, Brazil has been trying to standardise the way IDs are issued across its nearly 30 states. This new technology will help safely share data between the Federal Revenue Agency and other government departments, as stated in the announcement.

Emissão da Carteira de Identidade Nacional (CIN) conta agora com a segurança do Blockchain. Saiba o que muda no documento e confira todos os detalhes que tornam a nova carteira de identidade dos brasileiros mais segura do que nunca!https://t.co/G2MigNkG1J

Another big change happening in the country is the introduction of a new digital currency by the central bank.

The government recently shared more details about this project in August and has renamed the digital currency to “Drex.”

Past reports suggest that the central bank aims to make it easier for businesses to get funding through a special system linked to Drex. A local developer found that the code for Drex allows a central body to either freeze money or lower account balances.

Notably, Buenos Aires in Argentina has announced a similar plan that lets people get their identity documents through a digital wallet.

Blockchain-based in Buenos Aires, Argentina

Buenos Aires, Argentina’s capital, is also taking a big step to include blockchain technology in its administrative processes.

Starting in October, people living in the city will be able to get their identification documents through a digital wallet, as revealed in a September 28 announcement.

Initially, you’ll be able to get documents like birth and marriage certificates, proof of income, and school records on this blockchain system. The plan also includes adding health records and payment information down the line.

The city aims to have a detailed plan for expanding this blockchain service throughout the country by the end of 2023.

The technology backbone of this project comes from QuarkID, which is a digital identity system created by the Web3 company Extrimian.

QuarkID wallets use zkSync Era, a special feature built on the Ethereum network that helps it run more efficiently. This feature uses something called zero-knowledge rollups, which lets one person show another that something is true without having to share any detailed information about what that ‘something’ is.

¡Hola Buenos Aires! Welcome to the ZK Nation 🇦🇷

Buenos Aires is teaming up with @Quark_ID to issue digital identification services to millions of citizens in the city, with zkSync Era serving as the anchor blockchain for the program.

“This marks a huge leap forward in making government services in Latin America safer and more efficient,” said Guillermo Villanueva, the CEO of Extrimian.

The information in these digital wallets will be controlled by the individual, meaning people can decide how and when to share their credentials, whether it’s with the government, businesses, or other people. zkSync Era will serve as the foundation for QuarkID, making sure everyone’s credentials are accurate and secure.

Diego Fernandez, who leads innovation for Buenos Aires, added, “This makes Buenos Aires the first city in Latin America, and among the first globally, to adopt and champion this new technology. We’re setting an example for how other countries in the region can use blockchain technology for the good of their citizens.”

Officials in Argentina are looking into another digital ID project called Worldcoin. In August, they revealed that they’re examining potential privacy issues tied to how Worldcoin gathers, stores, and uses people’s information. The project is also facing questions in Europe and Africa since it went global in July. Created by Sam Altman, who is also a co-founder of OpenAI, Worldcoin uses eye scans to confirm the identity of its users.

After attempting to acquire FTX Europe to boost its international derivatives business, Coinbase pivoted to offer perpetual futures to qualified customers in and outside the U.S.

Coinbase, a major platform for trading cryptocurrencies, twice considered buying FTX Europe after it went bankrupt in November 2022. Their aim was to expand their services related to financial derivatives abroad.

Despite these efforts, they’ve decided to back out of the acquisition. Coinbase looked into this deal two times: once right after FTX Europe’s financial troubles in November 2022, and again in September 2023.

A Coinbase representative verified this, stating they’re continually exploring ways to grow their business globally.

Other companies like Crypto.com and Trek Labs are also reportedly interested in FTX Europe. FTX initially spent close to $400 million to set up its European division.

FTX Europe was unique in that it was based in Cyprus and was the only company to offer certain trendy financial products like perpetual futures.

A perpetual future is a type of derivative financial instrument often used in cryptocurrency markets. Unlike regular futures that have an expiration date, perpetual futures go on indefinitely until you decide to close the position. They’re designed to mimic the price of an underlying asset, like Bitcoin, without actually requiring you to own it. Traders use perpetual futures for various reasons, such as hedging against price changes or trying to profit from market movements. Traders can benefit from perpetual futures whenever the markets move, regardless of the direction, up or down.

If Coinbase had gone through with buying FTX Europe, they could have made more money from fees, especially since this type of trading is becoming more popular, even when the overall crypto market isn’t doing so well.

In fact, Coinbase made $707 million in the second quarter of 2023, though their earnings from regular trades dropped by 13% from the last quarter.

Meanwhile, globally, the trading of these financial contracts on centralised platforms went up by almost 14% in June to a staggering $2.13 trillion.

Binance led the way in this kind of trading, followed by OKX. Even Bitcoin futures trading saw a boost, especially on the CME exchange.

Coinbase now offers perpetual futures

As for Coinbase, they’ve already dipped their toes into this market in the U.S. and now just got the green light from authorities to offer this type of perpetual futures to non-U.S. qualified customers.

In the U.S., the green light from authorities allows Coinbase to offer Bitcoin and Ether futures contracts via its derivatives platform called FairX, which is overseen by the Commodity Futures Trading Commission. According to what Coinbase said when they announced this, these types of contracts make up nearly three-quarters of all crypto trading globally, making it a key entry point for traders.

Coinbase has announced its next steps in its “Go Broad, Go Deep” strategy, aiming to work closely with global regulators to shape a crypto-friendly framework.

They’ve expanded access to perpetual futures contracts to qualified customers outside the U.S., reinforcing their mission to update the global financial system.

This move comes at a time when other crypto exchanges face increasing regulatory challenges. Perpetual futures are highly sought-after, making up about 75% of global crypto trading. Coinbase sets itself apart by offering these contracts within strict compliance rules. They’ve already seen over $5.5 billion in trading volume from institutions as of the second quarter. Their exchange follows regulations set by the BMA and offers multiple layers of user protection.

What makes Coinbase unique is its emphasis on security and compliance. They guarantee a 1:1 hold on customer assets, and their financials are publicly audited. They’re also backed by a well-funded Insurance and Liquidity Support Program using the stablecoin USDC, rather than risky exchange tokens. Additionally, they have an experienced risk management team and don’t engage in market-making themselves.

As environmental concerns and costs mount, the future of crypto mining is looking increasingly green. Industry leaders are exploring alternative energy solutions for more sustainable and cost-effective operations.

In 2021, when cryptocurrency prices were soaring, big mining companies borrowed a lot of money to buy the gear and set up the systems they needed to mine crypto. But then major crypto platforms like FTX and Celsius went under, leaving many of these companies broke and struggling.

With crypto prices down and competition in Bitcoin mining fiercer than ever, people are questioning whether these mining operations can bounce back from their losses. One thing’s for sure, these companies are now looking at using greener energy options to save money, make some profit, and also be a bit kinder to the planet.

How do you keep crypto mining prices low?

According to Swan Bitcoin, a company focused on Bitcoin financial services, it generally costs around $26,000 to mine one Bitcoin.

However, companies that use renewable energy are finding it much cheaper, with costs ranging between $5,000 and $15,000 per Bitcoin.

A spokesperson from Riot Blockchain, a U.S.-based Bitcoin mining company, explained that thanks to wind and solar energy in Texas, their costs are among the lowest in the crypto mining business. To be exact, it costs Riot $8,389 to mine a single Bitcoin.

Kent Halliburton from Sazmining, a company that hosts Bitcoin mining operations, pointed out that the biggest cost in mining is electricity. He said that miners naturally want to find the cheapest power available, and renewable energy often fits the bill because it sometimes produces excess electricity. He also mentioned that data from the Bitcoin Mining Council indicates that the Bitcoin network is becoming increasingly sustainable, with 59% of mining now carbon-free and growing each year.

Phil Harvey, the CEO of Sabre56, a company providing infrastructure for crypto mining, said that they’re helping several mining companies set up operations at their facilities in Wyoming and Ohio. This move towards renewable energy appears to be a growing trend among miners who are thinking about their long-term success.

Crypto miners have ingenious designs to keep running costs low

Phil Harvey from Sabre56 said their mining center in Gillette, Wyoming, known as “Bonepile,” has around 2,200 mining machines running on a mix of energy sources. Nearly 29% of this energy is renewable, coming from wind, recovered energy, and hydropower. The machines they use are a mix of MicroBT Whatsminer M50s and Bitmain Antminer S19s. The Bonepile site uses a special design to keep the machines cool: they force air into the facility, which helps prevent the machines from overheating and allows for hot air to naturally exit.

This design is different from the usual methods used in the mining industry, where typically additional systems are used to suck hot air out, but there’s no special system to bring fresh air in.

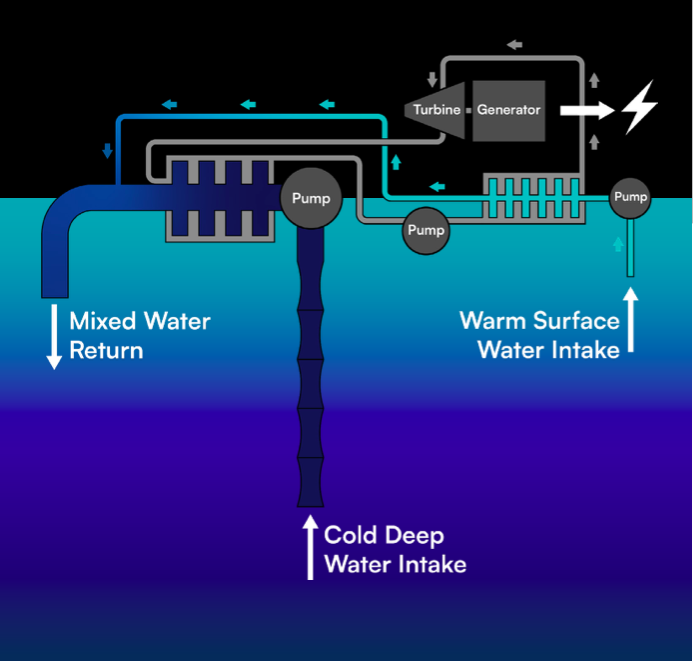

On the other hand, OceanBit is taking a unique approach to renewable energy for mining. Michael Bennett, the co-founder, explained that they are incorporating Bitcoin mining into their ocean thermal energy power plants. This allows them to adjust to fluctuating energy demands, deliver power more quickly to offshore projects, and also make extra money from unused energy.

Ocean thermal energy, according to Bennett, is a massive and largely untapped renewable energy source. It uses the temperature difference in ocean water to generate electricity, similar to how hydro and geothermal energy work. Bennett thinks that Bitcoin could be the key to making this type of energy more widely used because it helps solve some of the commercial challenges associated with ocean thermal energy.

Diagram of OceanBit’s thermodynamic cycle. Source: OceanBit

Nathaniel Harmon, who co-founded OceanBit with Michael Bennett, explained how their system is a win-win. The ocean thermal energy conversion (OTEC) process produces cold water as a byproduct, which is perfect for cooling the specialized computers used in Bitcoin mining, known as ASICs. On the flip side, these ASICs produce low-level heat, which can be recycled back into the OTEC process. This creates a cycle that makes both operations more efficient and cost-effective.

Bennett also mentioned that OceanBit is aiming to reveal its research and development power plant in Hawaii by 2024.

Alternative energy sources

Stronghold Digital Mining, a crypto mining company in Pennsylvania, is taking a different approach by using waste coal to power its mining activities.

This waste of coal, which is left over from the coal mining process and mixed with various impurities, has been a pollution issue in Pennsylvania for years. Greg Beard, the CEO of Stronghold, said they’re working with local environmental agencies to clean up these waste coal piles and use them for energy.

Beard pointed out that the waste coal has been a major source of water pollution and has also caught fire spontaneously over the years, releasing toxic fumes. By converting this waste into energy, Stronghold either powers its own Bitcoin mining or feeds electricity back into the local grid. Beard argues that this makes their operation more efficient than other miners who are just looking for cheap power.

However, this method isn’t without its critics. Using waste coal still means burning hydrocarbons, and some groups claim that these kinds of plants actually pollute more than new coal plants. Stronghold also faced backlash when it planned to burn tire-derived fuel at one of its plants. Russell Zerbo, an activist with the Clean Air Council, said that the plant should be reclassified as a solid waste incinerator, which would subject it to stricter air pollution monitoring. So, while Stronghold’s method does help clean up waste coal, it also raises environmental questions.

The challenges of using renewable energy

While it’s good news that crypto mining companies are moving towards alternative energy, there are hurdles that could slow down this transition.

Kent Halliburton mentioned that people often misunderstand the benefits that Bitcoin mining can bring to local communities, like creating jobs and making use of excess or wasted electricity. Electricity is hard and expensive to store, so if it’s not used or stored right away, it goes to waste.

Phil Harvey pointed out another challenge related to the location of their mining facility in Gillette, Wyoming. Due to the high altitude, the air is thinner, making it harder for their machines to pull in enough air for cooling.

Additionally, the issue of thermal pollution exists, where hot air from mining machines is released into the atmosphere. To counter this, some companies are getting creative. For example, Genesis Digital Assets uses the hot air generated by its mining machines to grow vegetables in colder climates.

So, while the move towards renewable energy in crypto mining is promising, there are still a variety of challenges that need to be addressed.

It looks like renewable energy will play a key role in the future of crypto mining. Bitmain, a top company in crypto mining gear, is now focusing on water-cooling technologies, as the demand for such eco-friendly options will keep rising.

Nearly 25% of all Bitcoin miners are already using water-powered setups. Wind and nuclear energy come in second and third as the most popular sources of power for these miners.

As Web3 technology gains traction in the gaming world, industry leaders discuss the hurdles and opportunities for mass adoption, predicting a significant increase in players within the next two years.

Saudi Arabia is working hard to grow its economy in new ways, so it’s not just relying on oil money.

The country is diving into the world of new tech like blockchain and artificial intelligence, and they’re also getting into the video game market.

Although Saudi Arabia isn’t yet a big name in video games or AI on a global scale, people who know a lot about this stuff think the country’s efforts could have a big impact down the line. Yat Siu, the co-founder of Animoca Brands, said that Saudi Arabia is really interested in this next wave of the internet, known as Web3.

Saudi Arabia pays to become a Web3 game developer

Saudi Arabia is teaming up with companies like The Sandbox and Animoca to explore the next phase of the internet.

Yat Siu, an executive in the industry, believes Saudi Arabia gets that the future of gaming will be tied to blockchain, where players actually own the items in the game.

Saudi Arabia is a big player in the Middle East’s growing video game market, thanks to its young people who are really into tech.

A report from Boston Consulting Group says that Saudi Arabia makes up almost half of the gaming market in the region and is worth over $1.8 billion.

In 2017, Saudi Arabia set up the Saudi Esports Federation to help grow and manage its video gaming scene. According to a Bloomberg report in April, the country invested a whopping $38 billion through its Public Investment Fund to become a big name in global gaming.

Yat Siu says that while the Saudi government understands the big picture of Web3 and how it could work with esports, there’s still some confusion. This is mainly because the country hasn’t set clear rules about things like cryptocurrency and other digital assets yet.

He also points out that other places, like Hong Kong, Japan, and the United Arab Emirates, are ahead in this area. They have clearer rules about what you can do with cryptocurrencies and Web3, making it easier to plan out a strategy.

It’s still unclear what Saudi Arabia’s plans for Web3 gaming will turn out to be, but according to Yat Siu, the country is studying other markets to figure things out. He feels that Saudi Arabia’s eagerness to be at the forefront of new technology is something special.

The incoming Web3 adoption

While some traditional gamers and developers are sceptical, games developers believe that for anyone to really get into Web3, whether in gaming or another area, they need a good understanding of finance.

At this stage, just having a bank account isn’t enough; you need a higher level of financial know-how to be a true Web3 user.

Getting people to use Web3 isn’t just about giving them a digital wallet; that’s actually the easy part.

The real challenge is making them understand that they now own something valuable, like a digital asset, and that it can do different things and has its own kind of value that needs to be maintained.

A spokesperson from FootballCoin, an independent blockchain game, says that Web3 games also allow people to be part of an ecosystem. In this way, individuals are more than simply players of the game and, basically, become a partner in the game.

Footballcoin is a Web3 game which empowers people to buy and sell digital assets. But in the end, Web3 should make the gaming experience better, not just be a way for people to make money.

While multiple Ethereum staking services are pledging to limit their market share to 22%, Lido Finance takes a different path, sparking debates on centralisation and community values.

The top five companies that offer ether staking pools for individuals have stated that they won’t control more than 22% of all ETH currently staked.

This is a way to make sure that no single company has too much power over the Ethereum network, keeping it open and fair for everyone.

Companies like Rocket Pool, StakeWise, Stader Labs, and Diva Staking are either already following this rule or planning to do so, says Superphiz, a key Ethereum developer.

Puffer Finance, another such company, has also said they’ll stick to this limit.

Lido doesn’t obey the 22% of ether staked limit

Why 22%?

Superphiz explains that to make any big changes to the Ethereum network, 66% of the participants have to agree.

By setting a limit of 22%, it ensures that at least four big companies would have to work together to push through any major updates. This makes the network safer and more secure.

When talking about blockchain transactions, the finality of a transaction is the moment when transactions are locked in place and can’t be changed.

Superphiz, a leading Ethereum developer, brought up an important question last May:

Would a company that helps people stake Ethereum be willing to put the network’s well-being over its own profits?

Lido voted by a 99.81% majority not to self-limit. They have expressed an intention to control the majority of validators on the beacon chain.https://t.co/T16rTdM3gm

Interestingly, Lido Finance, the biggest company of this kind, decided not to follow the 22% self-limit rule. Almost all of their members (99.81%, to be exact) voted against it back in June.

Superphiz mentioned in a post at the end of August that Lido aims to control most of the deciding power in the Ethereum network.

To give you an idea of how big Lido is, they control 32.4% of all Ethereum that’s currently being staked.

That’s a big deal, especially when you consider that the next largest, Coinbase, only has an 8.7% share, according to data from Dune Analytics.

Well, the Ethereum community has different opinions on that.

One expert named Mippo commented at the end of August that the 22% self-limit rule isn’t really about staying true to Ethereum’s ideals, which are about open access and innovation for everyone.

Mippo thinks that those advocating for the self-limit would probably not stick to it if they were in the dominant position like Lido Finance. In his view, everyone is just acting in their own best interest.

Yeah because they have way less market share than that now… easy to chirp from the cheap seats.

This has nothing to do with “Ethereum alignment.” None of these teams would self limit were they in Lido’s place.

Everyone is doing the economically selfish and rational thing…

Another person argued that user-friendly services shouldn’t be criticised as greedy.

On the flip side, some people are really concerned that a few big companies could end up controlling too much of the Ethereum network. They see Lido’s large market share as a problem, even calling it “selfish and disgusting.”

Honestly really disgusting and selfish

Centralization will lead to greater problems, this is a full 3 steps backward for ethereum

Lido: "We thought real hard about this for 0.2 seconds and decided it is definitely worth risking sending the entire network to zero for a fraction of a percent more yield"

Lido ticks all the boxes when it comes to staking services.

They support multiple types of digital money and make it super easy for anyone to use their platform.

Their fees are fair, and they even offer nice rewards if you refer people to their service. On top of that, they make a lot of different cryptocurrencies more available for trading and are backed by some big names in the decentralised finance world.

What’s cool is that when you stake your digital tokens with Lido, you get back tokens that are tied to the value of what you staked. You can then use these for more ways to earn money in the DeFi world.

Lido has become a top pick for people looking to stake their digital assets thanks to some standout features.

First off, staking is a breeze; you can earn daily rewards by simply staking your tokens, and there’s no minimum amount you need to start.

Want to make even more from your tokens?

Lido allows you to use them for things like loans, yield farming, and other money-making activities. This can give your earnings a nice boost.

They also have their own digital token, called LDO, that you can trade on popular exchanges like SushiSwap, Uniswap, and many more.

When it comes to security, you can rest assured. Lido’s smart contracts have been thoroughly checked by reputable firms like Quantstamp and Sigma Prime.

Although Lido doesn’t offer its own wallet, you can still use popular ones like TrustWallet and MetaMask to manage your assets.