Web3 games are still emerging. In the booming play-to-earn gaming arena, not all Web3 games and projects are created equal. Let’s delve into the complexities of Web3 gaming, exploring the issues that have hindered growth and how pioneering projects like FootballCoin have managed to innovate and thrive.

The world of play-to-earn games is more than just a way to pass the time. Players are looking for an interesting digital environment, and a huge added bonus is the ability to earn tokens or some sort of real-world benefit while getting involved in this Web3 world.

The play-to-earn games craze started in 2021. During that time, Web3 was going through big changes.

One of the highlights was a game called Axie Infinity, which allowed players in developing countries like Ghana and the Philippines to make a lot more than the minimum wage.

However, a serious issue with a token bridge and a drop in market interest caused the earnings from these games to decrease significantly.

Why most P2E games aren’t scaling?

When you take a broader look, only a few projects in the play-to-earn game world have managed to grow steadily.

This seems to be because of some basic problems with the way play-to-earn works.

To start playing, people might need to spend hundreds of dollars to buy the NFTs necessary to participate.

Even those who are willing to pay that much might be let down by the games themselves, which can have poor graphics and no real storyline.

But the issues don’t stop there.

Many Web3 games that make money through selling NFTs are still in the early stages of being made.

If the game’s developers don’t add new features quickly enough, players can become frustrated.

There can also be a need to keep coming up with new collectable items all the time to make sure there’s always money coming in.

The biggest problem, as seen with the game Axie Infinity, is related to the rewards given to players.

According to a research report by CoinGecko, For every Axie Infinity player, there are 2,155 Roblox players. While there may be many issues with the game itself, this is a clear indication that the world of Web3 games is still considered an emerging technology.

Giving away lots of tokens to attract new players might sound like a good idea, but it can actually be very harmful to the value of that digital currency.

Since the prices of digital assets change a lot and are affected by supply and demand, increasing the total number of tokens available can reduce their value.

This can lead to some pretty nasty results. Gamers who get tokens as rewards might not keep them unless there’s a really good reason to, which can put more pressure on selling and lower prices even more.

This can start a harmful cycle where the value of the digital asset keeps dropping. If the value falls by a large percentage, everyday players might stop playing, and when the community gets smaller, the entire project can fail.

Let’s look at what makes a game a Web3 experience

First of all, all Web3 are blockchain-based.

It’s not only the economy part of the project that is based on blockchain because everyone can do that.

You can recognise a Web3 project by asking yourself these questions:

Is blockchain technology used in this project?

Are there automated actions that happen when certain conditions are met?

Is it decentralised?

Can I buy or sell my digital assets?

Do I have the private keys of my wallet?

If the answer is “Yes” to all of these, then you are indeed looking at a Web3 project, and in this particular case, a Web3 game.

How to choose a good Web3 game

The first step towards a better change or choosing to spend your time and invest in a reliable Web3 game is recognising the main risks in the Web3 world today.

The success or failure of play-to-earn projects right now depends on either attracting new users or being able to keep giving rewards to current ones. Neither of these approaches is likely to work for a long time.

There’s often a lot of excitement at first, but without interesting stories or engaging gameplay to keep players interested, that excitement fades quickly.

A high-quality gaming experience might make players less concerned about earning and more focused on playing.

However, when neither earnings nor engaging play are present, players tend to lose interest and leave.

Projects are constantly trying to find a balance between drawing in new players and keeping the current ones satisfied, and it’s a struggle.

The Web3 game of the future

Even though there are big challenges facing this still-young field, Web3 gaming has the chance to be more than just a passing trend that’s not sustainable. And this has already been proven by reputable Web3 games.

FootballCoin emerged as an innovative concept in the world of gaming when it was launched in 2017.

Not just a game, it symbolises a vision to integrate the world of football fans with the burgeoning sphere of cryptocurrencies and blockchain technology.

What makes FootballCoin stand out is its holistic approach to creating a world-class gaming experience.

The developers didn’t merely focus on providing a fun experience; they also enabled players to win real prizes.

Through this game, participants can engage in football manager-type contests and fantasy sports, appreciating the tangible benefits of blockchain technology.

FootballCoin’s economy is another unique aspect.

The game has introduced two major types of player cards – free and collectable. In the Web3 world, these collectables are known as NFT trading cards or sports cards.

These trading cards, ranked based on the player’s real-world value, notoriety, and achievements, bring an additional layer of complexity and engagement to the game.

In a market where partnerships and collaboration often dictate success, FootballCoin’s affiliations with reputable companies like Sportradar, Perform, Omnisport, and BoostIT stand as a testament to its credibility.

Its cryptocurrency, XFC, has also gained respect, being listed on well-known exchanges such as Coindeal, Livecoin, InstaSwap, and Exrates.

From the perspective of a technology enthusiast, the game represents a project that respects core Bitcoin philosophies.

For gamers, it’s a gateway to a top-level gaming network where they can win real cryptocurrency rewards.

In a landscape filled with fleeting trends and unsustainable models, FootballCoin shines as a durable Web3 project that has withstood the test of time.

It continues to innovate and grow, carving a niche that bridges the gap between the crypto sphere and the passionate world of football fans.

Its continuous delivery on promises, alignment with both gaming and tech values, and innovative integration of blockchain technology make FootballCoin an exemplary model in the industry.

After PayPal’s recent introduction of PYUSD, the market examines the prospective use cases and benefits of this new stablecoin, especially within the U.S., highlighting its potential utility within the existing financial framework.

PayPal, a leading global payments company, is making its debut in the crypto realm with a U.S. dollar-backed stablecoin named PayPal USD (PYUSD). The announcement came on August 7, 2023.

What is PYUSD?

According to PayPal’s official statement, this new crypto called PYUSD is 100% backed by USD:

“PayPal USD is designed to contribute to the opportunity stablecoins offer for payments and is 100% backed by U.S. dollar deposits, short-term U.S. Treasuries, and similar cash equivalents. PayPal USD is redeemable 1:1 for U.S. dollars and is issued by Paxos Trust Company. “

The PYUSD stablecoin, built on the Ethereum platform, will soon roll out to American PayPal customers.

This is the first instance of a premier financial service launching its own stablecoin.

With PYUSD, users have the option to transfer between PayPal and approved external crypto wallets, employ the coin for various transactions, or exchange it with other cryptocurrencies supported on PayPal, like bitcoin (BTC) and ether (ETH).

PayPal emphasized that their stablecoin is poised for adoption by an expansive and evolving network of external developers, digital wallets, and web3 platforms and is also primed for easy integration by crypto trading platforms.

Paxos Trust, a crypto financial services firm located in New York, will oversee the issuance of PYUSD.

The coin is underpinned by U.S. dollar reserves, short-term government securities, and other cash-like assets. Moreover, users can redeem it for U.S. dollars or trade it for other digital currencies available on PayPal’s platform.

At the time of the launch, PayPal’s CEO Dan Schulman remarked, “Our commitment to responsible innovation and compliance, and our track record delivering new experiences to our customers, provides the foundation necessary to contribute to the growth of digital payments through PayPal USD.”

It is expected that PYUSD to be available later on the Venmo app as well.

How will the PYUSD be monitored?

PayPal’s PYUSD stablecoin reserves will be monitored and verified through a multi-step process to ensure transparency and trustworthiness:

Monthly Reserve Report

Starting from September 2023, Paxos, the firm in charge of issuing PYUSD, will release a public monthly Reserve Report for PayPal USD. This report will detail the specific assets that make up the reserves backing the stablecoin.

Third-party Attestation

In addition to the monthly report, Paxos will also release a public third-party attestation on the value of the PayPal USD reserve assets. This is to double-check and confirm the validity of the reserves.

Independent Accounting Firm

The attestation process will be carried out by an external, independent accounting firm. This ensures that there’s no conflict of interest and that the process is free from potential biases.

Adherence to Established Standards

The attestation will comply with standards set by the American Institute of Certified Public Accountants (AICPA). This means the audit will follow rigorous professional guidelines, ensuring the accuracy and reliability of the information.

PYUSD is a stable issued by a regulated company

PYUSD, launched by fintech leader PayPal, is distinct from other stablecoins due to its robust regulatory framework. PayPal’s PYUSD stands out in the stablecoin landscape due to its unique position of being backed by a trust company that is stringently regulated by the NYDFS.

This sets it apart from major stablecoins like USDT and USDC.

Here’s how PYUSD is regulated:

Issued by a regulated entity

Paxos Trust, the company behind the issuance of PYUSD, operates as a trust company. This status subjects them to direct oversight by a regulatory authority.

Regulatory oversight by NYDFS

Paxos is regulated by the New York Department of Financial Services (NYDFS). This means that the entire process of issuing PYUSD, including the management of its reserves, is under the constant supervision of NYDFS.

Protection by regulator

Walter Hessert, the head of strategy at Paxos Trust, highlighted the importance of having a prudential regulator. With such oversight, every activity linked to PYUSD’s issuance is monitored. For token holders, regardless of their location worldwide, this ensures that they benefit from the protection and guidelines established by New York’s regulatory framework.

Bankruptcy safeguard

One of the significant rules established by the NYDFS concerning PYUSD is the protection against bankruptcy risk. Should Paxos face bankruptcy, the assets of PYUSD token holders are safeguarded. The NYDFS would intervene, ensuring that PYUSD is excluded from the bankruptcy process. Consequently, token holders would not become involuntary creditors during a bankruptcy, and their funds would be promptly returned.

Clear differentiation from other stablecoins

Both USDT (issued by Tether) and USDC (jointly issued by Circle and Coinbase) dominate the stablecoin market. However, as Hessert pointed out, both these coins are unregulated, albeit transparent in their operations. In contrast, PYUSD’s regulatory structure offers an additional layer of security and trust for its users.

Why did PayPal decide to issue a stablecoin?

PayPal’s decision to issue the PYUSD stablecoin is emblematic of its substantial influence and strategic positioning in the financial sector.

While there’s undeniable regulatory uncertainty surrounding cryptocurrencies in the U.S., PayPal’s stature enables it to not only navigate but also potentially influence these regulatory decisions.

Companies like Coinbase and Circle may have paved the way in the crypto regulation space, but major entities like PayPal are sending a clear message: they can effectively handle and even counteract regulatory pressures.

At its core, PayPal’s move is driven by the prospect of profitability. The issuance of PYUSD isn’t a minor endeavor, requiring collaboration across several of PayPal’s departments, from compliance to communications.

However, this decision wasn’t born out of altruism. Instead, it’s a calculated business move, made in response to a rapidly evolving digital financial landscape, reinforcing PayPal’s dominant position and highlighting its confidence in seizing new lucrative opportunities.

What’s the use case for PYUSD?

The use case for PYUSD appears to be in its infancy, and its exact utility for the average consumer remains somewhat ambiguous.

Introduced via Venmo, PYUSD essentially provides another avenue for banked Americans to transact using a digital representation of the U.S. dollar, aligning with how most PayPal products have functioned since the company’s inception.

However, one distinct feature is that PYUSD can potentially be sent outside of PayPal’s proprietary ecosystem using the Ethereum network.

This capability hints at a use case where individuals barred from Venmo or PayPal could potentially transfer their funds via an Ethereum-based PYUSD withdrawal.

Yet, this use case might be limited, given the centralized nature of the stablecoin.

In essence, while the stablecoin could offer a mechanism to navigate around restrictive banking scenarios, its primary use cases might lean more towards backend financial operations that institutions can leverage, rather than direct consumer applications.

NYU law professors Richard Epstein and Max Raskin published a paper to explain the potential hazards of central bank digital currencies, highlighting the risk of overstepping governmental boundaries and the importance of maintaining the ‘separation of money and state’.

Central banks worldwide are swiftly progressing with their explorations in creating digital currencies.

Numerous examples, such as the recent announcement of a successful prototype by the New York Federal Reserve or the Bank of England’s achievement in the subsequent phase of its digital pound trial, indicate that over 130 nations globally are considering the idea of central bank digital currencies (CBDCs).

The reasoning behind this is twofold.

Firstly, central banks can position themselves as protectors of consumers and innovators in cost-saving technologies by eliminating the role of private banking intermediaries.

Secondly, they can acquire an additional mechanism for policymaking.

However, the proposition of excluding these intermediaries raises an important question of who would be responsible for the other end of the financial transactions.

The inevitable answer is a far-reaching and intrusive government capable of monitoring every single expenditure.

Digital cash?

Max Raskin, an adjunct professor of law at New York University and a fellow at the school’s Institute for Judicial Administration, and Richard Epstein, a law professor at New York University, a senior fellow at the Hoover Institution, and a senior lecturer at the University of Chicago, are exploring this topic in a paper called “A Wall of Separation Between Money and State: Policy and Philosophy for the Era of Cryptocurrency,“ published in The Brown Journal of World Affairs.

Their argument suggests that a central bank, for instance, the Bank of England, would issue a “digital pound,” which would be a direct claim on the central bank, much like current cash is.

This process would involve creating the necessary infrastructure for individuals to store digital pounds in digital wallets and facilitate interactions with retailers and other users.

Contrasting current practices where central banks such as the Federal Reserve and the Bank of England do not offer accounts to direct depositors, the proposed model would eliminate the costly private banking system that presently stands between the central bank and the accounts held by businesses and individuals.

At a glance, it seems that CBDCs might cut unnecessary costs.

However, these apparent efficiency benefits can be deceptive and hazardous.

Intermediaries function in thousands of markets, with representatives, aggregators, and monitors in almost every significant business line. These participants can’t be easily deemed obsolete.

Intermediaries often provide value as they are motivated to offer more than the bare minimum to stand out – such as new banking products and services.

The variety of services banks can offer due to competitive pressures that ultimately benefit consumers. Restricting these forces can hamper the market economy.

CBDC implementation can be risky

The implementation of CBDCs is not without risks.

The idea of providing extensive power and confidential information to a faceless government entity can be alarming. The system can use that data against you in numerous ways.

By removing the private banking intermediaries, CBDCs would eliminate a crucial barrier that currently safeguards individuals and firms from government intrusion and overstepping.

The use of cash and bearer instruments is currently untraceable by the central government.

However, the use of digital cash would be.

It’s clear that even those who decide to stick with private bankers will still be scrutinised by the state, which holds control over all transactions.

Moreover, these digital funds would empower central banks to direct personal loans and mortgages to specific private parties with minor competition, raising concerns around state industrial policies. It’s not hard to imagine potential nightmare scenarios, yet they are difficult to avert.

The question remains: can we trust thousands of new banker-bureaucrats to perform any better?

Can we trust banks?

The Bank of England, in its digital pound argument, emphasised the British government’s commitment to fighting climate change, stating that the digital pound would be designed with this objective in mind.

Why should a topic as intricate and contentious as climate change be regulated through the financial system?

Similarly, U.S. financial regulators have started to wade into political issues like climate change.

If such explicit political objectives are considered, it is not a stretch to imagine a government-run bank using its powers to favour certain energy producers and punish others through their bank accounts.

The power to impact credits and debits must be a feature of the central banks’ proposed code, which introduces a covert system of industrial policy.

If CBDCs become a reality, officially favoured energy sources like solar and wind power could witness their bank accounts receiving subsidies without the need to attract private investors or undergo the scrutiny of the private banking system.

Bank accounts could become vulnerable to political manipulations, bureaucracies, or even disenfranchisement overnight with limited recourse.

Furthermore, these CBDC initiatives in the U.S. were originally proposed in the context of directly providing pandemic stimulus to the economy. However, the evidence is overwhelming that this hasty system of government payments was incredibly wasteful.

Moreover, central banks could implement countercyclical monetary policies, such as providing cash boosts to individuals in specific regions or sectors, which again becomes a political football.

Money and new technologies

We should undoubtedly strive to leverage new technologies, but only when implemented correctly. According to the paper in the Brown Journal of World Affairs, “Money should be a neutral unit of measurement, like inches or kilograms.”

This concept, referred to as the “separation of money and state,” aims to stabilise all currencies over time, minimising the need for private parties to design complex and costly mechanisms like adjustable-rate mortgages to handle financial instability.

For instance, Bitcoin has a predetermined supply of no more than 21 million units, not governed by any individual institution but rather by the network’s consensus mechanism.

This feature provides a robust defence against value dilution that no government-centric system could hope to match.

This fixed system could offer additional institutional support for developing countries seeking modernisation.

Countries with a history of mismanaging their monetary systems could benefit from the discipline that comes with certain forms of digital currency.

For instance, a central bank like Zimbabwe‘s or Argentina’s, plagued with mismanagement, could adopt an innovative form of dollarisation using Bitcoin or another form of programmed cryptocurrency.

As the dawn of the new digital age ushers in, the synergy of blockchain and artificial intelligence (AI) is transforming multiple industries. These cutting-edge technologies are not just trending buzzwords, but robust tools that promise to revolutionize business operations, data security, and decision-making processes.

Blockchain and AI in financial services

Blockchain and Artificial Intelligence (AI) are combining to revolutionize the financial industry. Financial institutions handle massive amounts of data, and AI and blockchain can manage this data more efficiently.

By automating processes and examining data on the blockchain, these institutions can improve risk management and compliance. For example, AI algorithms can sift through financial data on the blockchain to detect potential fraud and money laundering. Here, blockchain technology guarantees that the data is safe and unalterable.

Take FactSet, a global provider of financial data and analysis software, for instance. They’re using AI and blockchain to enhance their risk management and compliance processes. AI algorithms are used to scrutinize the company’s financial data housed on a blockchain to identify potential fraud and other irregularities. At the same time, the company’s blockchain technology safeguards the algorithms and data.

Blockchain and AI in supply chains

Beyond finance, AI and blockchain have other valuable uses. In the transport sector and other industries, AI can boost the efficiency and transparency of supply chains.

AI algorithms can analyze data on the blockchain to identify supply chain inefficiencies, helping companies optimize their operations. Simultaneously, blockchain technology ensures the transparency and traceability of products in the supply chain by maintaining records of logistics documents and ensuring visibility of goods’ locations.

Blockchain and AI in healthcare

In healthcare, AI and blockchain can bring significant improvements. AI, by analyzing medical data on the blockchain, can help identify patterns in patient data, aiding doctors in making accurate diagnoses and treatments. The blockchain technology can be used to safeguard patient data, an essential requirement in healthcare.

Blockchain and AI in life sciences

Blockchain and AI are joining forces in the life sciences field, particularly in the pharmaceutical industry, to significantly enhance operations. They offer much-needed transparency and tracking abilities for the drug supply chain while significantly boosting the success rate of clinical trials.

By combining AI’s advanced data analysis capabilities with blockchain’s decentralized structure, these technologies bring about increased integrity and transparency to clinical trial data. They facilitate better patient tracking and consent management, along with automating the process of trial participation and data collection. In simple terms, AI digs deep into data to uncover valuable insights, while blockchain ensures that this data is securely stored and transparently managed, boosting the overall effectiveness of clinical trials.

Blockchain and AI in security and verification

Blockchain acts as a robust protective layer for AI systems with its encryption-backed, decentralized structure. This allows AI developers to set specific access parameters for AI, enforced by private keys and tamper-proof infrastructure like blockchains and smart contracts. Unlike centralized systems vulnerable to a single point of failure, a decentralized blockchain system is spread across multiple nodes and keys, making it harder for a single attacker to compromise the system.

This synergy between AI’s utility and blockchain’s security reduces attack possibilities, enhancing the safety of AI applications. It empowers organizations to harness AI’s full potential while maintaining high security standards supported by cryptographic assurances.

Blockchain also plays a vital role in verifying the authenticity of different media types, an aspect particularly crucial with the rise of deep learning models that can generate images and media from text prompts. These models, while promoting productivity and creativity, could be misused to spread misinformation or create deceptive synthetic media.

Blockchain technology, backed by cryptography and encryption, can validate the authenticity of a piece of content by verifying its origin and any alterations. Cryptographic watermarking, for example, can ensure tamper-proof timestamping.

In a future where distinguishing between AI- and human-generated content is crucial for societal stability, blockchain could facilitate the creation of decentralized platforms for content verification and distribution. It ensures that the spread media is unaltered, authentic, and has a transparent, verifiable history.

Non-fungible tokens (NFTs), unique digital assets on the blockchain, can also help verify the authenticity and provenance of digital content. NFTs can represent ownership and verify the origins of various media forms. When content is minted as an NFT, its origin, ownership history, and modifications become transparent and easily verifiable. This adoption can enhance online content accountability, helping differentiate between genuine and tampered content.

AI in cryptocurrency

AI (artificial intelligence) plays a significant role in the world of cryptocurrencies by aiding in market analysis, enhancing monetization insights, automating trading strategies, and predicting market trends.

Firstly, AI uses sentiment analysis to gauge public feelings towards specific cryptocurrencies. Using natural language processing, AI can sift through large volumes of data from the internet and blockchain, and analyze the sentiment—negative, neutral, or positive—quickly. This can help predict potential price changes, offering valuable insights for investors.

Secondly, AI can provide more profound insights into cryptocurrency monetization. Given the vast amount of unstructured data online, AI assists data scientists in producing clean, relevant data for traders, making it easier to spot valuable investment opportunities.

AI also plays a role in fully automated trading strategies for cryptocurrencies. High-frequency trading, in which a computer executes numerous orders in fractions of a second, often relies on AI to mimic human intelligence. This speedier trade execution gives investors an edge over slower competitors.

Lastly, AI aids in accurately predicting cryptocurrency market trends. With the increasing number of investment options, AI is becoming an essential tool in the financial industry.

Large financial firms already use AI in their workflows to discover new investment opportunities and buy/sell signals, with smaller businesses following suit. Combined with blockchain, AI becomes an even more powerful tool for predicting market trends.

How can blockchain improve AI?

Blockchain technology can significantly enhance AI in several ways. Firstly, by boosting trust. Blockchain’s permanent, transparent records can help explain how AI algorithms work and reveal the source of their data, enhancing people’s confidence in AI’s data integrity and recommendations.

Secondly, blockchain’s decentralized data storage can increase data security and integrity. It acts as an audit trail, allowing users to understand how their data is used. If AI models are stored on blockchains, their decisions become more accountable and transparent.

Thirdly, blockchain can help AI expand by providing access to both internal and external data. This enables more actionable insights, better data management, and shared models, potentially creating a more trustworthy and transparent data market.

Fourthly, the fusion of AI and blockchain can automate multiparty business processes, reducing the need for human intervention. Blockchain technology can eliminate unnecessary third parties from transactions, accelerating their speed and efficiency. This reduces transaction friction and enables individuals to own their data, while blockchain secures the transaction process.

Lastly, blockchain can assist with AI’s high computational power demands. As a distributed ledger technology, it can utilize the computing power of multiple machines, an asset that centralized data servers may struggle to provide. In essence, integrating blockchain with AI can lead to more trustworthy, transparent, efficient, and powerful AI systems.

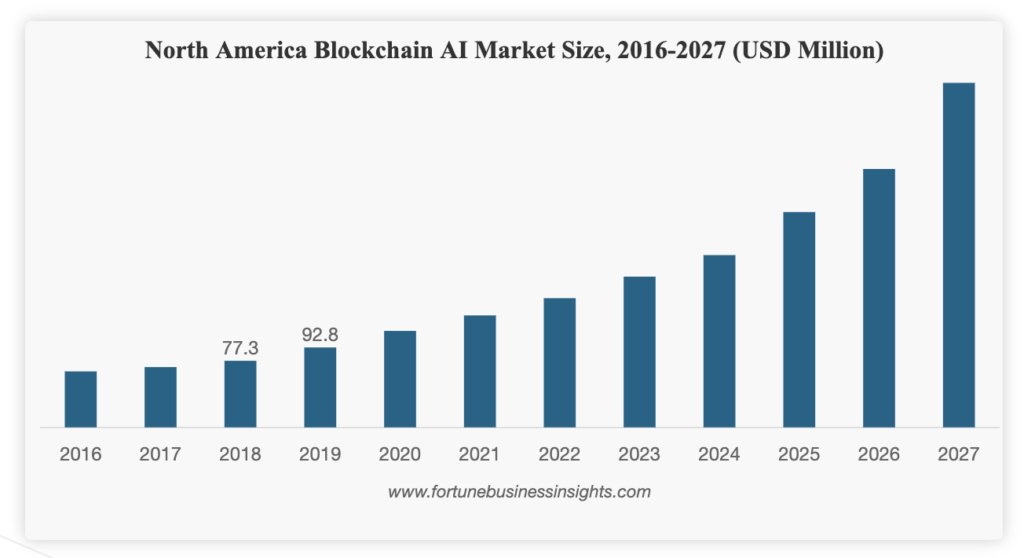

According to this report from Fortune Business Insights, the blockchain and AI market is expected to grow to over $973.6 million in 2027, “at a CAGR of 23.6% in the 2020-2027 period.”

Companies using AI and blockchain

CertiK. Provides tools powered by AI and formal verification to secure blockchain, smart contracts, and Web3 applications. With its product suite, CertiK technology helps identify security risks, monitor data insights, and visualize where crypto funds are going.

Core Scientific. Integrates personalized blockchain and AI infrastructure with current business networks, upgrading a business’ physical infrastructure, servers, and software in the process. The facilities are designed for long-term digital asset mining and to maximize hashrate, always running at optimal efficiency to reduce energy and time consumption.

Token Metrics. A tool that uses AI to analyze cryptocurrency trends for personal investment purposes. The technology scans the data of over 6,000 crypto and NFT projects and extracts market insights to help users make investment decisions.

AI BlockChain. Hosts a digital asset cloud platform built on blockchain and AI. The company applies artificially intelligent agents to its blockchain to detect changes and ensure platforms are secure.

Bext360. Uses AI and blockchain to boost supply chain transparency and efficiency in the coffee, timber, seafood, and mineral industries. The AI analyzes crops and predicts growing patterns, while blockchain ensures the recording of a product’s supply chain from seed to finished product.

Blackbird.AI. Uses its blockchain and artificial intelligence to gauge the credibility of news content in the communications and information industries.

BurstIQ. The LifeGraph platform combines AI and blockchain technology to provide enhanced ownership and management over patient data.

Chainhaus. A blockchain and AI advisory, education, and software development firm. The company provides a variety of end-to-end solutions for everything from teaching and app development to research and capital raising.

Cyware. Incorporates AI and blockchain-based tools into its cybersecurity and threat intelligence solutions.

Dobby. A home services platform for homeowners seeking assistance with maintenance or repair projects. The AI-based application operates on blockchain technology to exchange data quickly and reduce any financial loss.

Figure. Uses blockchain and artificial intelligence to streamline the home loan process. The platform offers home equity line of credit loan options, investment marketplaces and its own digital money app called Figure Pay.

Gainfy. A healthcare platform that employs blockchain, AI and IoT devices to improve the industry experience.

Hannah Systems. Brings AI and blockchain to autonomous vehicles with its portfolio, including an AI-powered data exchange platform, a real-time mapping tool, an insights dashboard, and blockchain.

Hashed Health. A venture studio based on blockchain that elevates startups in the healthcare industry.

Home Lending Pal. An application for home mortgage advising, comparison, and more. The AI-based platform allows users to view local homes, calculate personal budgeting, and choose their preferred home lender based on related mortgage rates.

Imaginovation. Builds and hosts customer-centric applications for clients in need. Utilizing solutions from blockchain, AI, IoT, AR, and VR, applications can be created for purposes ranging from manufacturing to entertainment.

MOBS. A blockchain-based video marketplace for the selling and buying of smartphone videos. The blockchain creates a smart contract that directly allocates money to the content creator based on engagement rates and views.

NetObjex. Merges blockchain and AI to host its NFT marketplace platform, where users can create their own marketplaces and digital wallets as well as host metaverse events.

Neureal. A prediction engine that combines AI, blockchain, and cloud technologies to predict everything from the stock market to Google searches.

Numerai. A decentralized hedge fund at which data scientists from all over the world are constantly working on AI problems.

Stowk. A blockchain-based platform that features AI tools for almost every part of a business’s operations, streamlining everything in supply chain management from data access and IT governance to procurement.

Verisart. Uses artificial intelligence and blockchain to help create and certify NFT work in real-time.

Vytalyx. A healthtech company using AI to give healthcare professionals blockchain-based access to medical intelligence and insights.

WealthBlock. An automated marketing and messaging SaaS platform for businesses raising capital. Blockchain powers the company’s investor referral and suitability checking process.

WorkDone. Helps businesses automate daily processes and discover insights to retain employees. The company specializes in machine learning and blockchain to seek out resource bottlenecks, analyze best management practices, and continually maintain service compliance.

In a groundbreaking development, a judge ruled that XRP is not considered a security in the Securities and Exchange Commission’s (SEC) case against Ripple. This ruling has significant implications for the future of XRP and the broader crypto industry.

On July 13, 2023, Ripple Labs won against the SEC, and XRP was declared to not be a security.

The company achieved a notable win in the United States District Court in the Southern District of New York when Judge Analisa Torres issued a partial ruling in favor of the company. This ruling pertained to a case brought against Ripple by the Securities and Exchange Commission (SEC) that dates back to 2020.

It’s official, Ripple’s token (XRP)is not a security

Based on documents filed on July 13th, Judge Torres granted summary judgment in favor of Ripple Labs.

The ruling clarified that the XRP token should not be considered a security, specifically in relation to its programmatic sales on digital asset exchanges.

However, the SEC also secured a victory of its own as the federal judge determined that XRP qualified as a security when sold to institutional investors. This classification was based on the conditions outlined in the Howey Test.

The SEC’s lawsuit aimed to compel Ripple to cease offering its XRP token, arguing that it qualified as a security and, therefore, required additional regulatory measures.

According to court documents, the motion for summary judgment by the defendants has been granted for Programmatic Sales, Other Distributions, and the sales made by Larsen and Garlinghouse. However, it has been denied for Institutional Sales.

This means that the XRP token is not considered a security when sold through retail digital asset exchanges.

After this news broke, the price of XRP surged from $0.45 to $0.61 within a few minutes.

The legal case against Ripple began in December 2020 when the Securities and Exchange Commission (SEC) filed a lawsuit against Ripple and its two top executives, Brad Garlinghouse and Chris Larsen.

The SEC alleged that the company was offering an unregistered security.

Throughout the past three years, the case has been filled with dramatic twists, including the release of the “Hinman Documents” and Garlinghouse’s ongoing defiance in response to the SEC’s accusations.

In addition to the noticeable price movement of the XRP token following this news, the general sentiment within the cryptocurrency community seems to be one of celebration and joy.

XRP’s non-security status

Ripple CEO Brad Garlinghouse is confident that the United States Securities and Exchange Commission (SEC) will face a lengthy process before being able to appeal the recent ruling in its case against Ripple Labs.

During an interview with Bloomberg on July 15, Garlinghouse downplayed the significance of the ruling regarding institutional sales, referring to it as “the smallest piece” of the overall lawsuit. He expressed his belief that if the SEC were to appeal the ruling on retail sales, it would only serve to reinforce Judge Torres’ decision.

Despite acknowledging that it may take a considerable amount of time before the SEC can file an appeal, Garlinghouse firmly stated his belief in the current legal status of XRP: “Based on the current law of the land, XRP is not classified as a security. Given the lengthy process required for the SEC to file an appeal, which could take years, we maintain a high level of optimism.”

Garlinghouse emphasized that this marks the first instance where the SEC has faced a setback in a “crypto case.” He openly criticized the SEC, referring to them as “bullies” who target players in the crypto industry unable to mount a strong defense.

We said in Dec 2020 that we were on the right side of the law, and will be on the right side of history. Thankful to everyone who helped us get to today’s decision – one that is for all crypto innovation in the US. More to come.

He highlighted the initial response of various U.S. crypto exchanges when the lawsuit against Ripple was initially filed.

Many took a cautious approach, waiting to observe the outcome due to the uncertainty surrounding the case. Consequently, exchanges such as Coinbase and Kraken decided to delist XRP entirely.

Garlinghouse accused the SEC of deliberately creating confusion in the market. He claimed that the SEC was aware of the existing confusion and intentionally engaged in actions that further exacerbated the situation.

According to Garlinghouse, this deliberate confusion was a means for the SEC to exert its power, hindering innovation within the United States. He criticized the SEC for prioritizing power and politics over the establishment of clear regulatory frameworks, resulting in difficulties for entrepreneurs and investors seeking to participate in the U.S. crypto market and blockchain industry.

Why are NFT prices falling? What to avoid when buying NFTs from a crypto project?

Remember the popular NFT collection called Bored Ape Yacht Club (BAYC)?

This collection became extremely valuable in early 2022, but as of 2023, its popularity has faded, causing prices to drop dramatically.

The lowest price for one of these NFT artworks, also called the ‘floor price’, has fallen from 153.7 ETH (a type of digital currency) to 27.4 ETH.

This ‘floor price’ helps indicate the overall worth of the art collection, so a big drop in the floor price means that the value of individual pieces has also taken a big hit.

One popular example of a BAYC NFT price decrease that has been circulating on social media is a piece owned by Justin Bieber, which was once valued at $1.3 million and is now only fetching offers of around $58,000.

That being said, those who bought these artworks early are still doing okay, as these pieces are still quite valuable compared to other NFTs.

However, this isn’t the only digital asset that’s seen prices skyrocket and then crash in recent years. In fact, it’s pretty much keeping pace with the overall NFT market, which is at its lowest in two years.

However, there are important lessons to be learned from this situation.

Many people, especially those who invested heavily, have paid a steep price to learn these lessons. So if you can learn from their experiences without losing money yourself, it’s wise to do so.

Beware of projects which use extreme marketing

The Bored Apes always had an intense marketing campaign going on.

Such unnatural hype can artificially inflate an asset’s value and make its market more fragile. For digital assets like these, it can result in investors who don’t really understand what they’ve bought into.

It encourages risky speculation over genuine engagement, weakening the market. A stable market should be built on cultural value and real affection for the asset, not just a flashy advertisement.

Additionally, when these NFTs are showcased in mainstream media, it might prompt wealthy individuals to buy many, raising the entry price for new investors and creating potential points of failure.

For instance, when a major Ape owner rapidly sold dozens of NFTs earlier this year, it drove the market to a five-month low.

A healthy digital art market needs a diverse community of engaged, individual owners, not a bunch of speculators ready to sell at the first sign of trouble.

Don’t rely on digital assets to maintain a stable value

Some Bored Ape owners have used their Apes as loan collateral and are now facing losses as values fall.

For example, BendDAO, a loan service, is selling dozens of Apes that were taken as collateral for unpaid loans.

This is just one of many similar services, and these forced sales might even be causing Bored Ape values to spiral downwards.

The notion that NFTs could be used as reliable financial tools this early in their existence is highly doubtful, even though providing such a service might be profitable.

But borrowing against a volatile asset, whether it’s a digital one or not, is a terrible idea.

Now these borrowers are seeing their Apes being sold off at the market’s lowest point instead of potentially waiting for a better time.

Joining late can be costly

Those suffering the most right now are the latecomers who bought Apes NFTs at peak prices.

Some have suffered larger losses than even Justin Bieber, and it’s unlikely they’ll recover their investments.

The issue with this is that investors, especially new crypto investors, will find it challenging to identify when a market is overpriced.

However, there are a few red flags to watch out for. Be wary if you see heavy marketing (such as an Ape being promoted on late-night TV shows). Such hype could be driving up the asset’s price beyond its real value.

A cautious approach is to realize that if others are already making huge profits, it’s probably too late for you to benefit from that surge, regardless of the asset. You might end up being the one left holding the bag.

This is especially true for community-driven NFTs.

If everyone around you is buying into a rising asset expecting future profits, they’re probably all doing the same thing.

A bubble in NFTs can actually harm the organic growth of its community.

Of course, another aspect is also the utility of that said digital asset. While some projects have a blockchain game, such as Footballcoin, which gives true utility to their NFTs, most do now.

Most projects will use words such as “unique” or “innovative” to describe their assets but will spend little time explaining the mechanics of the project. These are other red flags that you should consider when judging an NFT project.

Don’t mix arrogance with digital assets

Remember the exclusive BAYC yacht parties?

Some of the negative feelings towards Apes stem from typical behavior seen during a booming crypto market, such as over-the-top parties.

However, Ape owners also seem to have earned a reputation for being unusually arrogant and self-centered. To many people, an Ape picture is like a rude tweet mocking those who don’t understand why a digital monkey image could be worth half a million dollars.

While this behavior might have been a reaction to widespread ridicule towards the Apes, it was a strategic blunder (similar to what we see with Bitcoin). Now, the lack of goodwill towards Apes, whether within the crypto community or in general, is resulting in less financial support for these assets.

This is because the community of owners plays a vital role in the value of NFTs like these. For instance, the communities of other NFT collections, like Wassies and Miladies, have done a much better job at maintaining their value compared to Apes over the past year, although they started from a lower price point.

This may not be a lesson you’d learn in a traditional market, but it’s an important one. Most of us are now paying more attention to the Apes’ downfall partly because of how the owners behaved when things were going well.