Raiffeisen Bank’s Austrian branch and top Australian crypto exchanges, including Independent Reserve, BTC Markets, Swyftx, Kraken, and Binance Australia, are gearing up for an anticipated surge in the crypto market. The Austrian Bank is set to offer cryptocurrency trading, while Australian exchange leaders are bolstering their infrastructure and customer education initiatives.

Raiffeisen Bank’s Austrian branch is gearing up to introduce cryptocurrency trading for its customers. This means you will be able to trade Bitcoin directly on the bank’s platform. This move, first mentioned in April 2023, is now taking shape through a partnership with Austrian crypto company Bitpanda.

The plan is to launch these crypto trading services in Vienna, starting in the early months of 2024.

A bank spokesperson shared that they’ve teamed up with Bitpanda to create a user-friendly digital investment platform, responding to their clients’ growing interest in easy and accessible digital investments.

Raiffeisen wants to keep up with its customers’ investment desires

The bank is enthusiastic about this new venture, emphasizing its commitment to meeting customer needs and preferences.

“We have seen the demand from customers for easy, intuitive, digital investment platforms. Our main intention to take customer-centric decisions has triggered these efforts, which we are excited about bringing to market.”

As part of their new crypto initiative, customers of RLB NÖ-Wien, a branch of Raiffeisen Bank, will have access to a wide range of cryptocurrencies offered by Bitpanda, their partnering firm.

Bitpanda’s Deputy CEO, Lukas Enzersdorfer-Konrad, had mentioned that this collaboration would include Bitpanda’s extensive digital asset portfolio, which boasts over 2,500 cryptocurrencies, such as Bitcoin and Ether.

Furthermore, Enzersdorfer-Konrad highlighted that Raiffeisen aims to make these crypto trading services available to all types of clients, including those in retail, private banking, and the corporate sector.

“As we announced in April, the end goal is to make our offer available to all RLB NÖ-Wien customers. However, the rollout will begin with their customers in Vienna,” a spokesperson for Bitpanda noted.

Raiffeisen Bank’s venture into cryptocurrency trading is a further indication of the increasing acceptance of Bitcoin and other digital currencies.

Established as one of Europe’s oldest banks, Raiffeisen’s roots date back to its first branch opening in Mühldorf, Austria, in 1886.

As of June 30, 2023, the Raiffeisen Group managed assets totalling 247 billion Swiss francs (equivalent to about $280 billion) and had client loans amounting to 219 billion CHF (around $248 billion).

Banks are taking note of the increase in popularity of cryptocurrencies, just as the bull market is expected to start.

Australian Exchanges Anticipate Market Growth

Australia’s top crypto exchange leaders are preparing for an anticipated bull market, expecting a rapid increase in business. Adrian Przelozny of Independent Reserve is ensuring his exchange is ready with the necessary processes, people, and infrastructure to handle a potential tripling of business overnight. He optimistically predicts the next two years to be promising for the crypto market.

BTC Markets’ Caroline Bowler has observed more bullish market conditions since January, with notable growth in asset prices and technological applications in the industry. She cites the influx of new users and increased trading volumes as signs of an emerging bull market.

Tommy Honan from Swyftx reports a rise in buying activity and is enhancing direct debit functions, a recent challenge in Australia’s crypto sector. He attributes this increase to improved market fundamentals, not just investor FOMO, noting a return of customers who were inactive during the bear market.

Jonathon Miller of Kraken Australia urges caution, pointing out the grey area between bull and bear markets. However, he acknowledges reasons for optimism, such as the upcoming Bitcoin halving and Ethereum’s Dencun upgrade, which are attracting both institutional and retail investors. He highlights the growing institutional interest in crypto assets.

Ben Rose from Binance Australia observes an increase in new registrations and trading activity but refrains from confirming a bull market. Focusing on educating users, Rose aims to avoid FOMO-driven buying, emphasizing sustainable and responsible engagement with crypto as part of financial management rather than just price-driven interest.

In a significant move since the FTX collapse, former executives have collaborated to create a cutting-edge cryptocurrency exchange. This platform emphasises security, incorporating a self-custody approach with advanced multiparty computation techniques to ensure robust protection of customer funds.

A group of former employees from the cryptocurrency exchange FTX have joined forces to create a new crypto exchange in Dubai.

This new venture aims to address a key issue FTX struggled with – keeping customer funds safe.

Who is involved in this new crypto exchange?

Can Sun, previously a lawyer for FTX, is leading this initiative with a company called Trek Labs. Trek Labs, based in Dubai, recently got a license to provide crypto services in the region. They will operate under the name Backpack Exchange.

Supporting Sun in this endeavour is Armani Ferrante, another ex-FTX employee. Ferrante is the CEO of Trek’s parent company in the British Virgin Islands. He also oversees Backpack, a crypto wallet that’s part of Backpack Exchange. This collaboration was detailed in a report by The Wall Street Journal on November 11.

Claire Zhang, who worked closely with Sun at FTX and is Ferrante’s wife, is also a key member of Trek’s executive team. However, she plans to leave the company after an investment round is raised. The Wall Street Journal mentioned that Zhang has been contributing without a salary to support the early stages of the exchange’s development.

Will this new exchange be better than FTX?

Sun and Ferrante, both former FTX executives, are keen on applying the lessons they learned from the downfall of FTX, particularly in safeguarding customer assets.

They’re introducing a self-custody feature in their new venture, Backpack, which uses a multi-party computation (MPC) method. This approach requires multiple approvals for any transaction, enhancing security.

Additionally, Backpack will allow its customers to check their funds at any time. Sun highlighted to The Wall Street Journal the importance of trust and transparency in the current financial landscape, especially after the FTX collapse.

Backpack Exchange is currently undergoing beta testing, with plans for a broader rollout later in the month, as per the company’s announcement.

Sun was also involved in the recent fraud trial of Sam Bankman-Fried, FTX’s former CEO. He testified, revealing that Bankman-Fried had consulted him for legal advice regarding the use of FTX’s funds by Alameda Research. Bankman-Fried was found guilty on all seven charges related to fraud.

Disillusioned by the misuse of customer funds, Sun resigned from his role as FTX’s general counsel the day after learning about these practices. He expressed his disappointment, noting that this went against his principles and what he was led to believe by Bankman-Fried.

The collapse of Bankman-Fried’s empire was marked by the misuse of billions in customer funds through Alameda Research for investment purposes, resulting in approximately $9 billion in missing customer funds.

What happens when you deposit funds on a crypto exchange?

In simple terms, here’s what’s happening with your funds when you interact with a centralized crypto exchange.

Crypto exchanges are where you can buy, sell, or store your cryptocurrencies. However, not all exchanges operate the same way. Some might use your funds in ways you don’t expect, like investing them in other ventures, which can be risky.

The collapse of FTX is a key example. The CEO allegedly used customer funds for other investments, leading to huge losses. This shows that if the people running the exchange are not trustworthy, your funds could be at risk.

Exchanges use hot wallets (online) and cold wallets (offline) to store crypto. Cold wallets are safer from hacking but less convenient for quick transactions. Most exchanges keep a mix of both to balance safety and convenience.

Exchanges are now focusing more on self-custody options, meaning you have more control over your crypto. They are also using advanced security measures like multi-party computation to protect funds.

Exchanges with securities registration are held to higher standards, which include keeping comprehensive records and being subject to regulatory inspections. This is important for the safety of your funds.

What can you do to protect your funds?

Always research an exchange or broker before investing.

Understand their business model, how they store and use your funds, and what security measures they have in place.

It’s crucial to be aware of the risks and choose platforms that prioritise the safety of your funds.

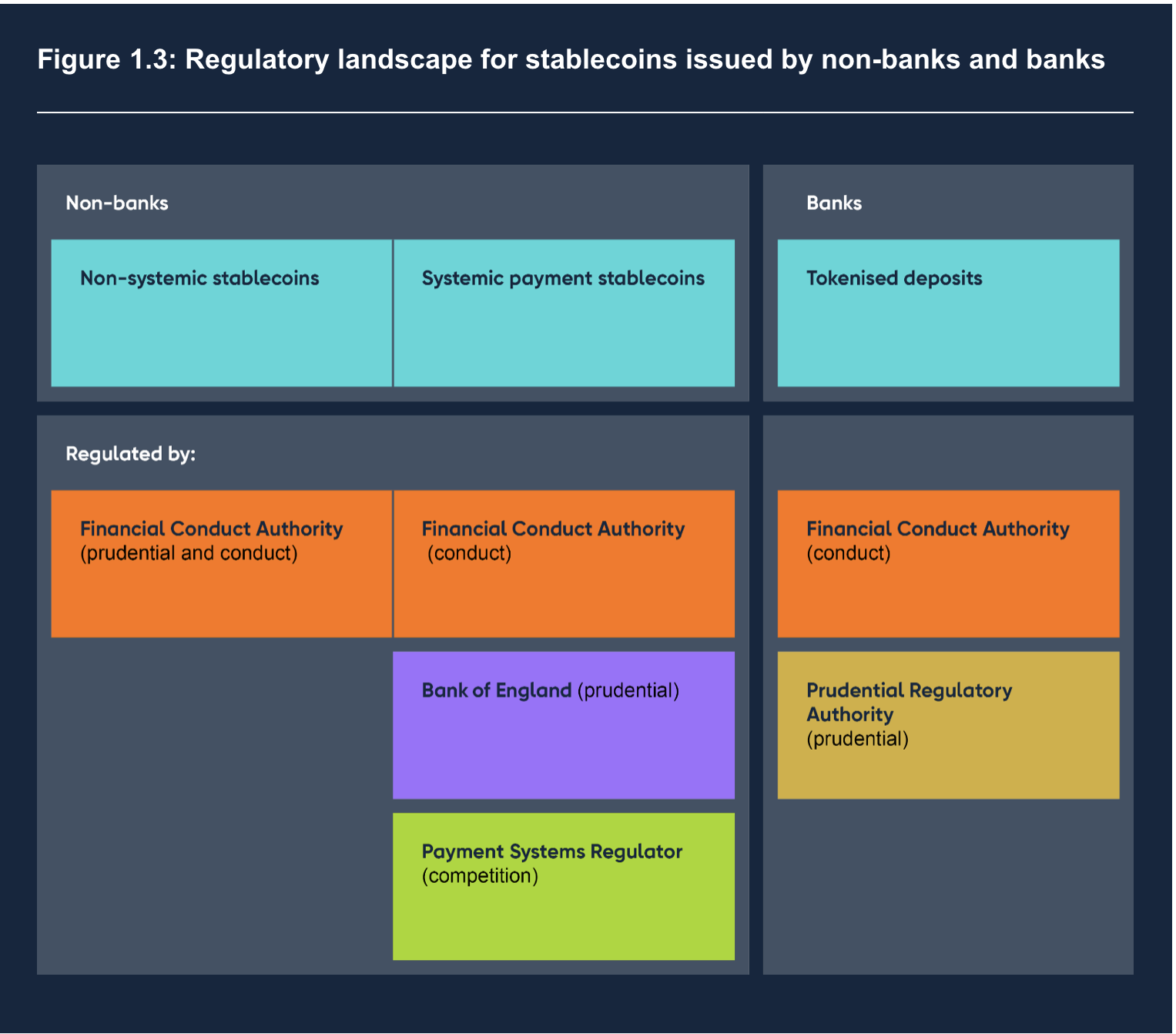

While the new regulatory framework for UK stablecoins is slated for a 2025 rollout, recent papers from the Financial Conduct Authority and the Bank of England provide an early look into the future landscape of digital currency regulation, revealing the direction and thought process of the UK’s financial watchdogs.

The UK is serious about launching a stablecoin. On November 6th, a collection of important papers was shared with the public about new rules for stablecoins, which are cryptocurrencies designed to have a stable value.

The Financial Conduct Authority (FCA), which looks after the fairness of financial markets, and the Bank of England (BOE), the UK’s central bank, both presented their ideas on the subject. Also, the BOE’s Prudential Regulatory Authority (PRA), which supervises banks, sent out a special note to the heads of banks. Moreover, the BOE created a plan to connect all these different pieces.

Before these papers came out, the UK Treasury gave us a sneak peek on October 30th of what to expect regarding new stablecoin rules. The FCA then went into much more detail, sharing their thoughts on how stablecoins could be used in day-to-day shopping and in big financial dealings, what kind of checks and balances might be needed, and how the coins and the assets backing them should be managed separately to avoid conflicts of interest.

According to the FCA, getting the regulation of stablecoins right is a critical first step towards creating a broader set of rules for all sorts of digital currencies.

The document focused on how to ensure that the same level of risk would lead to the same regulatory treatment. It suggested taking the current rules for looking after clients’ assets as a starting point for new guidelines on how people can get their money back from stablecoins and how those coins should be safely kept.

It also referred to an existing manual for senior managers on how to set up their company’s systems and controls properly. The paper mentioned that there are already rules in place for keeping financial operations running smoothly and for preventing financial crimes, among other things.

The Financial Conduct Authority (FCA) is thinking about adjusting the current financial rules for those who issue stablecoins and look after them, with the aim of applying these adjusted rules to other types of cryptocurrencies in the future.

The Bank of England (BOE) considered how stablecoins, which are tied to the value of the pound and aimed at everyday use, could be integrated into major payment systems. It looked at how stablecoins should be transferred, what the providers of digital wallets and related services should do, and how this connects with the FCA’s ideas about issuing stablecoins and protecting deposits.

While the BOE expects to lean on the FCA to oversee those who keep stablecoins safe, it hasn’t ruled out setting some of its own rules if needed. It highlighted the challenges in regulating wallets that don’t rely on a third party and transactions that take place outside of the blockchain, especially when it comes to preventing money laundering and ensuring that businesses know their customers.

Source: Bank of England

The letter from the Bank of England’s Prudential Regulatory Authority (PRA) made it clear that banks need to distinguish between “e-money or regulated stablecoins” and traditional deposits. They pointed out that as various new digital currencies and currency-like options become available, it’s easy for everyday customers to get mixed up if banks were to market e-money or stablecoins the same way they do with regular bank deposits.

The PRA suggested that banks should focus their creative efforts on traditional deposits and keep any activities related to issuing digital currencies or stablecoins separate, including using different branding. If a company that issues these digital assets wants to also accept deposits in the traditional sense, they should act swiftly and keep the PRA in the loop from the start. The letter also reminded these institutions that any new developments in the area of deposit-taking are still governed by existing rules and regulations.

Source: Bank of England Prudential Regulatory Authority

The plan set out by the Bank of England includes a schedule that aims to have the new system up and running by the year 2025.

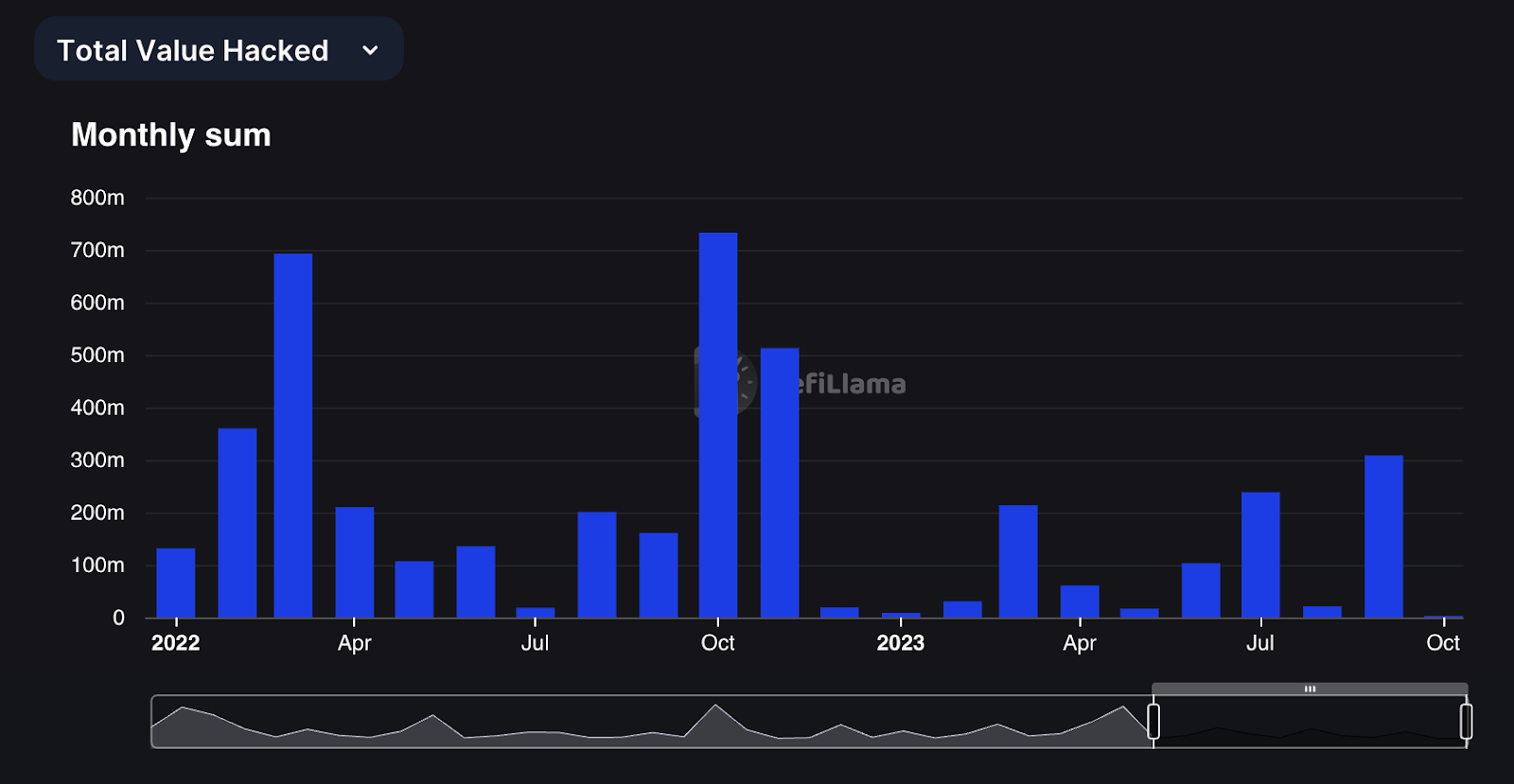

With a staggering $1 billion in crypto gone missing in 2023, how is on-chain data and blockchain analysis painting a nuanced picture of hackers’ motives while helping to recover stolen riches? Get the inside scoop on how these digital tools keep you one step ahead in the crypto game.

The world of decentralised finance (DeFi) and Web3 is like the Wild West of the internet—fast, thrilling, and downright risky. Just this year, a jaw-dropping $1 billion vanished into thin air or landed in the wrong hands. Yep, you read that right, according to the DefiLlama.

But don’t worry, it’s not the end of the world. A new league of digital guardians is rising to the occasion. From folks who specialise in decentralised IDs to the Sherlock Holmes of smart contract audits, there’s a whole squad working around the clock to keep this virtual playground safe.

Oh, and let’s not forget our notorious villains. Meet the Lazarus Group, North Korea’s own state-backed hacking squad. These guys have siphoned off a staggering $291 million this year alone. They even pulled off a Hollywood-style heist on CoinEx, swiping more than $55 million. It’s like a cyber-thriller unfolding in real-time, reminding us that this new frontier is exciting but still has its fair share of bad actors.

According to a 2023 Chainalysis report, illicit crypto inflows are down 65% compared to where they were at the same time in 2022.

What’ crypto and blockchain security?

Let’s spice things up a bit! Imagine your digital wallet gets hacked, and your crypto goes poof—vanished! What do you do? Enter blockchain analysis, the detective work for the crypto world. Even big companies sometimes drop the ball when it comes to dodging digital theft, so knowing a thing or two about this can be your own superhero cape.

So, what is blockchain analysis? It’s like being a digital Sherlock Holmes, digging through transaction histories to find where the stolen crypto went. Here’s a quick rundown:

Transaction tracing: Think of this as following a breadcrumb trail. Analysts keep an eye on every movement of the stolen cryptocurrency.

Address clustering: This is like connecting the dots. They group together related wallet addresses to see where the stolen money might have been moved.

Behavioural analysis: Ever notice someone acting sketchy? It’s the same here. By looking at transaction patterns, analysts can spot anything that seems off and might point to theft.

Pattern recognition: This is about learning from the past. Analysts use old data and known tricks hackers have used before to catch new threats faster.

Regulatory vigilance: The government is stepping in, too. They’re making rules stricter to make sure people can’t use crypto for shady stuff like money laundering.

Team effort. It’s not a one-man show. Often, these analysts team up with the police, crypto exchanges, and other big players to either freeze the stolen money or get it back.

Everything you need to know is on the blockchain

When a cryptocurrency hack goes down, it’s not just a “whodunit,” but also a “how-can-we-fix-it,” and our digital Sherlock Holmes has a trusty toolkit for just that. Enter blockchain analysis, the magnifying glass for all those cryptic crypto transactions.

But wait, there’s another star in this crime-busting duo—Open-source intelligence, or OSINT for short. Imagine it as the Watson to blockchain analysis’s Sherlock. OSINT dives deep into the digital world, sifting through clues using nifty tools like Etherscan, Nansen, Tenderly, Ethective, and Breadcrumbs. It’s like the Swiss Army knife of cyber-sleuthing.

Mash up the keen eye of blockchain analysis with the broad reach of OSINT, and what do you get? A turbocharged, crime-solving engine that not only pins down the bad guys but also has a good shot at getting back that stolen loot.

So, the next time you hear about a crypto heist, remember: our digital detectives are on the case, armed with blockchain analysis and OSINT, making the virtual world a little safer, one solved case at a time.

Tracking down the crypto hacker

Get this—sometimes crypto villains have a change of heart! Take the Curve Finance exploit, for example, where the baddie walked away with $61 million in digital dough.

Plot twist: the hacker returned nearly $9 million not because they were scared of getting caught, but because they wanted to keep the systems they hacked into running smoothly. Yeah, it sounds like something out of a comic book, but this is real life, and it shows how complex the ethics of the crypto world can be.

What helped crack the case?

It’s all thanks to the digital fingerprints left on the blockchain.

On-chain data is like the DNA test of the crypto world. It gives us a crystal-clear view of who did what, when, and where. It’s like a treasure map that helps you understand how to keep your assets safe and sound while steering clear of the digital booby traps.

So whether you’re a casual enthusiast or a crypto guru, this ever-evolving landscape is full of opportunities and threats. Just remember, knowing is half the battle, and in this high-stakes game, knowledge can be your superpower.

There’s a growing momentum for crypto adoption in Europe, from stablecoins to digital euros. European agencies and companies are taking steps to make the digital financial landscape more accessible and regulated.

ESMA crypto guidelines

On October 20, two major European financial agencies released a paper to discuss new rules regarding how individuals interact with crypto assets. These are called the European Banking Authority (EBA) and the European Securities and Markets Authority (ESMA). These rules are aimed at checking if the people running and investing in crypto-related companies are qualified for their roles.

The guidelines offer a common way for regulators to decide if these people are suitable for giving permission to launch new crypto assets or services. This includes making sure they have the necessary knowledge, skills, and time commitment for their roles.

The new guidelines aim to make the cryptocurrency market more trustworthy and consistent. They are open for public feedback until January 22, 2024.

Looking ahead to new rules that will be in place by June 30, 2024, the EU’s banking authority has also suggested that companies dealing with stablecoins should start following certain best practices for managing risks and protecting consumers. These initial suggestions were shared with the public on July 12 to clarify what will be expected under the upcoming crypto regulations.

Digital Euro project

In February 2023, a Finnish firm called Membrane Finance launched a stablecoin tied to the euro. The CEO, Juha Viitala, believes this regulated coin, called EUROe, will help more people in Europe to increase their money using decentralised financial apps (DeFi).

On October 18, the European Central Bank said they’re entering the “preparation phase” for their digital euro project. This stage will take two years and will be about setting the final rules and choosing who will issue the digital euro.

Transaction anonymity of digital Euro

On October 18, European privacy agencies released a statement about the digital euro, a new type of money suggested by the European Commission in July 2023. These agencies gave advice on how to better protect people’s personal information.

For example, they said that rules around how much digital euro one person can have need to be clearer. Right now, the European Central Bank and national banks can see all of a user’s information through one access point, and the agencies think that needs to be reconsidered. They believe there are technical ways to store this data without centralising it.

They also said that the current plans for spotting fraud could be too intrusive and suggested finding less invasive methods. The agencies strongly recommend setting up a privacy limit for small, everyday transactions that don’t need to be tracked for anti-money laundering reasons.

Meanwhile, the European Central Bank said it’s moving ahead with its digital euro project. After two years of studying the idea, they are now going to spend another two years finalising the rules and picking who will be in charge of issuing this digital money.

Private stablecoins vs Central Bank Digital Currencies (CBDCs) in Europe

Here’s a comparison between private stablecoins and Central Bank Digital Currencies (CBDCs) in the European context:

Private Stablecoins like EUROe

Issuers. Issued by private companies, such as Membrane Finance in Finland.

Regulation. While they aim to be regulated, the guidelines are not always as stringent as those for traditional currencies.

Accessibility. Generally, it is easier to acquire and use, especially for those familiar with cryptocurrencies and decentralised finance (DeFi) platforms.

Purpose. Often aimed at facilitating trade and investment in the DeFi ecosystem.

Trust. Reliance is primarily on the issuing company and its ability to maintain a 1:1 peg with the euro.

Anonymity. The level of transaction privacy depends on the issuing company’s policies and technology.

Central Bank Digital Currencies like the Digital Euro

Issuers. Issued by a country’s central bank, in this case, the European Central Bank (ECB).

Regulation. Heavily regulated and backed by the government, making them a more “official” form of currency.

Accessibility. Likely to be more universally accessible but may require more stringent identity verification.

Purpose. Aimed at a wider array of applications, including retail payments, cross-border transactions, and even government disbursements.

Trust. Backed by the government, thereby considered more secure and stable.

Anonymity. Subject to government regulations, including Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) laws, meaning less potential for anonymity, especially for large transactions.

Explore the cutting-edge developments in the world of digital currencies, from China’s groundbreaking digital yuan hub to the impending launch of Japan’s DCJPY. Discover how Finland is embracing the digital euro, and witness JPMorgan’s successful cross-border payments pilot with First Abu Dhabi Bank.

China Unveils Shenzhen Hub for Digital Yuan CBDC Innovation

China has launched an industrial park in Shenzhen aimed at fostering the development of the digital yuan ecosystem.

This groundbreaking initiative, reported on Oct. 11 in Chinese media, marks the establishment of the first-ever park dedicated to the central bank digital currency (CBDC), also known as the e-CNY.

Situated in Shenzhen’s Luohu district, adjacent to Hong Kong, the industrial park is commencing its operations with nine initial residents.

Reports indicate that the district government has introduced ten strategic initiatives to accelerate the growth of the digital yuan ecosystem. These initiatives encompass the advancement of payment solutions, smart contracts, hard wallets, and the promotion of the digital yuan.

In an effort to incentivise new residents, the government is offering compelling benefits, including up to three years of rent-free accommodation.

Commercial banks that choose to establish a presence in the park can receive incentives of up to 20 million yuan ($2.7 million), while startups may be eligible for support of up to 50 million yuan ($6.9 million).

The total government support allocated for this endeavour amounts to 100 million yuan ($13.7 million). Additionally, favourable loan terms are being extended to participants.

Notably, among the inaugural residents of the park are prominent entities such as Hengbao, Wuhan Tianyu Information, and Lakala Payment. Hengbao and Tianyu are engaged in the production of payment cards, among other endeavours, while Lakala Payment operates as a payment processor and collaborates with Visa.

The Shenzhen Digital RMB Industrial Park officially launched operations on Wednesday, according to a press briefing held in the southern Chinese metropolis of Shenzhen https://t.co/Pi3Z6bjUvppic.twitter.com/SehYDnhoUu

China has implemented numerous strategies to stimulate the adoption of the digital yuan, which is currently in the pilot phase.

This initiative spans 26 cities participating in the pilot program, and the central bank digital currency (CBDC) is already accepted by 5.6 million merchants—a number that is expected to steadily increase, thanks to government support and technological advancements.

Notably, the digital yuan app recently introduced a feature allowing tourists to link their Visa and Mastercard accounts, further enhancing its accessibility. Despite these efforts, the adoption rate is still perceived as sluggish, with 261 million digital yuan wallets created as of 2022.

Japan to launch its digital currency in 2024

In a significant development, the DCJPY, a digital currency backed by the Japanese yen, is set to launch in July 2024. This ambitious project is spearheaded by DeCurret Holdings, a digital currency and electronic payments firm, as detailed in their white paper released on October 12.

The DCJPY Network, outlined in the white paper, will comprise two key zones: the Financial Zone and the Business Zone.

The former will facilitate banks in minting digital currency deposits on the blockchain, while the latter will be dedicated to conducting transactions.

Additionally, the Business Zone will serve as a platform for the issuance of nonfungible tokens, security tokens, and governance tokens.

Aozora Bank, a commercial institution with 19 branches in Japan, is poised to become the principal issuer of DCJPY.

The digital currency will be fully backed by Japanese yen deposits.

In 2021, DeCurret reported the formation of a consortium consisting of 70 Japanese companies that will participate in the DCJPY Network. While the white paper doesn’t disclose specific participant names, DeCurret boasts the support of 35 shareholding companies, including prominent names such as Japan Post Bank, Mitsubishi, and Dentsu Group.

In related news, the Bank of Japan, in May 2023, disclosed the results of the second phase of its central bank digital currency experiment and is on track to make a final decision on issuing a “digital yen” by 2026.

Simultaneously, Binance and Mitsubishi UFJ Trust and Banking Corporation are actively exploring the issuance of Japanese yen and other foreign currency-denominated stablecoins within the country.

First Abu Dhabi Bank Successfully Concludes Cross-Border Payments Testing on JPMorgan Onyx

In a significant milestone, First Abu Dhabi Bank (FAB) has wrapped up its cross-border payments testing on JPMorgan’s Onyx platform. This achievement follows a similar pilot conducted by Bank ABC in Bahrain.

JPMorgan, known for its cutting-edge blockchain solutions, has also introduced its Tokenization Collateral Network on the Onyx platform.

The blockchain-based cross-border payments pilot project between JPMorgan’s Onyx Coin Systems and FAB was executed seamlessly, with response times meeting expectations, according to an official statement.

Notably, the FAB pilot concluded shortly after a successful test in Bahrain, where Bank ABC trialed the Onyx system and subsequently initiated a limited launch of services.

JPMorgan’s permissioned distributed ledger, launched in 2020, has been gaining substantial traction in recent months. Tyrone Lobban, the Head of JPMorgan Onyx Digital Assets and Blockchain, disclosed that the platform currently processes a daily volume ranging from $1 billion to $2 billion.

Moreover, Onyx has expanded its reach beyond the Middle East, serving as a platform for euro-denominated payments in Europe since June.

During the same period, it also facilitated interbank United States dollar settlements in India through collaboration with a consortium of six banks.

On October 11, JPMorgan’s groundbreaking Tokenization Collateral Network, operating on the Onyx blockchain, recorded its first public trade.

In this instance, money market fund shares were tokenised and securely deposited at Barclays Bank to support a derivatives exchange between JPMorgan and BlackRock.

The finance industry has witnessed increased interest in tokenisation, with Mastercard testing its Multi Token Network in June and Citigroup introducing Citi Token Services in September.

This collaborative effort, concluded in June, was initiated by the Monetary Authority of Singapore and the Bank for International Settlements. It focused on creating a liquidity pool of tokenised bonds and deposits for lending and borrowing purposes.

Finland Forges Ahead with Instant Payments and Digital Euro Initiatives

The Bank of Finland (BOF) is taking active steps to foster innovative payment solutions.

BOF, under the guidance of Tuomas Välimäki, a BOF board member and a member of the Governing Council of the European Central Bank (ECB), has announced its role in coordinating the development of a Finnish instant payment system aligned with European standards.

Välimäki emphasized the significance of the digital euro, referring to it as the most prominent project within the European payment sector. He highlighted the potential of a digital euro, stating, “The possible introduction of a digital euro would give consumers the option of paying with central bank money wherever electronic payment is accepted.”

The Bank of Finland, in collaboration with the European Payments Council, is actively engaged in crafting this Finnish instant payment solution.

It’s worth noting that this solution will be based on credit transfers, eliminating the reliance on traditional payment card infrastructure.

In February 2023, a Finnish company named Membrane Finance took a significant step by launching a fully reserved stablecoin backed by the euro, known as EUROe.

Membrane Finance CEO Juha Viitala expressed optimism about EUROe’s potential to encourage more Europeans to explore decentralised finance (DeFi) applications and enhance their financial well-being.

On October 18, the governing council of the European Central Bank (ECB) initiated the “preparation phase” for the digital euro project, a two-year period aimed at finalising regulations for the digital currency and selecting potential issuers.

Finland’s proactive stance in embracing instant payments and exploring the digital euro reflects the country’s commitment to staying at the forefront of modern payment solutions.

Source: Bank of England

Source: Bank of England Source: Bank of England Prudential Regulatory Authority

Source: Bank of England Prudential Regulatory Authority