While the new regulatory framework for UK stablecoins is slated for a 2025 rollout, recent papers from the Financial Conduct Authority and the Bank of England provide an early look into the future landscape of digital currency regulation, revealing the direction and thought process of the UK’s financial watchdogs.

The UK is serious about launching a stablecoin. On November 6th, a collection of important papers was shared with the public about new rules for stablecoins, which are cryptocurrencies designed to have a stable value.

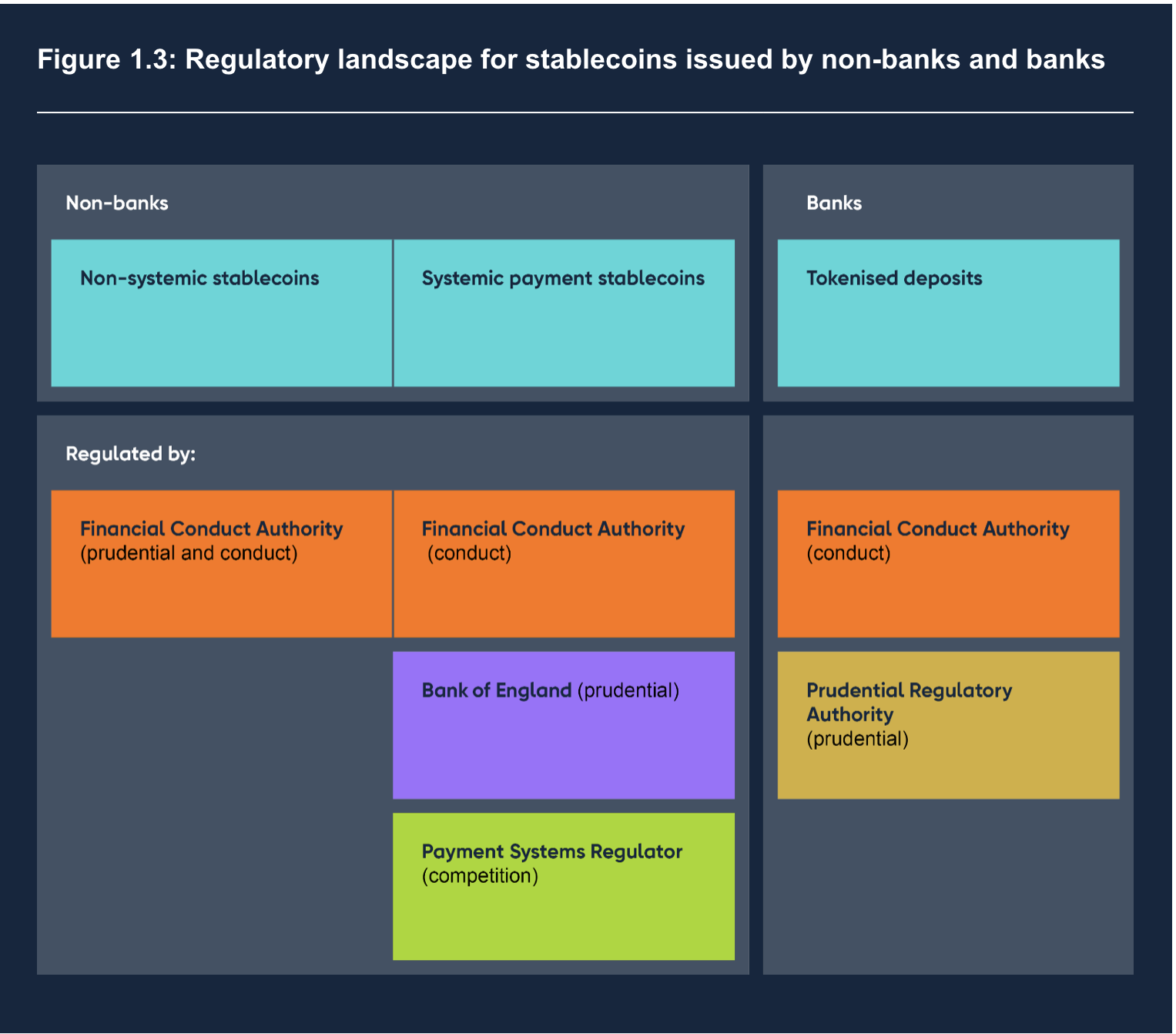

The Financial Conduct Authority (FCA), which looks after the fairness of financial markets, and the Bank of England (BOE), the UK’s central bank, both presented their ideas on the subject. Also, the BOE’s Prudential Regulatory Authority (PRA), which supervises banks, sent out a special note to the heads of banks. Moreover, the BOE created a plan to connect all these different pieces.

Before these papers came out, the UK Treasury gave us a sneak peek on October 30th of what to expect regarding new stablecoin rules. The FCA then went into much more detail, sharing their thoughts on how stablecoins could be used in day-to-day shopping and in big financial dealings, what kind of checks and balances might be needed, and how the coins and the assets backing them should be managed separately to avoid conflicts of interest.

According to the FCA, getting the regulation of stablecoins right is a critical first step towards creating a broader set of rules for all sorts of digital currencies.

The document focused on how to ensure that the same level of risk would lead to the same regulatory treatment. It suggested taking the current rules for looking after clients’ assets as a starting point for new guidelines on how people can get their money back from stablecoins and how those coins should be safely kept.

It also referred to an existing manual for senior managers on how to set up their company’s systems and controls properly. The paper mentioned that there are already rules in place for keeping financial operations running smoothly and for preventing financial crimes, among other things.

The Financial Conduct Authority (FCA) is thinking about adjusting the current financial rules for those who issue stablecoins and look after them, with the aim of applying these adjusted rules to other types of cryptocurrencies in the future.

The Bank of England (BOE) considered how stablecoins, which are tied to the value of the pound and aimed at everyday use, could be integrated into major payment systems. It looked at how stablecoins should be transferred, what the providers of digital wallets and related services should do, and how this connects with the FCA’s ideas about issuing stablecoins and protecting deposits.

While the BOE expects to lean on the FCA to oversee those who keep stablecoins safe, it hasn’t ruled out setting some of its own rules if needed. It highlighted the challenges in regulating wallets that don’t rely on a third party and transactions that take place outside of the blockchain, especially when it comes to preventing money laundering and ensuring that businesses know their customers.

The letter from the Bank of England’s Prudential Regulatory Authority (PRA) made it clear that banks need to distinguish between “e-money or regulated stablecoins” and traditional deposits. They pointed out that as various new digital currencies and currency-like options become available, it’s easy for everyday customers to get mixed up if banks were to market e-money or stablecoins the same way they do with regular bank deposits.

The PRA suggested that banks should focus their creative efforts on traditional deposits and keep any activities related to issuing digital currencies or stablecoins separate, including using different branding. If a company that issues these digital assets wants to also accept deposits in the traditional sense, they should act swiftly and keep the PRA in the loop from the start. The letter also reminded these institutions that any new developments in the area of deposit-taking are still governed by existing rules and regulations.

The plan set out by the Bank of England includes a schedule that aims to have the new system up and running by the year 2025.