Web3 games are set to redefine the landscape of video games by integrating blockchain technology, NFTs, and decentralized platforms.

As gaming projects continue to evolve and new Web3 standards emerge, the gaming industry is on the brink of a transformative shift.

What is web3 games?

Web3 games are a new type of video game that uses blockchain technology to give players true ownership of in-game assets.

Unlike traditional games, where items and characters are owned and controlled by the game developers, web3 games allow players to buy, sell, and trade their assets as NFTs (non-fungible tokens) on platforms and wallets like web3 Metamask.

This means that even if the game shuts down, players still retain ownership of their items.

Web3 games also integrate cryptocurrencies, allowing players to earn and spend gaming coins. These games can be played on various devices, including mobile phones and special web3 gaming consoles, and are a key part of the growing metaverse.

The web3 gaming market is expanding rapidly, with new gaming projects and platforms emerging to meet web3 standards and enhance the gaming experience.

Current web3 games adoption

Right now, the blockchain game scene isn’t seeing the adoption everyone was expecting, especially after the big market hit of NFTs.

However, a 2022 report from Crypto.com found that “Blockchain gaming is estimated to grow to $50B by 2025, a growth rate 10x of traditional gaming.”

This means there’s a huge opportunity for game developers to create and market these new types of games. Even though popular web3 games like Axie Infinity and The Sandbox are well-known in the crypto community, they haven’t made a big impact on mainstream gamers yet.

This untapped market presents a significant chance for growth and innovation in the gaming industry. As users get more used to these crypto games, we can expect a surge in other, lesser-known games in the next couple of years.

Examples of existing blockchain and web3 games

Axie Infinity. Players collect, breed, and battle creatures called Axies. Players can earn cryptocurrency by winning battles and selling Axies.

Gods Unchained. It is a trading card game where players collect and trade cards, battling each other to win matches. The cards are NFTs, giving players true ownership and the ability to trade them.

Star Atlas. It is a space exploration game where players build spaceships, form alliances, and explore the universe. The game’s economy is built on blockchain, allowing players to own and trade in-game assets.

FootballCoin. This is a fantasy football game where players create teams using blockchain-based player cards. Players earn rewards based on the real-life performance of their chosen footballers.

Decentraland. Welcome to a virtual world where players can buy, sell, and build on virtual land. The land and other assets are owned as NFTs, and players can create various experiences within the world.

The Sandbox. Another metaverse where players can create, own, and monetize their gaming experiences. Players use blockchain to trade virtual real estate and in-game items.

CryptoKitties. A game where players collect, breed, and trade virtual cats, each represented as an NFT. The game’s novelty lies in its focus on digital collectibles and breeding mechanics.

Splinterlands. A digital card game where players build decks to battle each other. Cards are NFTs, allowing players to trade and sell them, with each card having unique stats and abilities.

Illuvium. An open-world RPG where players capture and train creatures called Illuvials. Players can battle with their Illuvials and earn cryptocurrency by participating in the game’s economy.

My Neighbor Alice. A multiplayer builder game where players can buy and own virtual islands, collect items, and meet new friends. The game’s assets are NFTs, providing players with true ownership and the ability to trade items.

The core problems with traditional gaming

Traditional gaming has several issues. When game studios shut down, players lose their in-game purchases and downloadable content (DLC), which they cannot recover or resell.

The centralized nature of the gaming industry means that studios and publishers control all aspects of the game, leaving players with little say or ownership.

Additionally, traditional games offer few opportunities for players to make money, limiting their ability to earn from their gaming efforts.

Blockchain gaming addresses these problems by giving players true ownership of their in-game assets and the ability to trade or sell them, creating new economic opportunities.

The promise of blockchain gaming

Blockchain gaming offers solutions to key problems in traditional gaming by ensuring true ownership of in-game assets and enabling reselling.

In these games, items and characters are represented as NFTs, which players can trade or sell outside the game. Axie Infinity exemplifies the economic potential of blockchain games. Players earn cryptocurrency by collecting, breeding, and battling creatures called Axies, with some earning significant income.

There is a distinction between partial and fully on-chain games. Partial on-chain games, like Axie Infinity, use blockchain for asset ownership but rely on central servers for gameplay.

Fully on-chain games, however, store all game assets, mechanics, and states on the blockchain, ensuring greater transparency, security, and player control. This approach provides a more decentralized and empowering gaming experience.

According to DAppRadar, most blockchain games don’t have much over 100k users, but any blockchain tool don’t provide the whole image and none have listed all the web3 games in existence.

Traditional Games vs. Blockchain Games

Difference

Traditional Games

Blockchain Games

Ownership of assets

Players do not own in-game items; these are controlled by the game developers.

Players have true ownership of in-game assets, which are represented as NFTs.

Reselling and trading

In-game items cannot be sold or traded outside the game.

Players can buy, sell, and trade their assets on various marketplaces, even outside the game.

Economic opportunities

Limited opportunities for players to earn money.

Players can earn cryptocurrency through gameplay, creating new income streams.

Security and transparency

Game data and assets are stored on centralized servers, which can be vulnerable to hacks and data loss.

All game data and assets are stored on the blockchain, offering enhanced security and transparency.

Player control

Game developers and publishers control all aspects of the game, including asset distribution and game rules.

Players have more control over their assets and can participate in governance decisions in some games.

Persistence and availability

Games and servers can be shut down by developers, causing loss of access to in-game items.

Assets exist independently of the game; even if the game shuts down, players retain ownership of their items.

Decentralization

Centralized control by game developers and publishers.

Decentralized systems allow for community-driven development and decision-making.

Innovation and customization

Limited ability for players to influence game development.

Greater potential for player-driven innovation, customization, and creation of mods and plugins.

Interoperability

Assets and progress are confined to a single game.

Potential for interoperability, where assets can be used across different games and platforms.

Fully on-chain games

Fully on-chain games are games where all aspects, including game assets, mechanics, and states, are stored on the blockchain. This means that everything in the game is decentralized and transparent, providing players with unparalleled control and security.

Storing all game data on the blockchain offers several benefits:

Transparency: Players can verify all transactions and game mechanics, ensuring fairness.

Security: Blockchain technology protects against hacks and data loss, making the game more secure.

Player control: Players have complete ownership and control over their in-game assets, which they can trade or sell freely.

An example of a fully on-chain game is Dark Forest, a real-time strategy game that uses zero-knowledge proofs (zkProofs) to create a “fog of war.” This ensures that players can keep their strategies confidential while maintaining transparency on the blockchain. This innovative approach demonstrates the potential of fully on-chain games to provide unique and secure gaming experiences.

The future of web3 gaming

Fully on-chain games have the potential to transform how players engage with, own, and control their gaming experiences.

By decentralizing game mechanics and assets, these web3 games ensure player sovereignty and foster community collaboration. The future of gaming could become more inclusive and democratic, where players have a meaningful say in game development and governance.

As blockchain technology advances, we can expect an exciting digital frontier that prioritizes transparency, security, and player empowerment. This shift promises to create richer, more immersive gaming worlds that truly reflect the desires and creativity of the gaming community.

Are web3 games the future of the gaming industry?

Web3 games have the potential to revolutionize the gaming industry by offering players true ownership of in-game assets through NFTs and blockchain technology. Unlike traditional games, web3 games allow players to trade, sell, and own their items, providing economic opportunities that were previously unavailable.

Platforms like Axie Infinity and Decentraland showcase the benefits of this new model, attracting a dedicated community of players and developers.

While still in the early stages, the growing interest and investment in web3 games, crypto games, and the metaverse indicate that they could play a significant role in the future of gaming.

As the technology matures and becomes more accessible, web3 games could set new standards for transparency, security, and player empowerment, potentially transforming the gaming industry into a more inclusive and decentralized space.

There are five key on-chain indicators that suggest a bullish outlook for the price of Bitcoin. With market dominance above 54% and miner revenue per hash still strong, the data points to more potential gains ahead.

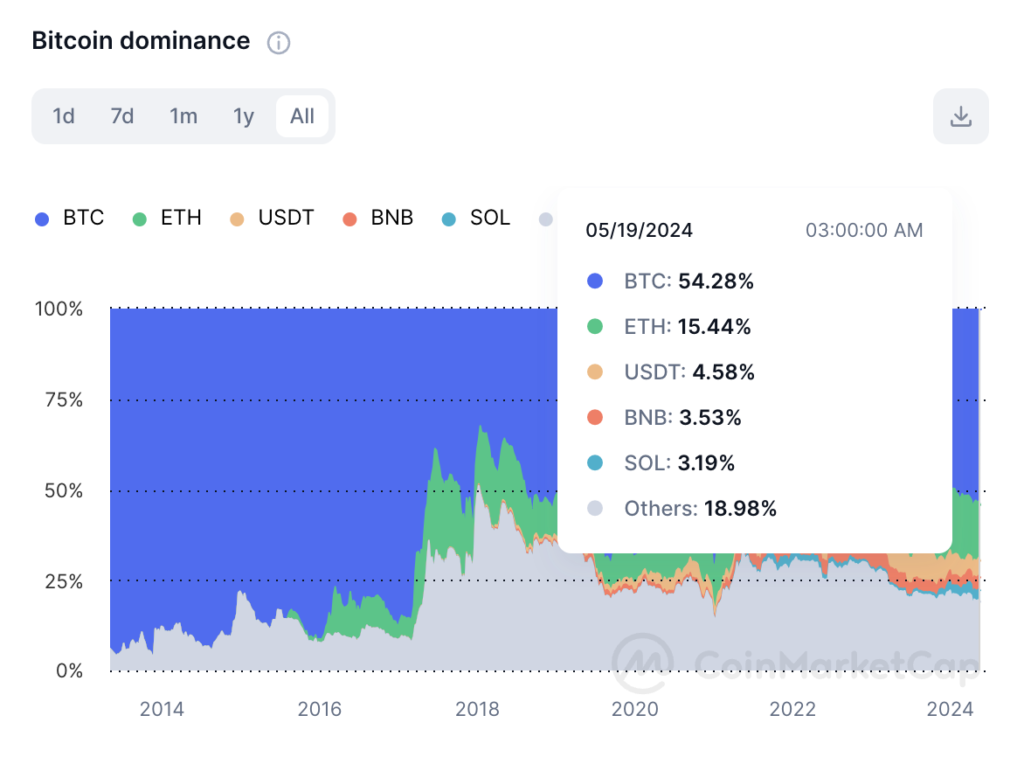

Bitcoin market dominance is above 56%

Historically, when Bitcoin (BTC) dominates the crypto market, it’s often a sign of a bull market. Traders typically sell their altcoins during bear markets, which increases Bitcoin’s market share.

Conversely, when Bitcoin’s dominance drops and the altcoin season begins, it indicates that the bull market is nearing its end.

As of May 2024, according to CoinMarketCap, Bitcoin’s dominance is still high at over 54%. Since October 2023, Bitcoin’s market share has remained above 50%.

Bitcoin’s market dominance and its correlation to a period of bull run

In mid-2015, after a prolonged bear market, Bitcoin’s dominance increased from around 40% to over 60%, which preceded the 2016-2017 bull run.

In 2017, Bitcoin’s dominance rose from 37% in January to 66% by June, before the famous bull run that culminated in Bitcoin reaching nearly $20,000 by December.

After the 2018 bear market, Bitcoin’s dominance grew from around 33% in January 2018 to over 70% by September 2019, preceding the 2020-2021 bull run.

During the market recovery in early 2019, Bitcoin’s dominance steadily climbed from around 50% in January to over 70% by September.

In late 2020, Bitcoin’s dominance surged above 50%, signalling the start of a major bull run that saw Bitcoin’s price rise from around $10,000 in September 2020 to over $60,000 by April 2021.

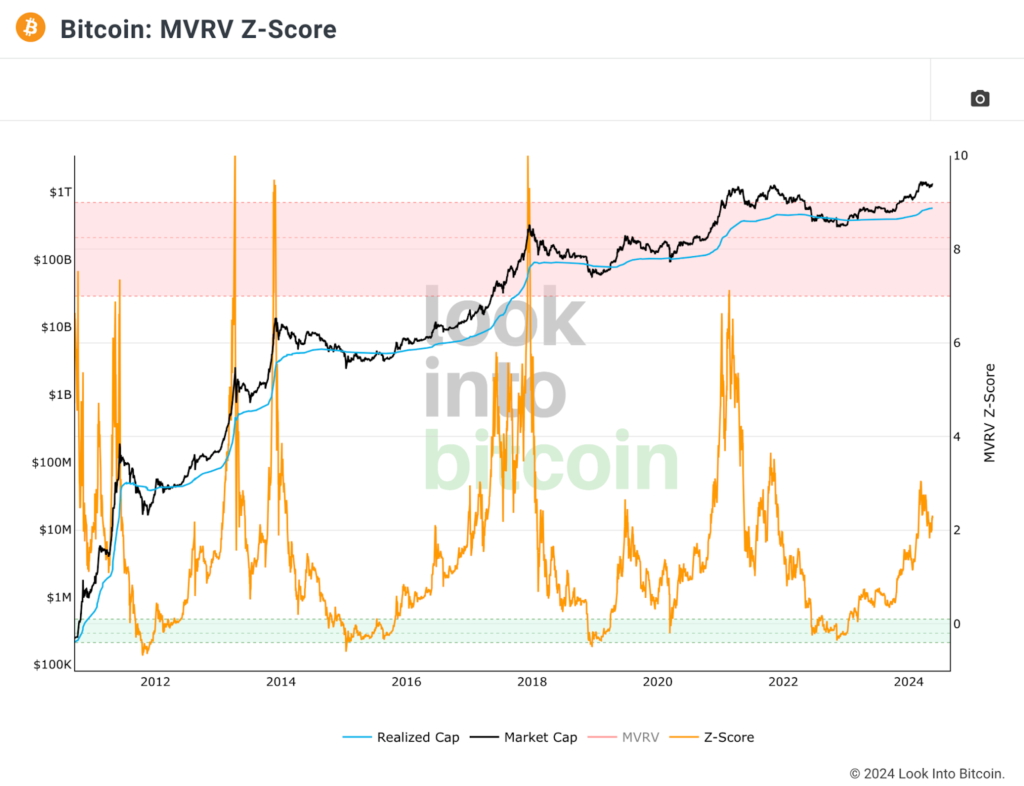

Bitcoin MVRV Z score under six

The Bitcoin Market Value to Realized Value (MVRV Z) score is a measure that compares Bitcoin’s current market value to its historical average.

This score tends to peak around six during market cycles. Currently, the MVRV Z score is below three and hasn’t exceeded six since March 2021, according to LookIntoBitcoin.

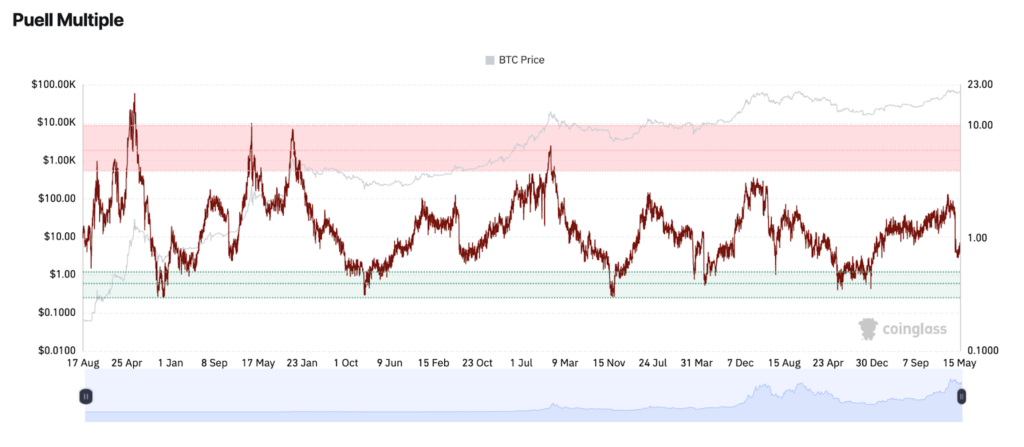

The Puell Multiple is another indicator used to identify market cycle peaks. It’s calculated by dividing the daily value of Bitcoin mined by the yearly moving average of that value.

According to Coinglass, the Puell Multiple fell below one after the halving on April 20. Peaks above three are usually seen at cycle tops, and the highest it reached during the 2024 price surge in mid-March was 2.4.

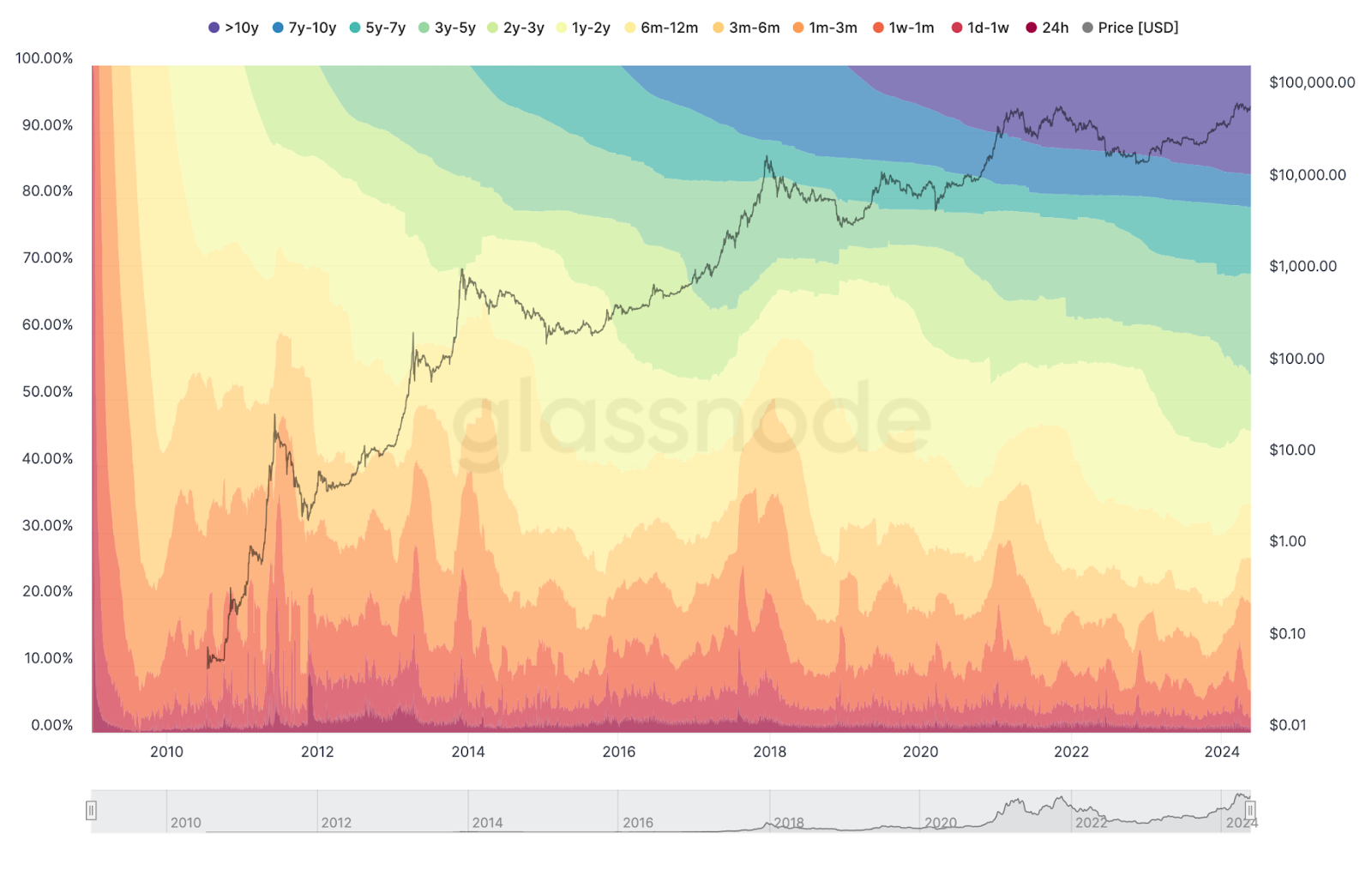

Charts that analyse the amount of Bitcoin held by different groups, known as hodl waves, also suggest a bullish outlook for Bitcoin.

Realized cap hodl waves provide insights into how much Bitcoin is held by recent buyers versus long-term holders. A decline in peaks among newer holders indicates that selling pressure might have lessened, potentially paving the way for further gains.

Source: Glassnode

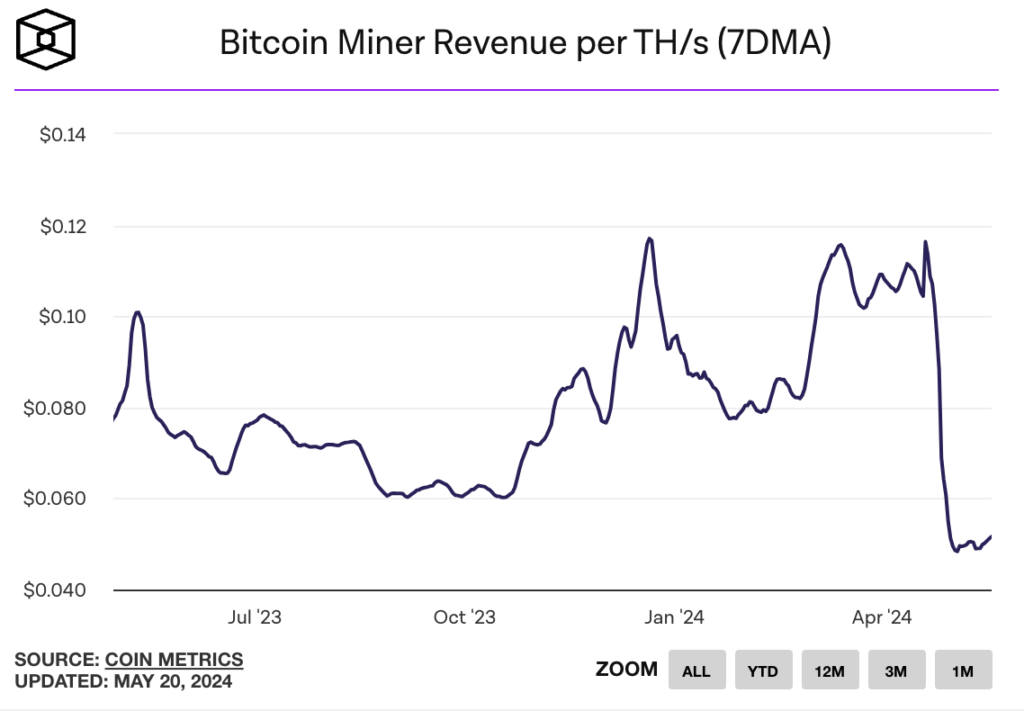

Bitcoin miner revenue per hash

Another bullish indicator is the miner revenue per hash, which tracks how much money Bitcoin miners earn.

A terahash (TH/s) is a unit of measurement used in cryptocurrency mining to indicate the speed at which a computer can process complex calculations. Specifically, it represents one trillion (1,000,000,000,000) hash calculations per second.

The higher the terahash rate, the more calculations a miner can perform, increasing the chances of successfully mining a block and earning rewards.

Although this metric tends to decline as network difficulty increases, past spikes to $0.3 per terahash have coincided with market peaks. Currently, it suggests miners are still profiting well.

Despite these bullish signals, some metrics suggest the market might be overheating. The Realized Hodl (RHODL) ratio compares the price of recently bought Bitcoin to that of Bitcoin bought one to two years ago.

If new buyers are paying significantly more than long-term holders, it could indicate a market peak. This ratio signalled a peak in March.

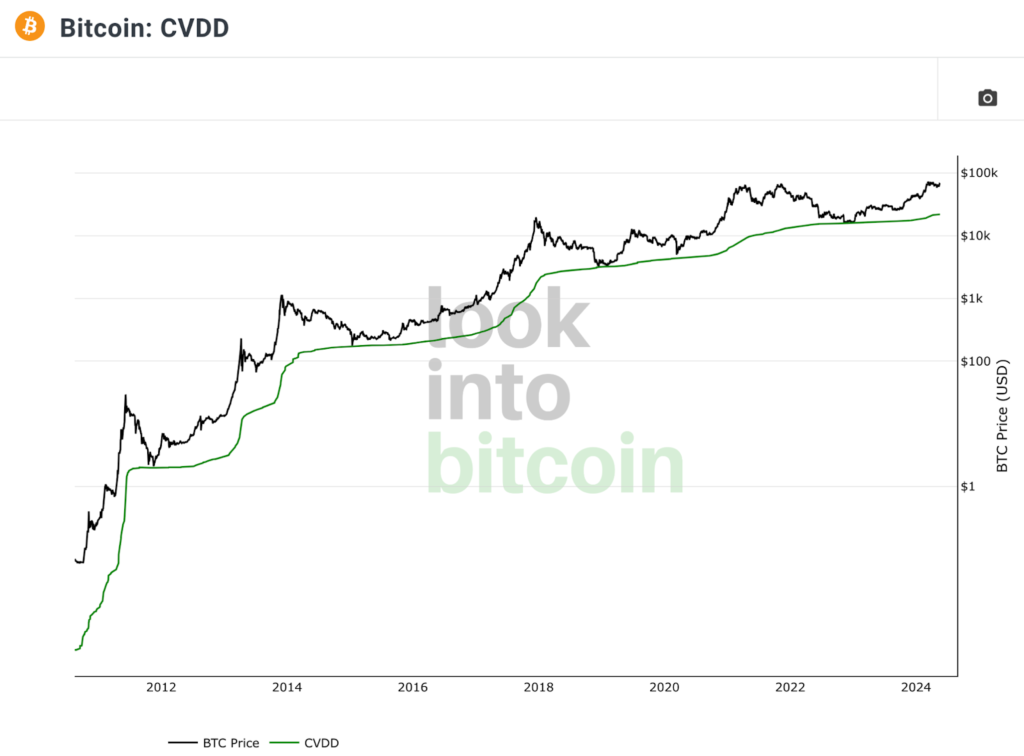

The Cumulative Value-Days Destroyed (CVDD) metric also appears to have peaked.

CVDD measures the cumulative value of Bitcoin moved from older hands to new hands relative to the market age. A sudden movement of old coins can signal a market peak.

Source: LookIntoBitcoin

What’s next for Bitcoin’s price?

Given the current on-chain indicators, it looks like Bitcoin’s price is set to continue rising. High market dominance, favourable MVRV Z score, Puell Multiple, hodl waves, and miner revenue all suggest a bullish trend.

Although some metrics hint at a potential market peak, the overall data indicates that Bitcoin’s price is likely to see further gains before any significant downturn.

Mastercard is integrating advanced technologies with major banking institutions to enhance cryptocurrency transactions and settlement systems. They are set to become a pivotal players in the evolving digital currency landscape.

Mastercard has teamed up with leading U.S. banks, including Citigroup, Visa, and JPMorgan, to explore a new way of handling settlements across different types of assets using a technology called a shared ledger.

This technology, known as the Regulated Settlement Network (RSN),allows for the tokenisation of assets like government bonds, high-quality debt, and bank-issued money, enabling them to be settled together on one platform.

Traditionally, these assets are handled through separate systems, but with RSN, they are converted into digital tokens and managed collectively on a single system.

This method aims to simplify the settlement process by using a distributed ledger—a type of database spread across several sites, countries, or institutions, ensuring secure and transparent transactions.

This initiative is part of a broader trial that began with a 12-week pilot in late 2022, initially focusing on cross-border and domestic dollar transactions between banks.

The first phase of Mastercard on a distributed ledger

The current phase is experimenting with simulating settlements in U.S. dollars to refine the process.

Mastercard’s recent announcement highlighted the potential benefits of this technology, such as enhanced efficiency in cross-border settlements and a reduction in errors and fraud risks.

Raj Dhamodharan, who leads Mastercard’s blockchain and digital assets efforts, emphasised that this approach could revolutionise market infrastructure by enabling around-the-clock, seamless settlements.

The RSN Proof of Concept (PoC) has been expanded with two notable additions: interbank tokenised deposit networks, featuring the USDF Consortium as a key participant and the Tassat Group as a contributor.

Additionally, the consulting giant Deloitte is providing advisory services. The Securities Industry and Financial Markets Association is overseeing the program.

There are ten major banking participants in the project: Citi, JPMorgan, Mastercard, Swift, TD Bank N.A., U.S. Bank, USDF, Wells Fargo, Visa, and Zions Bancorp.

Furthermore, six additional participants are contributing their specialized expertise, including the nonprofit MITRE Corporation, BNY Mellon, Broadridge, the DTCC, ISDA, and the Tassat Group.

Catalysing cryptocurrency adoption and utility

The collaboration between Visa and Transak, a Web3 infrastructure service, has garnered attention, particularly among crypto wallet users like those of MetaMask, Ledger, and Trust Wallet.

This partnership is significant as it simplifies the process of converting cryptocurrency into fiat currency.

Visa now allows crypto to be directly converted into local fiat at over 130 million merchant locations across 145 countries. This development is particularly notable because it supports around 40 types of cryptocurrencies.

The implications of this advancement extend beyond convenience for cryptocurrency users.

The involvement of Visa and Mastercard in the crypto sector signifies a crucial shift, potentially indicating a bullish trend for the market.

Despite previous hesitations, such as Visa’s reported step back from crypto partnerships last year, the current engagement suggests a strategic recalibration in response to positive market movements, such as rising Bitcoin prices and significant crypto events like Bitcoin halving.

Implications for Centralized and Decentralized Crypto Exchanges

This shift might pose a challenge to centralised crypto exchanges like Coinbase and Binance, as users now have the option to bypass these platforms for certain transactions.

However, the broader adoption of cryptocurrencies facilitated by Visa and Mastercard could benefit the entire industry, including decentralised finance (DeFi) and centralised exchanges (CEXs).

The role of CEXs remains crucial in ensuring the scalability, reliability, and security of crypto transactions.

The entry of major payment networks into crypto payments also addresses the ‘network effects’ barrier, where the utility of new forms of money increases as more people and merchants accept them.

By enabling real-time conversion of cryptocurrencies to fiat, Visa and similar entities are making cryptocurrencies a more practical medium of exchange.

However, this integration comes with trade-offs, particularly concerning the decentralisation and privacy aspects that are foundational to cryptocurrencies.

The involvement of traditional financial entities in crypto payments might dilute some of these core principles, although it could also lead to greater mainstream adoption and acceptance of cryptocurrencies as a part of everyday financial transactions.

The European Union’s research body delves into the possibilities of using the metaverse to enhance children’s health and education while also addressing the accompanying risks and challenges.

The European Parliamentary Research Service (EPRS), which is like a big brain for the European Union, recently wrote a letter talking about how kids can have good and bad things happen to them in the metaverse.

Maria Niestadt, who works at EPRS, says the metaverse can make kids more creative, help them learn, and maybe even make them feel better if they’re sick.

But there are also lots of problems to think about, like making sure kids don’t feel bad mentally or physically because of things like using special goggles or worrying about their privacy and safety.

What’s the metaverse?

The metaverse is like a big, virtual world where people can explore and do all sorts of things. It’s not just one place but a whole bunch of different digital spaces that connect to each other.

Imagine it like a huge playground where you can play games, chat with friends, go to school, or even work, all without leaving your computer or special goggles.

Advantages of the metaverse

Endless possibilities. In the metaverse, the only limit is your imagination. You can create and experience things that might not be possible in the real world, like flying through space or visiting ancient civilizations. Some metaverses even digital assets that can be seen as digital objects. They are called metaverse NFTs.

Connectivity. It brings people from all over the world together. You can meet new friends, attend events, or collaborate on projects, no matter where you are.

Accessibility. The metaverse is accessible to anyone with an internet connection, opening up opportunities for education, entertainment, and social interaction to a wider audience.

Innovation. Companies use the metaverse to develop new products and services, from virtual reality games to immersive training simulations for employees.

How to use the metaverse?

Socializing. People use the metaverse to hang out with friends, attend virtual parties, or join online communities based on shared interests.

Entertainment. Many use it for entertainment purposes, such as playing games, watching live performances, or exploring virtual museums and galleries.

Education. Schools and universities are increasingly using the metaverse for virtual classrooms, interactive learning experiences, and simulations that enhance traditional teaching methods.

Business. Companies utilize the metaverse for virtual meetings, conferences, and product demonstrations. It also serves as a platform for e-commerce, virtual advertising, and brand experiences.

The EPRS letter says there are lots of good things kids can do in the metaverse. It doesn’t say kids should always use special goggles, but it talks about some good ways they can use them.

Opportunities for children in the metaverse

The letter from EPRS talks about how the metaverse offers many opportunities for children.

While it doesn’t fully say that kids should always use virtual and mixed-reality headsets, it does highlight some positive ways they can be used.

According to EPRS, virtual worlds can help doctors find out and treat things like autism or ADHD in kids. They can also help kids exercise in a fun way and get over things like being scared of heights. Besides that, kids can learn about history and culture in virtual lessons and make friends in a safe way.

What are the challenges in the metaverse?

Although there are many opportunities in the metaverse, the EPRS also points out various challenges that need attention to keep EU children safe from the possible risks of metaverse technology.

Children often encounter similar risks in virtual worlds as adults do, but their vulnerability makes them more susceptible to harm. Reports, like the one from the Centre for Countering Digital Hate in 2023, show that minors are frequently subjected to different types of harassment, abuse, and content that isn’t suitable for their age in virtual environments.

The main concerns are about how being in digital worlds and using special equipment can affect kids’ minds and bodies. This includes things like feeling alone in real life, facing bullying or seeing things they shouldn’t do online, and even feeling sick or scared.

One big challenge is figuring out the right age for kids to use the metaverse. Right now, it’s up to the companies that make the special goggles. But sometimes, they lower the age limit. For example, in 2013, Meta made it okay for kids as young as 10 to use their Quest headsets, down from 13.

Overall, the metaverse in the European Union is changing a lot, and regulators are trying to find ways to make it safer. They’re counting on companies to follow the rules and make sure kids stay protected while using these technologies.

Metaverse opportunities

According to the letter, the metaverse is rife with opportunities for children. While it stops short of offering a full-throated endorsement for the use of virtual and mixed-reality headsets by children, the think tank lays out several claims for their positive use.

Per the EPRS:

“Virtual world technologies can be used to diagnose and treat various paediatric mental and physical health disorders (such as autism, attention-deficit/hyperactivity disorder). They can also be used to promote physical health through immersive fitness exercises, to help prepare children for psychological difficulties (such as the fear of heights) or to aid in their physical rehabilitation.”

Other opportunities include educational uses such as virtual immersion in lessons of historical and cultural significance and the potential for positive social interaction.

As Bitcoin goes through its 4th pivotal halving event, the landscape of cryptocurrency has transformed significantly. This new financial territory brings key changes and developments surrounding Bitcoin’s halving, from the unprecedented pre-halving price surges to the enhanced global decentralisation and security of its network

Bitcoin halving has catalysed a surge in crypto adoption

Since the Bitcoin halving event in May 2020, the number of people using cryptocurrencies worldwide has skyrocketed by at least 400%, growing from about 100 million to nearly 580 million users by the end of 2023.

This dramatic increase in user base is drawn from estimates by the Cambridge Centre for Alternative Finance and Crypto.com.

Although the rate at which new Bitcoins are generated has slowed down due to the halving process, global interest and adoption of cryptocurrencies have not decreased.

As of early 2024, data suggests that roughly 2.7% of the world’s population owns Bitcoin, amounting to about 219 million individuals.

This represents a significant rise—approximately 208%—from the 71 million Bitcoin users estimated four years earlier. It’s important to note, however, that these figures are estimates; accurately gauging the exact number of Bitcoin or other cryptocurrency users is challenging.

Factors like the inability of on-chain transaction analysis to distinguish between active users, long-term holders, and lost coins make precise counts difficult.

The 2024 pre-halving period has shown unprecedented growth in Bitcoin’s price, marking a distinct difference from the previous three halving events.

Historically, significant price surges in Bitcoin occurred after the halving, with new all-time highs typically forming about a year later.

For instance, before the 2020 halving, Bitcoin did not surpass its previous peak of $20,000. It only exceeded this mark 10 months post-halving.

However, the scenario has dramatically changed in the current cycle.

Bitcoin achieved a new all-time high just before the upcoming halving, hitting a record price of $73,600 on March 13, 2024. This kind of price action prior to a halving is unprecedented and has been noted by several analysts.

How Bitcoin miners are better positioned ahead of the 2024 halving

This time around, the unprecedented surge in Bitcoin’s price before the halving may have bolstered the mining industry, granting miners greater control over their operational costs.

Miners seem to be in better financial standing compared to previous halving cycles, with reduced debt levels and improved cost management, particularly in electricity expenses.

Moreover, the price appreciation preceding the halving is a novel occurrence in Bitcoin’s history, providing an additional boon to miners.

Since the third halving in May 2020, Bitcoin’s mining energy consumption has notably risen, reaching 99 Terawatt hours (Twh) by April 18, 2024. Despite this increase, there’s a positive trend in the utilisation of renewable energy sources for Bitcoin mining, accounting for 54.5% of the network’s energy consumption as of January 2024, up from 39% in September 2020, according to Bitcoin ESG Forecast and CCAF data, respectively.

The first Bitcoin halving with active spot ETFs in the U.S.

The 2024 Bitcoin halving stands out as the first to occur alongside active spot Bitcoin ETFs (exchange-traded funds) in the United States, marking a significant evolution in Bitcoin investment accessibility.

These ETFs, which began trading in January 2024, have opened the doors for institutional investors to engage more directly with Bitcoin.

Bloomberg’s ETF analyst, Eric Balchunas, reported that these spot Bitcoin ETFs have achieved “blockbuster success,” indicating a sharp rise in Bitcoin demand. Since their inception, the combined holdings of all ten spot Bitcoin ETFs have increased by at least 220,000 BTC, valued at approximately $14 billion.

Missed this earlier but looks like BlackRock and Pimco have filed for mutual fund to ETF conversions, joining about 70 funds so far with $100b to convert. MF cos looking to exploit all three roads to ETFville: clones, conversions and classes = bullish https://t.co/fqzMCG8cj5

Among these, BlackRock’s spot Bitcoin ETF has seen the most substantial inflows, with its holdings skyrocketing more than 10,000% from an initial 2,621 BTC to 273,140 BTC as of April 18.

As for the broader market dynamics, while the halving is significant, it should be viewed as part of a larger narrative that includes ETFs, quantitative easing, and other factors shaping the market’s future.

Bitcoin’s global decentralisation and enhanced security

Bitcoin’s network has seen substantial improvements in security and decentralisation over the past few years.

Previously concentrated primarily in mainland China, where nearly 80% of the mining activity took place as of 2020, the Bitcoin mining landscape has now become significantly more global.

As of February 2024, the United States leads with 40% of the total mining hash rate, followed by China and Russia, which contribute 15% and 12%, respectively, according to Hashlab Mining.

This shift toward geographic decentralisation continues as miners explore regions like Africa and Latin America, which are attracted by lower electricity costs.

Moreover, the security of the Bitcoin blockchain has dramatically increased; its hash rate has quintupled since the last halving, making the network much more robust against attacks.

Now, it requires five times more computing power and associated resources such as electricity, infrastructure, and hardware to pose a threat to the network.

Explore the intricate interplay between Bitcoin’s price movements, economic indicators, and trader behaviors in this detailed analysis.

As the cryptocurrency market approaches a pivotal moment with the upcoming Bitcoin halving, understand the factors influencing price trends, including leverage risks, regulatory impacts, and broader economic conditions.

Gain insights from expert predictions and strategies to better understand how global financial trends and internal crypto dynamics could shape the future of Bitcoin’s valuation.

Exploring the Link Between Bitcoin, S&P 500, and Economic Indicators

The relationship between Bitcoin‘s price movements, the S&P 500 index, and broader economic indicators is a complex interplay that reflects broader market sentiment and investor behaviour. This connection can be understood through several key dynamics:

Market sentiment and risk appetite

Bitcoin and the S&P 500 often react similarly to changes in global market sentiment.

During times of economic optimism, both markets tend to rise as investors are more willing to take on riskier assets. Conversely, economic downturns or market uncertainties often lead investors to pull back from both equities and cryptocurrencies, which are considered risk assets.

For example, significant drops in the S&P 500 due to economic fears or poor corporate earnings often coincide with declines in Bitcoin’s value as investors seek safer holdings.

Inflation and Monetary Policy

Bitcoin has been characterised by some investors as a “digital gold,” akin to a hedge against inflation.

The cryptocurrency’s limited supply contrasts with fiat currencies that can be printed without limit. When inflation fears rise, as indicated by economic indicators like CPI (Consumer Price Index), or when the Federal Reserve signals tighter monetary policy by raising interest rates, both the S&P 500 and Bitcoin can be affected. Stocks generally react negatively to high inflation and higher rates, which can also increase the appeal of Bitcoin as an alternative investment.

Liquidity and market dynamics

The Federal Reserve’s monetary policy also impacts liquidity in financial markets. Lower interest rates and quantitative easing generally increase market liquidity, making funds available for investment in both stocks and cryptocurrencies, leading to potential price increases in both markets.

Conversely, quantitative tightening reduces liquidity, which can lead to lower prices. Bitcoin’s reaction to these policies can be swift, mirroring or even exaggerating the movements seen in the S&P 500.

Investor behaviour and technological adoption

The increasing adoption of blockchain technology and the integration of cryptocurrencies into traditional finance (like Bitcoin ETFs and futures) further intertwine the performance of Bitcoin with traditional stock markets.

As institutional investors enter the crypto space, their investment behaviours — often driven by the same factors influencing their stock market investments — can lead to correlated movements between Bitcoin and the S&P 500.

Geopolitical and economic uncertainties

Global events such as geopolitical tensions, trade wars, or pandemics can influence both the stock market and Bitcoin prices.

For instance, during times of heightened uncertainty, there may be an increase in Bitcoin buying as a hedge against global instability, even as stock markets might falter due to risk aversion among traditional investors.

Understanding the nuanced relationship between Bitcoin, the S&P 500, and economic indicators not only helps in assessing the risk and opportunities inherent in both markets but also in strategizing investments that can withstand or capitalize on the interconnected volatility of these asset classes.

Trading crypto during this turbulent period

During this turbulent period in the crypto market, traders are expressing a mix of caution and strategic optimism. Here’s a snapshot of the prevailing sentiments and strategies among traders:

Caution over leverage. The recent liquidations of leveraged positions have served as a stark reminder of the risks involved. Traders are advising against over-leveraging and are emphasising the importance of risk management to withstand sudden price swings.

Don’t use leverage – at least not without a stop loss.

Using leverage is the only way to send your portfolio to 0, and to then miss out on the rest of the bull market.

If you are trading spot you’re down. So what. If you get liquidated you’re out of the game entirely.…

Market volatility. The unpredictable movements make it essential for traders to stay very active and responsive, adjusting their positions as the market changes.

Strategic patience. Experienced traders are advocating for a more cautious approach, suggesting that sitting out the high volatility might be wise. They believe that waiting for clearer signs or more stable conditions could prevent losses and lead to better opportunities in the future.

Market will go through a big shakeout.

Majority of alts are already down 40%-45% from their recent highs.

They'll most likely get to 50%-70% retracements across the board by the time we're done.

Optimism for post-halving gains. There is a strong sense of optimism regarding the upcoming Bitcoin halving. Some traders, like Andrew Kang of Mechanism Capital, predict that the reduced supply of Bitcoin resulting from the halving will lead to significant price increases, potentially reaching new all-time highs.

Diversification. With the current uncertainties, some traders are looking at diversifying their investments beyond just Bitcoin and Ethereum. They are exploring other cryptocurrencies and blockchain projects that might offer better stability or growth potential in the current environment.

Economic indicators. Traders are closely monitoring broader economic indicators, especially inflation rates and actions by the Federal Reserve, as these factors are seen as key drivers for both the stock market and cryptocurrency prices. Their strategies often involve adapting quickly to economic news that could affect market sentiment.

The second scenario, the impulsive wave: is that we roll over here and we are in the midst of a 5 wave impulsive move down, either way there's so much liquidity being formulated below is would seem pretty unlikely to me that we would not unlock all that liquidity from stop losses… pic.twitter.com/UCQr9iuNUh

As we navigate through a period of significant volatility and anticipation in the crypto market, various traders and analysts have shared their expectations for Bitcoin’s future. These insights combine optimism with caution, reflecting the complex factors influencing the market.

Post-halving surge

The upcoming Bitcoin halving is a focal point of discussion. Andrew Kang of Mechanism Capital is notably optimistic, predicting that Bitcoin’s price could ascend to new all-time highs, potentially reaching $80,000 by May. This optimism is grounded in Bitcoin’s historical performance following previous halvings, where reduced supply typically led to price increases due to the heightened scarcity of available coins.

Whale activities and market impact

The activity of Bitcoin whales—large holders capable of influencing market dynamics through substantial transactions—is also a key indicator to watch. Recent data suggest that whales are accumulating Bitcoin, possibly in anticipation of price increases post-halving. This trend could provide upward pressure on prices if it continues, signaling strong demand overcoming the reduced supply.

Economic indicators and external influences

Economic announcements, particularly regarding inflation and Federal Reserve policies, have recently impacted Bitcoin’s price.

Traders should continue to monitor these indicators as they provide a critical context for Bitcoin’s behaviour in relation to broader financial markets.

For instance, if inflation remains high, Bitcoin may increasingly be viewed as a hedge, similar to gold, which could boost its price further.

Volatility and trader behaviour

Despite the optimistic projections, seasoned traders like Honeybadger express a more cautious stance, suggesting potential price volatility could lead to unexpected market movements. This sentiment is echoed by others who advise against over-leverage and recommend waiting for more stable market conditions to avoid the risks of sudden price reversals.

Long-term trends

Looking further ahead, the integration of blockchain technology and broader financial acceptance of cryptocurrencies may bolster Bitcoin’s position as a mainstream asset. This could lead to greater stability and less susceptibility to sharp market movements compared to the current landscape.