In a groundbreaking development, a judge ruled that XRP is not considered a security in the Securities and Exchange Commission’s (SEC) case against Ripple. This ruling has significant implications for the future of XRP and the broader crypto industry.

On July 13, 2023, Ripple Labs won against the SEC, and XRP was declared to not be a security.

The company achieved a notable win in the United States District Court in the Southern District of New York when Judge Analisa Torres issued a partial ruling in favor of the company. This ruling pertained to a case brought against Ripple by the Securities and Exchange Commission (SEC) that dates back to 2020.

It’s official, Ripple’s token (XRP)is not a security

Based on documents filed on July 13th, Judge Torres granted summary judgment in favor of Ripple Labs.

The ruling clarified that the XRP token should not be considered a security, specifically in relation to its programmatic sales on digital asset exchanges.

However, the SEC also secured a victory of its own as the federal judge determined that XRP qualified as a security when sold to institutional investors. This classification was based on the conditions outlined in the Howey Test.

The SEC’s lawsuit aimed to compel Ripple to cease offering its XRP token, arguing that it qualified as a security and, therefore, required additional regulatory measures.

According to court documents, the motion for summary judgment by the defendants has been granted for Programmatic Sales, Other Distributions, and the sales made by Larsen and Garlinghouse. However, it has been denied for Institutional Sales.

This means that the XRP token is not considered a security when sold through retail digital asset exchanges.

After this news broke, the price of XRP surged from $0.45 to $0.61 within a few minutes.

The legal case against Ripple began in December 2020 when the Securities and Exchange Commission (SEC) filed a lawsuit against Ripple and its two top executives, Brad Garlinghouse and Chris Larsen.

The SEC alleged that the company was offering an unregistered security.

Throughout the past three years, the case has been filled with dramatic twists, including the release of the “Hinman Documents” and Garlinghouse’s ongoing defiance in response to the SEC’s accusations.

In addition to the noticeable price movement of the XRP token following this news, the general sentiment within the cryptocurrency community seems to be one of celebration and joy.

XRP’s non-security status

Ripple CEO Brad Garlinghouse is confident that the United States Securities and Exchange Commission (SEC) will face a lengthy process before being able to appeal the recent ruling in its case against Ripple Labs.

During an interview with Bloomberg on July 15, Garlinghouse downplayed the significance of the ruling regarding institutional sales, referring to it as “the smallest piece” of the overall lawsuit. He expressed his belief that if the SEC were to appeal the ruling on retail sales, it would only serve to reinforce Judge Torres’ decision.

Despite acknowledging that it may take a considerable amount of time before the SEC can file an appeal, Garlinghouse firmly stated his belief in the current legal status of XRP: “Based on the current law of the land, XRP is not classified as a security. Given the lengthy process required for the SEC to file an appeal, which could take years, we maintain a high level of optimism.”

Garlinghouse emphasized that this marks the first instance where the SEC has faced a setback in a “crypto case.” He openly criticized the SEC, referring to them as “bullies” who target players in the crypto industry unable to mount a strong defense.

We said in Dec 2020 that we were on the right side of the law, and will be on the right side of history. Thankful to everyone who helped us get to today’s decision – one that is for all crypto innovation in the US. More to come.

He highlighted the initial response of various U.S. crypto exchanges when the lawsuit against Ripple was initially filed.

Many took a cautious approach, waiting to observe the outcome due to the uncertainty surrounding the case. Consequently, exchanges such as Coinbase and Kraken decided to delist XRP entirely.

Garlinghouse accused the SEC of deliberately creating confusion in the market. He claimed that the SEC was aware of the existing confusion and intentionally engaged in actions that further exacerbated the situation.

According to Garlinghouse, this deliberate confusion was a means for the SEC to exert its power, hindering innovation within the United States. He criticized the SEC for prioritizing power and politics over the establishment of clear regulatory frameworks, resulting in difficulties for entrepreneurs and investors seeking to participate in the U.S. crypto market and blockchain industry.

BlackRock Bitcoin ETF seeks SEC approval.Are Bitcoin ETFs the way to mass adoption? Or is traditional finance trying to profit from this new asset?

Bitcoin fans got excited when the news that BlackRock is applying for a Bitcoin-based fund got out. They think it could mean a big change in how the government regulates these things. They also believe it could make Bitcoin more accessible to everyone.

While there might be some truth to these ideas, we should take a step back and see the bigger picture. It’s not good that the simple chance of a Bitcoin-based fund being approved in the US can send the market crazy. The fact that BlackRock could have such a big effect on the price of Bitcoin should make us all think, not celebrate.

A Bitcoin-based fund would be an easy way for US retirement funds to benefit from Bitcoin’s potential growth. It’s also likely that if such a fund is approved in the US, it could lead to a big increase in Bitcoin’s price in the following years. But what about Bitcoin’s main goal – to become an alternative to the traditional financial system?

A Bitcoin-based fund wouldn’t do much to help with these things.

The BlackRock Bitcoin ETF

Recently, there’s been a lot of focus on applications for Bitcoin-based funds. Following BlackRock, a company that manages $10 trillion worth of assets, other firms like Fidelity, Invesco, Wisdom Tree, and Valkyrie have also applied for approval from the SEC.

If the SEC ends up approving the applications from big players like JPMorgan, Morgan Stanley, Goldman Sachs, BNY Mellon, and Bank of America who want to offer similar services, the digital currency market could open up to firms managing a total of $27 trillion in assets. As we wait for a decision on Grayscale’s application, GBTC, its Bitcoin trust, has seen its price increase by over 134% in 2023, reaching $19.47.

However, the United States may see a delay in the introduction of a Bitcoin exchange-traded fund (ETF) as the SEC has labeled recent applications by investment managers as insufficient.

According to The Wall Street Journal, the SEC found the filings by the Nasdaq and Chicago Board Options Exchange unclear and incomplete. The SEC expected them to specify a “surveillance-sharing agreement” with a Bitcoin exchange or provide enough details about these arrangements.

BlackRock’s Bitcoin ETF application included a “surveillance sharing agreement” to avoid market manipulation, leading others like ARK Invest and 21Shares to modify their applications similarly.

Other companies like Invesco, WisdomTree, Valkyrie, and Fidelity have also refiled or amended their applications. Notably, ARK Invest is considered a front-runner in this process.

Bitcoin ETFs have been continuously rejected by the SEC since 2017. However, such financial products are already available in Canada, with funds like Purpose Bitcoin, 3iQ CoinShares, and CI Galaxy Bitcoin directly investing in Bitcoin.

BlackRock ETF’s application re-submitted

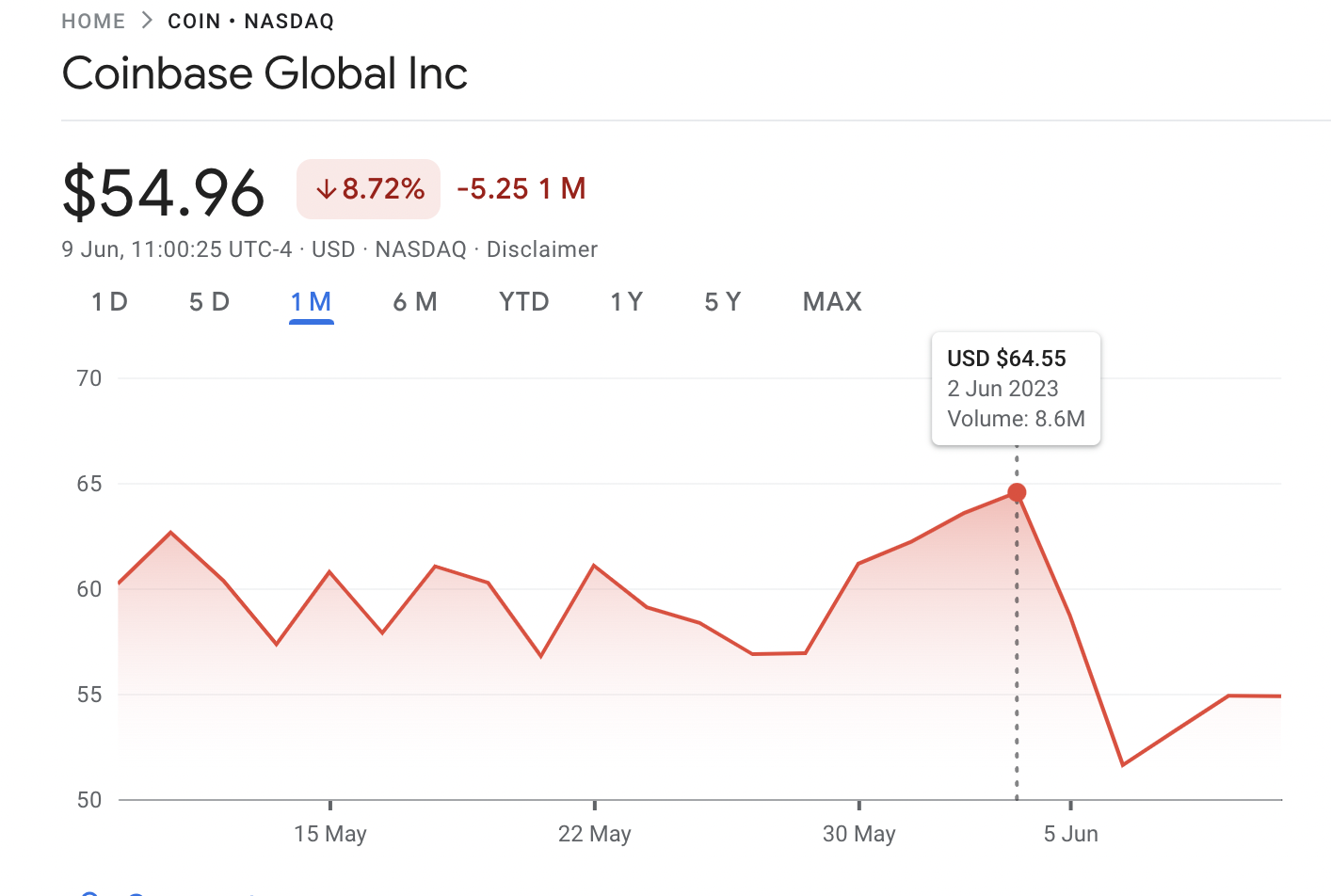

Nasdaq has resubmitted its application to list BlackRock’s proposed Bitcoin ETF, and has named Coinbase as the exchange to be monitored under a surveillance-sharing agreement.

This move follows feedback from U.S. regulators and aims to prevent market manipulation.

Other applications, including one from Fidelity, have also been updated to name Coinbase as the surveillance partner.

The Nasdaq reached an agreement with Coinbase on June 8, according to the new filing. The filing also indicates that Coinbase accounted for about 56% of the dollar-to-Bitcoin trading on U.S.-based platforms so far this year.

The SEC has historically rejected attempts to launch a Bitcoin spot ETF, but money managers are still trying. The news has positively affected Coinbase shares.

Traditional finance wants to take its share of crypto trading

The application from BlackRock and all the talk around it have really highlighted the mistrust that some people in the crypto world have toward traditional finance.

The timing of BlackRock’s move into Bitcoin funds is pretty interesting and has set off a bunch of conspiracy theories. Since the US Securities and Exchange Commission (SEC) has taken legal action against Binance and Coinbase, some think the government is trying to push aside crypto-focused companies to make way for traditional firms like BlackRock to lead in the crypto industry.

Whatever the reason is, the risk right now is that Bitcoin will turn into another type of investment.

These are the key dates and timeline for the BlackRock Spot Bitcoin ETF

Looking more closely at BlackRock’s application, more warning signs start to appear. The application includes a clause stating that in case of a major change or ‘hard fork’ in Bitcoin, BlackRock can decide which version of Bitcoin the fund should use. This could be a big deal because it means BlackRock could have a say in Bitcoin’s future or at least guide where big businesses and the general public put their money.

Having such a strong influence over what’s supposed to be a decentralized money system is obviously a problem. But, there’s another issue with these funds. Investors don’t actually get to own the Bitcoin their investment is based on. And owning Bitcoin is where the real benefits are.

Conflicting interests in Bitcoin-based funds

Bitcoin was created as a direct reaction to the financial aid and money-printing that happened after the 2008 financial crisis. Unlike regular money, there’s only a limited amount of Bitcoin. It’s truly rare and managed in a decentralized way.

Fifteen years after the crisis, central banks all over the world are still printing money as if it’s a free pass.

But it’s anything but free. Regular, hardworking people all over the world pay the price as the value of their money goes down, a problem that’s getting worse due to high, lasting inflation.

While central banks take risky gambles with public money, Bitcoin’s aim is to give power to individuals by providing a type of money that can’t be censored and works everywhere. As an open-source money network, Bitcoin has the potential to change the way we use money. It could even make centralized institutions much less important or not needed at all – something traditional finance likely knows all too well.

Bitcoin-based funds seem to go against this empowering philosophy.

El Salvador, with its revolutionary approach to adopting Bitcoin, arguably aligns more with Bitcoin’s main goals than any fund ever could.

While El Salvador is working to give power to people without banks by actively promoting Bitcoin ownership, investors in Bitcoin-based funds won’t get any of the benefits of Bitcoin.

Instead, they’ll fill the pockets of – and strengthen the position of – traditional finance institutions.

Potential risks of Bitcoin-based funds

Bitcoin-based funds are likely to become more common in the crypto world and appeal to a certain type of investor in the coming years. But their role shouldn’t distract us from Bitcoin’s long-term future.

If we only focus on letting people benefit from price changes without actually owning any Bitcoin, then we’ve completely missed the point of what could be a groundbreaking money system.

And no, if a rule is ever suggested that forces regular people to invest only through funds and not by owning Bitcoin directly, that’s not “protecting consumers.” It’s taking power away from them.

We in the crypto industry should be cautious, recognizing that the growing involvement of funds and traditional finance in the crypto world could threaten Bitcoin’s core purpose.

Being aware of these threats means not getting carried away by all the excitement but staying true to Bitcoin’s original goal – to change the world’s financial systems, not just to be an asset for gambling on price changes.

After recently suing Binance, the SEC now targets Coinbase for allegedly operating as an unregistered securities exchange, adding to regulatory scrutiny in the crypto industry.

The U.S. government’s finance watchdog, the Securities and Exchange Commission (SEC), is suing Coinbase. Coinbase is a big company in New York that trades cryptocurrencies like Bitcoin.

The SEC says that Coinbase should have registered as a broker, national securities exchange, or clearing agency, but they didn’t.

This registration helps keep trading fair and transparent.

Also, the SEC claims that Coinbase has been selling certain cryptocurrencies that it shouldn’t have. These include Solana, Cardano, Polygon, Filecoin, The Sandbox, Axie Infinity, Chiliz, Flow, Internet Computer, Near, Voyager Token, Dash, and Nexo. According to the SEC, these count as securities, and you need special permission to sell them.

Today we charged Coinbase, Inc. with operating its crypto asset trading platform as an unregistered national securities exchange, broker, and clearing agency and for failing to register the offer and sale of its crypto asset staking-as-a-service program.https://t.co/XPG2gDkxtVpic.twitter.com/hCdVMw8B2v

— U.S. Securities and Exchange Commission (@SECGov) June 6, 2023

The lawsuit also says that Coinbase has been working like a broker for securities since 2019 without the needed registration. This is two years before they first started offering public shares in April 2021.

The SEC says that Coinbase’s staking program is also a problem. This program involves five different cryptocurrencies. According to the SEC, this makes the staking program an investment deal and counts as a security. Coinbase has been arguing with the SEC about this, saying its staking products are not securities. They keep arguing even though Kraken, another crypto company, settled with the SEC and stopped offering staking services in the U.S.

Gary Gensler, the head of the SEC, spoke about the lawsuit against Coinbase. He said Coinbase had not given its customers enough protection against scams and manipulation. They’ve also not been open about conflicts of interest. Gurbir Grewal, who is in charge of enforcing SEC rules, said that Coinbase knew they were breaking federal securities laws, but they did it anyway.

After the SEC announced its lawsuit on June 6, the price of Coinbase’s shares fell by 15% before trading started.

The SEC’s lawsuit against Coinbase happened just one day after they also sued Binance. Binance is another crypto company that the SEC accuses of breaking securities laws and mixing up customers’ money. Binance is in trouble for breaking 13 different securities laws.

The U.S. Securities and Exchange Commission (SEC) has charged Binance, the world’s largest crypto exchange, and its founder, Changpeng Zhao. They’re accused of mixing up billions in user funds and sending them to a Zhao-controlled company in Europe.

The SEC says Zhao and Binance dodged their own rules to let rich U.S. investors keep trading on Binance’s unregulated international platform. It’s even claimed that an executive admitted the company acted as an unlicensed securities exchange in the U.S.

The lawsuit also suggests that Binance.US was created to protect Binance and Zhao from legal issues. Two former Binance.US CEOs, likely Catherine Coley and Brian Brooks, raised concerns about Zhao’s control over the company.

Between 2018 and 2021, Binance made $11.6 billion, mostly from transaction fees. The SEC claims that Binance knowingly had many U.S. customers and didn’t act, even though it’s against federal law to offer and sell unregistered securities. Binance’s compliance efforts in 2019 were mostly for show, according to the SEC.

Lastly, the SEC accuses Zhao of setting up a plan to help rich customers evade regulations using a VPN service to hide their location and fake compliance documents to cover their tracks.

Coinbase is a publicly traded company

But people in the crypto industry are confused about the lawsuit against Coinbase. This is mainly because Coinbase is a company that has publicly traded shares.

Binance’s boss, Changpeng Zhao, responded to the lawsuit against Coinbase by teasing the SEC.

If you have to pick a fight with everyone, maybe you are the one at fault. 🤷♂️

Paul Grewal, the top lawyer at Coinbase, said that the SEC’s focus on punishing rather than setting clear rules for digital assets is bad for U.S. business. He said we need new laws that create fair and clear rules for everyone instead of lawsuits. But for now, Coinbase will keep doing business as usual.

“The solution is legislation that allows fair rules for the road to be developed transparently and applied equally, not litigation. In the meantime, we’ll continue to operate our business as usual.”

A lot of people in the crypto community are wondering how Coinbase could have gone public in 2021 if it was acting like an unregistered securities broker.

Payment apps may lack protection: A recent warning from the US Consumer Financial Protection Bureau emphasizes that the FDIC might not protect money stored in mobile payment apps. Customers could be concerned about whether their funds are insured, highlighting the risks associated with these platforms.

The US Consumer Financial Protection Bureau (CFPB) has advised Americans to keep their money in a secure, insured bank account rather than in an unprotected app.

The Bureau expressed concern over the growing use of peer-to-peer payment apps, which also handle cryptocurrency transactions, due to the increased risk of losing money if things go wrong.

The public has become more aware of the protection offered by the Federal Deposit Insurance Corporation (FDIC). This comes after the failure of several cryptocurrency platforms and a banking crisis that resulted in the loss of a huge amount of customer money.

Despite this, the CFPB warns that a lot of money is still being held in these payment apps, which aren’t covered by the FDIC.

Payment services don’t offer insurance for your funds

The CFPB says that many peer-to-peer apps like PayPal, Venmo, Cash App, Apple Pay, and Google Pay have features that work much like bank accounts, although Meta Pay doesn’t have that feature.

The companies behind these apps actually like it when you keep your money in their apps because they can then use your money for their own investments (within legal limits), while they hardly ever pay you any interest on the money you store. However, there is a risk involved for these companies, as they could potentially lose money on the investments they make.

The CFPB explains that if your money is in an FDIC-insured account and something goes wrong, whether you’re covered by their insurance is only decided after the fact.

Plus, the insurance only covers the bank’s failure. It doesn’t cover the failure of the payment app, which is usually controlled by state laws and not watched over by the federal government. Most of the time, these state laws are meant for transferring money, not storing it.

So, if you have money in PayPal or Venmo, it could be protected by this pass-through insurance when it’s in their partner banks, but not if they’ve used your money for investments. Also, it might not be clear to you where your money is actually kept.

More and more, these mobile payment services are letting you handle cryptocurrencies. But remember, payment apps may lack protection and cryptocurrencies aren’t insured, even though services like PayPal and Venmo let you keep crypto in your accounts.

In October 2022, the EU published a report to describe the risks of crypto assets investments.

According to the report. “The pseudonymity that prevails in crypto-asset markets makes it virtually impossible to assess the creditworthiness or aggregate exposures of participants.” The paper also talks about the leverage offered by crypto exchanges to individual investors, which can raise up to 125x.

While some jurisdictions try to adopt regulations to protect investors (e.g., MiCA), these regulations often fall short in the face of the ever-expanding crypto industry.

All in all, keeping your crypto investments is a very risky business, and you should be aware of the risks.

Why aren’t crypto insurance policies good enough yet?

Insurance companies still need to improve their crypto insurance plans. Right now, these plans don’t cover everything. To fully protect all your crypto assets, you might have to combine different plans. One might cover the loss of your private key, another might cover errors in smart contracts, and you might need a third in case your wallet company goes under.

What are the risks of investing in cryptocurrencies?

Cryptocurrencies are pretty risky. Their prices can go up and down much more than things like stocks. Future prices could also be impacted by changes in laws, which might even make cryptocurrencies worthless. Plus, cryptocurrencies are always at risk from cyber threats like hacking and theft.

Are cryptocurrencies insured by the FDIC?

No, they’re not. The FDIC insures normal bank accounts up to $250,000, but it doesn’t protect cryptocurrencies at all. If you’re not from the US, you should check your country’s financial authority and see their conditions for insured investments and their limitations.

Can I get insurance for my cryptocurrency investments?

Yes, you can get insurance that offers limited protection against cryptocurrency theft. But these policies often only cover specific situations. They generally don’t protect you against losses due to market changes, hardware damage or loss, sending cryptocurrency to someone else, or problems with the blockchain technology that supports the asset. If you want more comprehensive coverage, you’ll probably need to buy multiple policies.

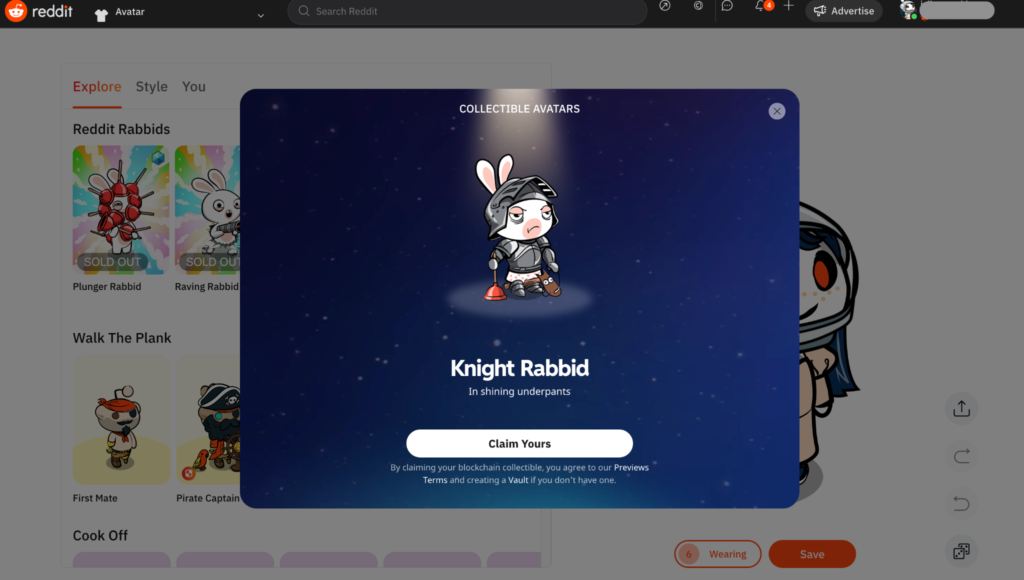

Revolutionizing the crypto and NFT landscape, Reddit’s unique collectible avatars are on the brink of reaching a staggering 10 million users.

Reddit, a social media site, is nearly hitting 10 million users who have its special profile pictures, called “Reddit NFTs.” These were introduced in July 2022, so it’s been about 11 months.

Right now, data from Dune Analytics shows that there are about 9.9 million people who have these special profile pictures. Among these, around 7.7 million users only have one of these special profile pictures and do not have them in several accounts.

In simple words, Reddit started a marketplace for special profile pictures on the Polygon blockchain in July 2022. These pictures, known as NFTs, were made by independent artists and people who create content on Reddit.

After the marketplace started, the number of people having these pictures grew quickly but then slowed down to about 3 million by November. However, there was a big increase in 2023, with the number of accounts holding these pictures tripling in the last six months.

From the start of 2023, the number of people with these special Reddit pictures has grown by 80%. The total value of the special profile pictures market is $38.4 million, and there are 13.7 million of these pictures.

Also, there have been over 303,033 sales totaling up to $32.6 million, according to the data from Dune Analytics.

In May 2023, a Reddit user named “ContextMelodic4212” praised Reddit for its success but also pointed out that some of the growth might be because of bots.

According to this Reddit user, there are some problems with people using bots to grab or ‘scoop up’ these avatars quickly. “However, I can’t think of a better use case for this technology!”

On May 26, 2023, Reddit said it will now support the Rabbids NFT collection from the big video game company, Ubisoft. Reddit users can get these Rabbids NFT pictures for their profiles for free, and people are grabbing them really quickly.

Rabbids first appeared as part of a different video game, the 2006 game “Rayman Raving Rabbids.” Ubisoft, the company that made these games, was the first big video game company to create NFT items within their games in December 2021. They made a collection of Rabbids NFT pictures for a virtual reality game called The Sandbox in February.

During a Q&A session with the India section of Reddit on May 25, Sandeep Nailwal, who helped start Polygon, said he really likes Reddit NFTs. He said that Reddit is maybe the only big tech company that has figured out how to use NFTs well, and they’ve been able to get a lot of people interested in Reddit NFTs.

He also suggested that Reddit could improve its NFTs by having a secondary marketplace and a place for artists to launch their work. He thinks these changes could make Reddit’s NFTs even better.

CryptoSnoo NFT from Reddit

But Reddit already had its own NFTs, which were launched in the summer of 2021.

CryptoSnoo are a collection of NFTs from Reddit that features the popular Snoo mascot in different contexts.

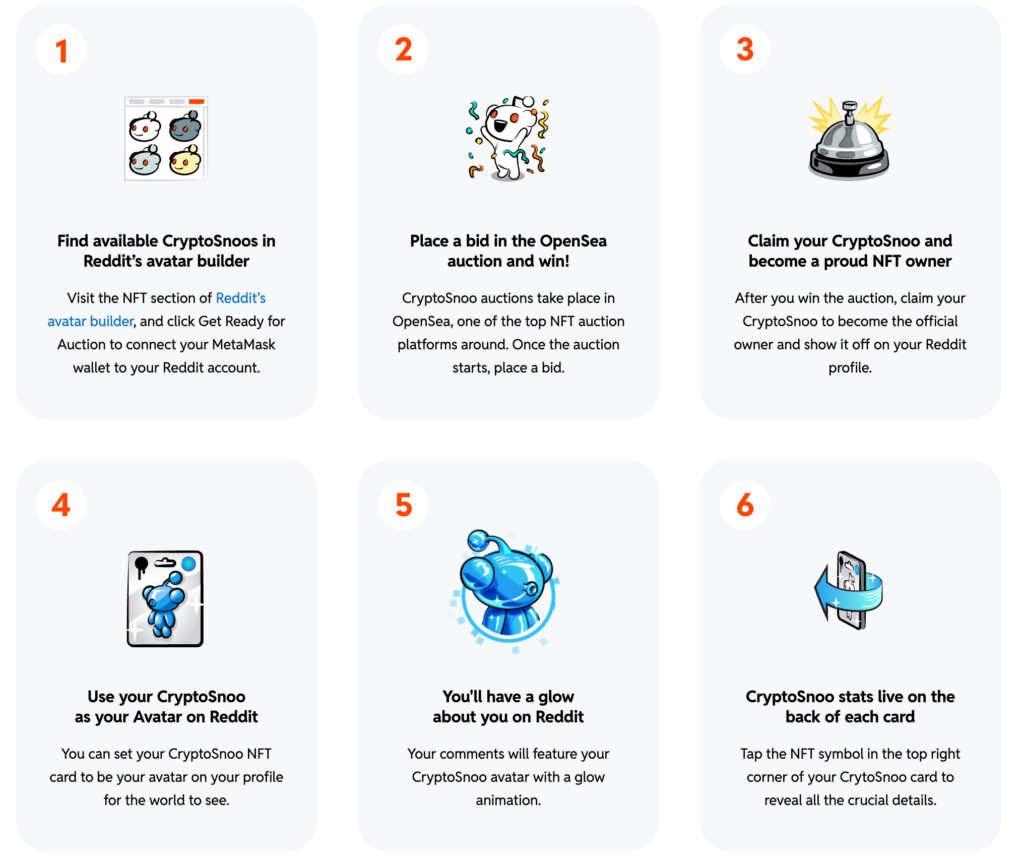

CryptoSnoos are unique cartoon avatars that take the form of the Reddit logo. These are created as non-fungible tokens (NFTs), which means they are unique digital items stored on the Ethereum blockchain. Two years ago, in June 2021, Reddit started an experiment to auction off these special avatars.

Since the Reddit NFTs were well received, the users of the popular platform can still claim their CryptoSnoos.

Three CryptoSnoos named “Original Block,” “Helium,” and “Snoopermatic” were created on June 17, 2021. These NFTs are based on the original Reddit logo that Alexis Ohanian, Reddit’s co-founder, designed in 2005. Reddit put them up for auction on OpenSea.

CryptoSnoos come in three categories: “Legendary” which means they are one of a kind, “Rare” which means there are very few of them, and “Epic” which means they are limited edition. Reddit users can find these available CryptoSnoos in Reddit’s avatar builder.

But buying an NFT from the CryptoSnoo collection doesn’t mean you own the artwork it represents. Reddit’s rules state that these NFTs are only for fun, and you don’t get any commercial rights to the artwork. Also, Reddit has the power to take away your rights to the CryptoSnoo if you say bad things about Reddit or take any legal action against them.

So, while CryptoSnoos might seem like a fun way to own a piece of Reddit history, potential buyers should understand what they are getting into before buying.

A malicious actor recently exploited Tornado Cash’s governance, enabling them to seize total control. This could potentially allow them to retrieve all the secured votes, empty the tokens held in the governance contract, and disable the router.

Tornado Cash, a decentralized crypto mixer, has faced another setback due to this incident. An attacker cunningly secured full control over the platform’s governance via a devious proposal.

The incident occurred on May 20 at 3:25 ET, when the attacker successfully attributed 1.2 million votes to a nefarious proposal. The proposal had already amassed over 700,000 valid votes, thus enabling the attacker to monopolize Tornado Cash‘s governance.

How was Tornado Cash’s governance exploited?

The disclosure was provided by @samczsun, affiliated with Paradigm, a research-oriented technology investment firm. He exposed the attacker’s claim that the malicious proposal utilized a similar logic to one that the community had previously accepted. Yet, this particular proposal contained an added function.

According to @samczsun, Tornado Cash’s governance was essentially annihilated on 2023/05/20 at 07:25:11 UTC. Through a crafty proposal, the attacker allotted themselves 1,200,000 votes. Since this number exceeds the approximate 700,000 authentic votes, they now wield absolute control.

What are the implications of this for Tornado Cash?

The assailant, by seizing control of the governance, can:

Retrieve all secured votes

Empty all tokens contained in the governance contract

Disable the router

Nonetheless, the attacker is still unable to:

Deplete individual pools

What caused this event?

When the malicious actor formulated their deceptive proposal, they alleged it was based on the same logic as a previously approved proposal. However, this wasn’t entirely accurate because they incorporated an additional function.

Upon voter approval of the proposal, the attacker leveraged the emergencyStop function to modify the proposal’s logic, which in turn awarded them with counterfeit votes.

The attacker’s complete dominance over Tornado Cash’s governance empowers them to retrieve all locked votes, empty the governance contract of all tokens, and disable the router. As per @samczsun, at the time of reporting, the attacker had “simply withdrawn 10,000 votes as TORN and subsequently liquidated them all.”

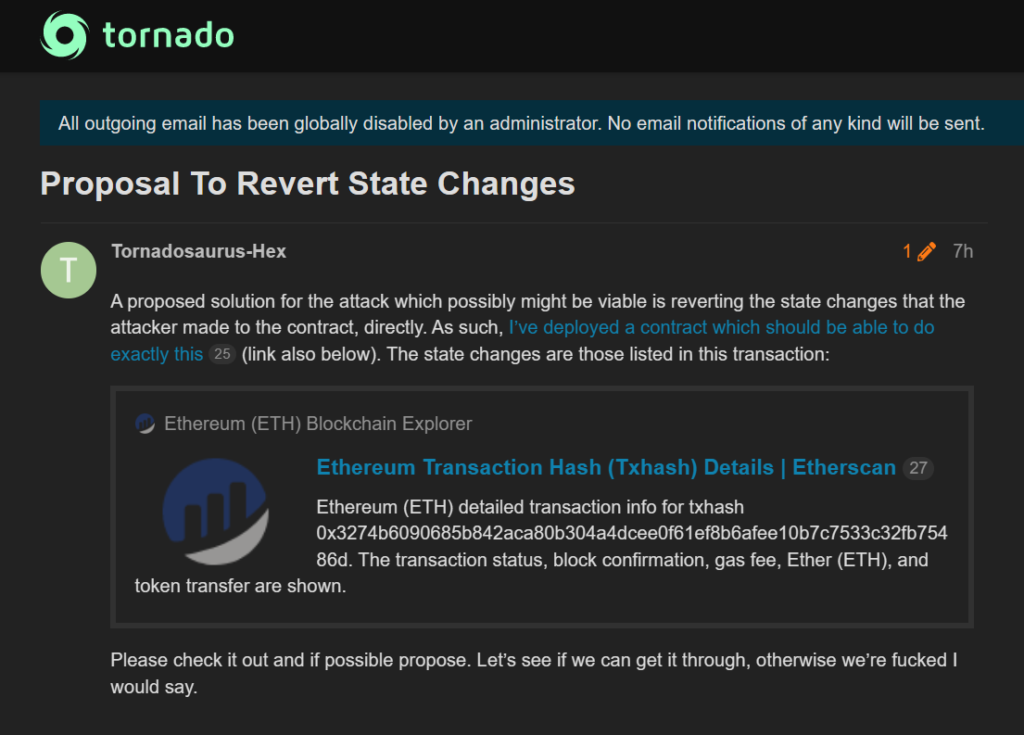

This incident serves as a crucial reminder to cryptocurrency investors to thoroughly scrutinize proposal descriptions and their underlying logic. A prominent member of the Tornado Cash community, known as Tornadosaurus-Hex or Mr. Tornadosaurus Hex, has confirmed the potential compromise of all funds in Governance. He has urged all members to withdraw any funds currently secured in governance.

The Tornado Cash community developer

They also attempted to set up a contract that might potentially reverse the changes, all the while advising the community to withdraw their funds. A distress signal from a Tornado Cash community developer, who verified these incidents, stated:

“We were aware of the protocol attack this morning. A fellow community developer and I have been contemplating solutions all day, but the situation seems nearly hopeless – as it stands, the attacker holds control over Governance.”

Currently, the team is seeking Solidity developers who can help prevent the protocol’s imminent demise. They have also expressed a need for communication with Binance, citing that this exchange possesses more tokens than the attacker.

A previous Tornado Cash developer is said to be in the process of creating a novel crypto mixing service from the ground up, aimed at addressing the “critical flaw” inherent in Tornado Cash.

The developer envisions that this solution will enable the community to protect itself from hackers who exploit the anonymity sets of honest users, without necessitating overarching regulation or compromising on crypto principles.