In just six years, Changpeng “CZ” Zhao transformed Binance from a startup funded by a $15 million ICO into a $60 billion titan of the crypto world. His recent resignation as CEO, part of a deal with the U.S. Department of Justice, marks a significant moment not only for Binance but for the broader crypto industry.

This event is part of a larger scrutiny faced by key players in the crypto space, with Kraken and Coinbase also facing legal challenges from U.S. authorities for various regulatory issues.

The crypto landscape is clearly in a state of flux, with regulatory actions signaling a shift towards more stringent oversight.

This period of change is evident in the diverse developments across the industry, from Grayscale and BlackRock’s dealings with the SEC to Circle’s new initiatives, Bittrex Global’s closure, and CoinGecko’s latest acquisition.

What happened to Binance?

Binance, under its CEO Changpeng “CZ” Zhao, agreed to a $4.3 billion settlement with U.S. officials for failing to implement adequate safeguards against illicit activities.

U.S. authorities accused Binance of allowing criminals to transfer stolen funds through the exchange.

We’re pleased to share we’ve reached resolution with several US agencies related to their investigations.

This allows us to turn the page on a challenging yet transformative chapter of learning that has helped us become stronger, safer, and an even more secure platform.

As part of the settlement, Binance will pay significant penalties to various U.S. departments, including over $3.4 billion to the Financial Crimes Enforcement Network and around $1 billion to the Treasury’s Office of Foreign Assets Control.

Additionally, Binance and CZ will face stringent monitoring and reporting requirements moving forward. This settlement resolves many civil and criminal investigations into Binance, but a civil case with the SEC remains pending.

Following the settlement with U.S. officials, Changpeng “CZ” Zhao has decided to step down from his role as chair of the board for Binance.US, distancing himself from the exchange’s governance.

This move aligns with his earlier resignation as Binance CEO after pleading guilty to a felony charge related to anti-money laundering deficiencies.

Binance.US, led by Norman Reed, remains separate from these legal issues but is still involved in an SEC lawsuit. CZ’s future involvement in the crypto industry and his legal status, particularly his travel permissions while awaiting sentencing, are currently under consideration by the court.

Today, I stepped down as CEO of Binance. Admittedly, it was not easy to let go emotionally. But I know it is the right thing to do. I made mistakes, and I must take responsibility. This is best for our community, for Binance, and for myself.

Binance’s mistakes may be reflected in the industry standards

The recent $4.3 billion settlement of a major cryptocurrency exchange with the U.S. Department of Justice is being viewed positively by industry experts.

This settlement is seen as a step towards reducing apprehensions about engaging with this global exchange, thereby potentially enhancing its trustworthiness in the eyes of investors and users.

Industry observers point out the significance of adhering to regulatory standards, emphasizing that even traditional financial institutions have faced similar challenges. The resolution of the exchange’s compliance issues, particularly around KYC protocols, is considered a positive move for its future operations and for the cryptocurrency industry at large.

Looking ahead, there is growing optimism about the future of Bitcoin.

Expectations are high for the approval of a Bitcoin exchange-traded fund (ETF) in the United States, and the anticipated Bitcoin halving in 2024 is also drawing attention.

These factors, combined with the potential for reduced interest rates by the Federal Reserve, are expected to positively influence Bitcoin’s value.

Furthermore, the forthcoming U.S. elections and ongoing fiscal challenges in major global economies are seen as factors that could increase Bitcoin’s attractiveness as an investment option.

Binance’s future plans

End support for BUSD

Binance has outlined its plan to phase out support for Binance USD (BUSD) products.

Beginning December 15, Binance will no longer support the minting of new BUSD coins, following a decision by Paxos to stop its production.

Users are advised to either withdraw or convert their BUSD into other assets on the exchange before this date.

After December 31, Binance will deactivate BUSD withdrawals, and any remaining BUSD balances will be automatically converted to First Digital USD (FDUSD) for certain users.

This decision is part of Binance’s broader strategy to gradually reduce its reliance on BUSD.

Initially, the exchange will discontinue borrowing and lending services for BUSD, with complete support cessation planned by February 2024.

This move follows regulatory challenges, including the U.S. Securities and Exchange Commission labeling BUSD as an unregistered security and the New York Department of Financial Services ordering a halt to its issuance.

The change in strategy coincides with significant shifts within Binance, including a $4.3 billion settlement with U.S. authorities and a leadership transition, with the former CEO stepping down and the head of regional markets assuming the role.

Once one of the largest stablecoins in terms of market capitalization, BUSD has seen a significant decrease in value over the past year.

Binance to end support for crypto card in Europe

Binance, facing increased regulatory scrutiny globally, is set to end its crypto card services in the European Economic Area (EEA).

The service, which allowed for the direct conversion of digital assets in Binance accounts to local fiat currency, will cease from midnight (UTC+0) on December 20, 2023, affecting all 27 EU member states and others like Iceland, Lichtenstein, and Norway.

Binance’s decision follows the discontinuation of the service by UAB “Finansines passages ‘Contis,’” the issuer of the Binance Visa Debit card.

This change will not affect the accounts of EEA residents but will end the Refugee Crypto Card service introduced for Ukrainian refugees.

The discontinuation in the EEA, alongside earlier service stoppages in Latin America and the Middle East, reflects the challenges Binance faces, including the loss of operating licenses in several countries and ongoing legal battles with regulatory bodies like the SEC.

Binance launches pilot program for bank custody of collateral

Binance has launched a pilot programallowing institutions to trade without depositing collateral directly on the exchange.

This innovative approach enables banks to keep trading collateral off-exchange, such as at a third-party bank, reducing counterparty risk.

The program, mirroring traditional financial market practices, offers flexibility for institutions to manage their crypto-asset allocation according to their risk tolerance. Institutions can hold collateral in cash or Treasury bonds, earning yields while trading.

This initiative, in development for over a year, aims to address institutional investors’ concerns about counterparty risk – the risk of a party defaulting on its contractual obligations.

By not requiring crypto or cash deposits on the exchange, the program lessens the risk of asset loss due to potential exchange issues.

Binance plans to expand this program, engaging with banking partners and institutional investors interested in participating. This move by Binance follows similar efforts by other exchanges to enhance security and trust in crypto trading.

After recently suing Binance, the SEC now targets Coinbase for allegedly operating as an unregistered securities exchange, adding to regulatory scrutiny in the crypto industry.

The U.S. government’s finance watchdog, the Securities and Exchange Commission (SEC), is suing Coinbase. Coinbase is a big company in New York that trades cryptocurrencies like Bitcoin.

The SEC says that Coinbase should have registered as a broker, national securities exchange, or clearing agency, but they didn’t.

This registration helps keep trading fair and transparent.

Also, the SEC claims that Coinbase has been selling certain cryptocurrencies that it shouldn’t have. These include Solana, Cardano, Polygon, Filecoin, The Sandbox, Axie Infinity, Chiliz, Flow, Internet Computer, Near, Voyager Token, Dash, and Nexo. According to the SEC, these count as securities, and you need special permission to sell them.

Today we charged Coinbase, Inc. with operating its crypto asset trading platform as an unregistered national securities exchange, broker, and clearing agency and for failing to register the offer and sale of its crypto asset staking-as-a-service program.https://t.co/XPG2gDkxtVpic.twitter.com/hCdVMw8B2v

— U.S. Securities and Exchange Commission (@SECGov) June 6, 2023

The lawsuit also says that Coinbase has been working like a broker for securities since 2019 without the needed registration. This is two years before they first started offering public shares in April 2021.

The SEC says that Coinbase’s staking program is also a problem. This program involves five different cryptocurrencies. According to the SEC, this makes the staking program an investment deal and counts as a security. Coinbase has been arguing with the SEC about this, saying its staking products are not securities. They keep arguing even though Kraken, another crypto company, settled with the SEC and stopped offering staking services in the U.S.

Gary Gensler, the head of the SEC, spoke about the lawsuit against Coinbase. He said Coinbase had not given its customers enough protection against scams and manipulation. They’ve also not been open about conflicts of interest. Gurbir Grewal, who is in charge of enforcing SEC rules, said that Coinbase knew they were breaking federal securities laws, but they did it anyway.

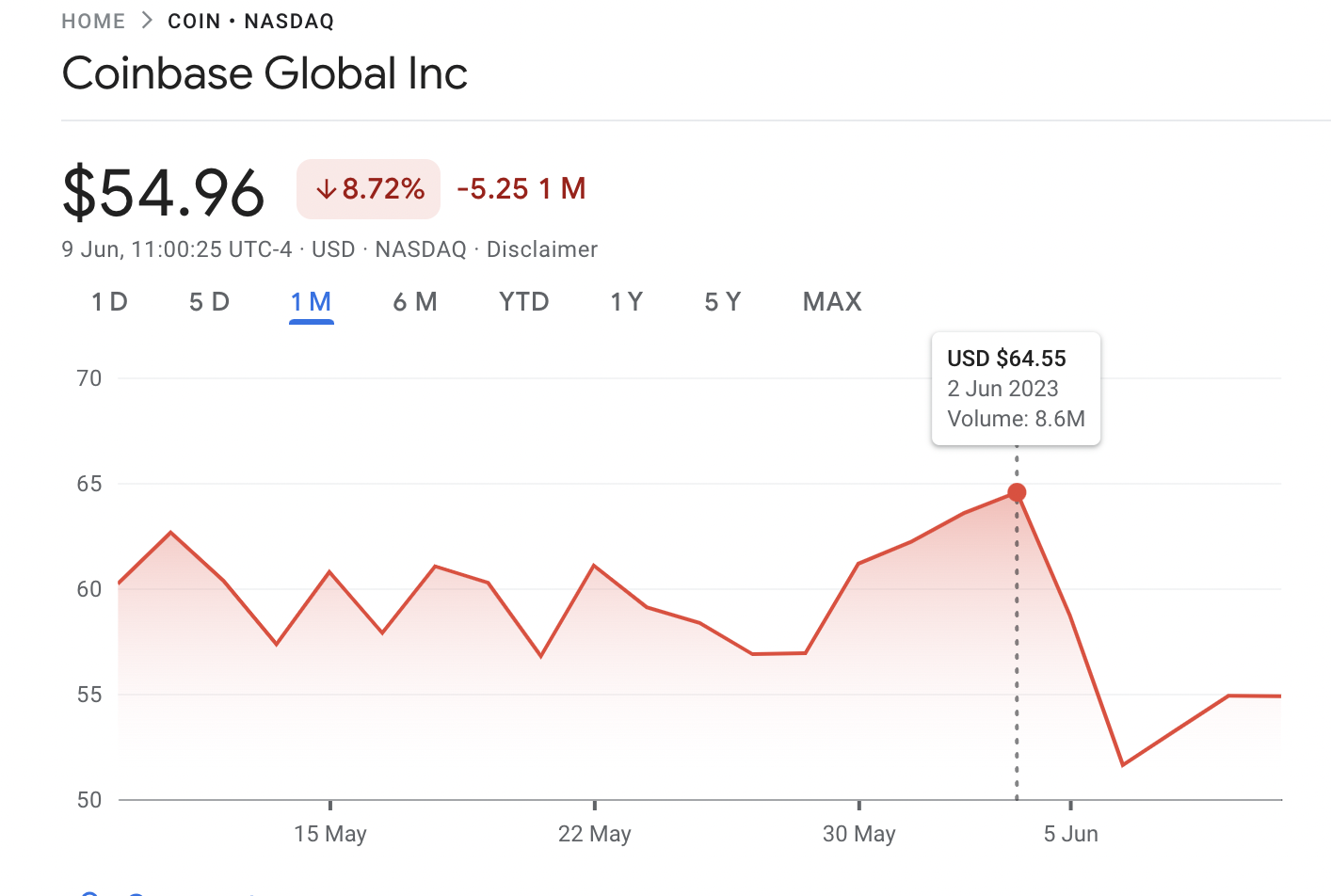

After the SEC announced its lawsuit on June 6, the price of Coinbase’s shares fell by 15% before trading started.

The SEC’s lawsuit against Coinbase happened just one day after they also sued Binance. Binance is another crypto company that the SEC accuses of breaking securities laws and mixing up customers’ money. Binance is in trouble for breaking 13 different securities laws.

The U.S. Securities and Exchange Commission (SEC) has charged Binance, the world’s largest crypto exchange, and its founder, Changpeng Zhao. They’re accused of mixing up billions in user funds and sending them to a Zhao-controlled company in Europe.

The SEC says Zhao and Binance dodged their own rules to let rich U.S. investors keep trading on Binance’s unregulated international platform. It’s even claimed that an executive admitted the company acted as an unlicensed securities exchange in the U.S.

The lawsuit also suggests that Binance.US was created to protect Binance and Zhao from legal issues. Two former Binance.US CEOs, likely Catherine Coley and Brian Brooks, raised concerns about Zhao’s control over the company.

Between 2018 and 2021, Binance made $11.6 billion, mostly from transaction fees. The SEC claims that Binance knowingly had many U.S. customers and didn’t act, even though it’s against federal law to offer and sell unregistered securities. Binance’s compliance efforts in 2019 were mostly for show, according to the SEC.

Lastly, the SEC accuses Zhao of setting up a plan to help rich customers evade regulations using a VPN service to hide their location and fake compliance documents to cover their tracks.

Coinbase is a publicly traded company

But people in the crypto industry are confused about the lawsuit against Coinbase. This is mainly because Coinbase is a company that has publicly traded shares.

Binance’s boss, Changpeng Zhao, responded to the lawsuit against Coinbase by teasing the SEC.

If you have to pick a fight with everyone, maybe you are the one at fault. 🤷♂️

Paul Grewal, the top lawyer at Coinbase, said that the SEC’s focus on punishing rather than setting clear rules for digital assets is bad for U.S. business. He said we need new laws that create fair and clear rules for everyone instead of lawsuits. But for now, Coinbase will keep doing business as usual.

“The solution is legislation that allows fair rules for the road to be developed transparently and applied equally, not litigation. In the meantime, we’ll continue to operate our business as usual.”

A lot of people in the crypto community are wondering how Coinbase could have gone public in 2021 if it was acting like an unregistered securities broker.

The recent SEC lawsuit against Paxos over Binance USD (BUSD) has caused confusion and debate among the cryptocurrency community.

The U.S. Securities and Exchange Commission (SEC) issued a wells notice to Paxos. They claim that BUSD is an unregistered security, which resulted in the New York Department of Financial Services (NYDFS) ordering the halt of BUSD issuance.

This has led to a range of reactions from the crypto community, with some members dismissing it as fear, uncertainty, and doubt (FUD), while others view it as an attack on the Binance exchange.

The community is split on their thoughts about the situation, with some saying that those who bought the stablecoin were not expecting it to increase in value.

The crypto community on Twitter started to talk about this controversy, but they seem to agree that nobody would buy a stablecoin and anticipate a profit. Others expressed confusion about the development, questioning how BUSD can be considered a security and asking their followers if they expected its value to reach $2.

Some even took it more personally, attacking SEC chairperson Gary Gensler, suggesting that he is on an “unhinged, unchecked crusade against crypto.”

However, some dismissed the news as FUD and pointed out that BUSD is fully backed and the halt in issuance by Paxos will not affect existing tokens. They encouraged everyone to stay informed but advised against making emotional decisions. A few voices have also pointed out the urgent need for a stablecoin registry framework.

Bitcoin analyst Tedtalksmacro also expressed similar thoughts, suggesting that BUSD may not meet the criteria of a security. The analyst hinted that the situation might just be a way to target Binance.

The SEC claims that BUSD is an unregistered security and is suing it's issuer Paxos 🚩

To be considered a security, the Howey Test is used… I don't think BUSD meets the criteria, it's a damn stablecoin!?

It’s important to understand that despite stablecoins being designed to have a fixed value, their holders can still generate profits through methods such as arbitrage, hedging, and staking.

What is BUSD?

BUSD is a stablecoin co-founded by Paxos and Binance. Paxos leverages blockchain technology to provide its Stablecoin as a Service product to other companies.

The company has also previously developed a stablecoin backed by gold, known as PAX Gold (PAXG). Both BUSD and PAXG tokens fall under the jurisdiction of the New York State Department of Financial Services.

BUSD is a fiat-backed stablecoin, pegged to the U.S. dollar. Paxos holds an equivalent amount of U.S. dollars in FDIC-insured banks or backed by U.S. Treasuries, serving as the reserves for the total supply of BUSD.

The price of BUSD adjusts in equal amounts to the changes in the value of the U.S. dollar.

Binance’s CEO still supports BUSD

Binance CEO Changpeng Zhao, also known as “CZ,” announced that the exchange would continue to support Binance USD (BUSD), despite the announcement made by the SEC that argues that BUSD is an unregistered security.

Changpeng Zhao (CZ), CEO of Binance, has reassured users that their funds are secure despite regulatory enforcement.

However, he stressed the fact that Paxos, regulated by NYDFS, fully owns and manages BUSD.

Paxos will continue to manage BUSD, including redemptions, and its reserves have been audited by multiple parties, according to Zhao. He acknowledged that the enforcement action might cause a decrease in BUSD’s market cap over time. But Binance will consider alternative non-USD-based stablecoins.

Despite this, Binance will remain supportive of BUSD on the exchange, though it acknowledges that some users may switch to other stablecoin tokens due to the enforcement.

CZ also explained that Paxos, the issuer of the Binance USD (BUSD) stablecoin, is regulated by the New York State Department of Financial Services. He has made assurances of its reserves, which have been audited by multiple parties.

Zhao also acknowledged that the actions taken by the SEC and NYDFS could have a significant impact on the future development of the cryptocurrency ecosystem. He warned of the potential implications if BUSD is ruled as a security by the courts.

Given the regulatory uncertainty in certain markets, Binance may also review other projects to ensure the safety of its users. This comes after a number of cryptocurrency service providers, and tokens have faced enforcement actions by American regulators, including Ripple’s ongoing legal battle with the SEC over XRP being an unregistered security. Kraken also ceased its staking services to U.S. clients and paid a $30 million settlement to the SEC for failing to register its crypto asset staking program.

Policymakers have scrutinized Binance, the largest crypto exchange, amid multilateral sanctions against Russia and U.S. sanctions against Iran. At the same time, the exchange fails to make its balance sheet fully transparent to auditors.

Binance joins the Association of Certified Sanctions Specialists

In an effort to stay compliant with global sanctions, Binance was one of the first cryptocurrency firms to join the Association of Certified Sanctions Specialists (ACSS).

According to a news release on January 6, Binance announced that its sanctions compliance team would receive training as part of the ACSS certification process. The website states that the group offers an exam covering “knowledge and skills common for all sanctions professionals in different employment settings.”

“The blockchain industry is still young, and it’s important to maintain the highest level of compliance in a rapidly-evolving space,” stated Chagri Poyraz, Binance’s global head for sanctions. “At the end, we want the industry standard in security and compliance to continue alongside other industry players.”

In October 2022, Poyraz stated that the exchange had complied with multilateral sanctions against Russia after the country invaded Ukraine. However, he said there was “room for improvement” when it came to clarity in EU guidelines on crypto.

Binance claims that the ACSS training will inform the exchange’s staff about guidelines from the U.S Treasury’s Office of Foreign Assets Control, and help them to avoid potential violations. According to Binance, the exchange is the largest in the entire crypto space and is available in over 100 countries.

Binance US does business in US-sanctioned countries

There have been reports that Binance might have granted Iran-based users certain services, which may be in violation of United States sanctions. This has prompted officials to investigate.

An investigative report by Reuters shows that individuals in Iran continued trading on Binance even after Iran was placed on a blacklist.

Iranians using the exchange also raises questions about capital controls that were increased against Iran in 2018. Binance itself is based in the Cayman Islands and is therefore not subject to U.S. sanctions prohibiting Iranian entities from doing business.

But, Binance US (the version of the exchange that operates in the US) could face secondary sanctions for doing business with a sanctioned country and providing an opportunity for Iranians to circumvent trade embargoes.

Binance aims to build trust with crypto holders but fails to provide transparency

With over 8 billion people on the planet, over 320 million are crypto holders, according to a TripleA estimate. Cryptocurrency use is expanding, but as of the beginning of 2023, only 4% of the world’s population uses it.

Binance, the world’s largest crypto exchange, is trying to boost confidence following a spike in customer withdrawals in December 2022 and a sharp drop in its digital token value. According to the exchange, net outflows totaling $6 billion were managed “without breaking stride” in the first week of December 2022. This is because its finances are strong, and “we take responsibility as custodians seriously.” Binance founder Changpeng Zhao said that his company would lead by example and make a point to prove its transparency, especially after the bankruptcy of the FTX crypto exchange, which collapsed in November 2022. Reuters’ analysis of Binance’s corporate filings reveals that the core business, the Binance.com exchange, which has processed trades in excess of $22 trillion this fiscal year, is mostly hidden from the public.

Binance refuses to disclose the location of Binance.com. It does not disclose basic financial information like revenue, profit, and cash reserves. Although the company has created its own cryptocurrency coin (BNB coin), it doesn’t disclose its role on its balance sheet. It lends money to customers against crypto assets and allows them to trade on margin with borrowed funds. It doesn’t provide details about how large those bets were, how vulnerable Binance is to this risk, nor the extent of its reserves for financing withdrawals.

While Binance has said that it has been audited using the proof-of-reserves mechanism, the auditing firm has deleted the initial report and paused its proof-of-reserves checks due to miscommunication and the way the public perceived the reports. The auditing company, Mazars, did not make any further comments, but Binance’s CEO had already tweeted in Dec 2022 that the audit had been completed.

On October 6, a glitch was discovered on the BNB Chain that allowed someone to create $570 million worth of BNB tokens. The BNB Chain was halted for a few hours while a software patch was created. The good news is that the hacker retrieved a smaller amount.

BNB Chain had to stop on Thursday, October 6, as the blockchain that has ties to the largest crypto exchange in the world suffered what it called a ‘potential exploit.’ On-chain evidence indicated that the potential exploit could have been used to target hundreds of millions of crypto dollars.

BNB Chain is made up of BNB Beacon Chain (BSC) and BNB Smart Chain.

“Due to irregular activity we’re temporarily pausing BSC,” BNB Chain tweeted. Later, it confirmed that the activity was a potential exploit that it described as contained.

Due to irregular activity we're temporarily pausing BSC. We apologize for the inconvenience and will provide further updates here.

Initial token movements indicated that 2 million BSC tokens worth approximately $570 million were being targeted by an attacker on Thursday. However, in a tweet, Binance CEO Changpeng Zhao stated that the attacker could only get away with $100 million. BNB Chain also tweeted to say that $7 million was already frozen.

An exploit on a cross-chain bridge, BSC Token Hub, resulted in extra BNB. We have asked all validators to temporarily suspend BSC. The issue is contained now. Your funds are safe. We apologize for the inconvenience and will provide further updates accordingly.

The fact that such a small amount of assets was stolen underlines the benefits of BNB’s choice to stop the chain and not risk any more assets fleeing. Blockchains are supposedly decentralized entities that can operate independently from single entities. It is impossible to flip a switch to turn it on or off.

On a Reddit thread, BSC confirmed it coordinated the shutdown of the chain following issues with the BSC Token Hub protocol. This protocol is the clearing house for crypto transactions between the Binance-linked Blockchain’s interlocking components. The BSC team thanked the validators for their speedy action.

After confirming that the chain was halted, the team thanked the validators for their cooperation.

We want to thank all node service providers for their quick and attentive response.

Since then, the chain has been back online, and BNB Chain stated that it would hold a series of on-chain governance votes to decide whether or not the hacker funds should be frozen. A vote will be held on a bug bounty system that will reward those who prevent future hacks.

BSC’s native BNB token was rocked by the threat of an attack. It dropped to $278 from $293.10, according to CoinMarketCap, which Binance owns.

On-chain data shows two large withdrawals of 1,000,000 BSC tokens by an attacker who seized crypto assets with cross-chains bridges, swaps, and loans. BNB’s Twitter account assured that all funds were safe and promised to “help freeze any transfer.”

Twitter detectives have discovered that Tether, the largest stablecoin provider, has blacklisted the address in question. This suggests that Tether suspects that the tokens were moved as a result of an attack.

BNB Smart Chain has resumed

The official Twitter account of BNB chain has tweeted that the chain is back in business after a software update was issued to prevent hackers from accessing accounts.

📢BNB Smart Chain (BSC) is running ok from 20+ mins ago.

The validators are confirming their status and the community infrastructure are upgrading as well.

BNB Smart Chain (BSC), which was reopened at 06:40 UTC after chain validators had adopted a software upgrade that would close an exploit used by hackers for stealing funds from the chain.